Deep Dive - Ant Group | Fintech Inside #105, 24th Mar 2026

Inside Ant Group's strategy to build a parallel Visa/Mastercard network, using the global Chinese diaspora - and what Indian founders can learn from it

Hi Insiders, I’m Osborne, an investor in early stage startups.

Welcome to the 105th edition of Fintech Inside. Fintech Inside is the front page of Fintech in emerging markets.

This week’s edition is a bit different. It’s a single, long-form deep dive into a company I’ve been researching for a while - one that I think every fintech founder, investor, and policymaker in India should understand deeply but almost nobody in our ecosystem talks about.

Ant Group.

Alibaba’s financial arm. Parent of Alipay. The world’s largest fintech company by virtually every metric - users, transaction volume, revenue.

I spent the last few weeks going through as much information on Ant as is available in English - equity research, academic papers on its regulatory crackdown, Ant International’s sustainability reports, and a stack of Chinese media commentary (translated by Kimi, I don’t speak Mandarin obvs).

What I found was a story that’s part masterclass in ecosystem building, part cautionary tale about regulatory hubris, and part geopolitical chess move that has direct implications for India’s own fintech ambitions.

Fair warning: this is a longer read than my usual long reads. There was so much more but I had to cut it out in the final edit. I think it’s worth it though. If you only read one Fintech Inside edition this year to understand where global fintech is actually headed, not where X/LinkedIn thinks it’s headed, make it this one.

Thank you for supporting me and sticking around. Enjoy another satisfying week in fintech!

Considering angel investing? I get a bunch of fintech founders reaching out to me for investors. I’d be happy to put you in touch. Send me a DM here.

🤔 One Big Thought

The Invisible Juggernaut: How Ant Group is Quietly Rewiring Global Finance

If you ask an investor or founder in our circles to name the world’s most important fintech company, you’ll probably hear Razorpay, or Stripe, or PayPal, or maybe Visa. All of these companies are important and innovating a lot in the payments and broader fintech sector.

They’d be missing out on one very important company.

I’ve long held the belief that one of the most consequential fintech company in the world is one that barely registers in our discourse: Alibaba’s Ant Group. While the world has been debating stablecoin regulations, credit card interchange fees, agentic commerce, cross border payments and more, Ant Group has built a financial ecosystem of genuinely staggering scale - 1.8bn monthly active users, 150M+ global merchants, and over $21trillion in annual transaction volume.

Ant Group generated an estimated $26-27bn in revenue in 2025, holds 23,550+ patents (including 10,000+ in blockchain alone - the world’s largest portfolio), and 59% of its 24,700 employees are in tech roles. For context, Visa processed about $15tn in total volume in 2024. Ant is already larger. And most of us couldn’t tell a single thing about its business model.

But here’s why it’s important to know the story of Ant Group. It is no longer just a Chinese domestic payments champion. It has become the tip of the spear in a much larger structural shift: the slow, deliberate construction of an alternative global financial architecture that doesn’t run through New York, doesn’t depend on SWIFT, and doesn’t need Visa or Mastercard.

And the strategy powering this expansion? It isn’t a government mandate or a Belt-and-Road loan package. It’s the Chinese diaspora. Tourists, students, e-commerce exporters - ordinary people carrying their financial habits across borders.

I think there’s a masterclass in here for India. Let’s get into it!

The Holy Grail - a financial walled garden

To understand what Ant Group is today, we need to understand why it was created. And the origin story is surprisingly familiar to anyone who’s watched Indian fintech evolve.

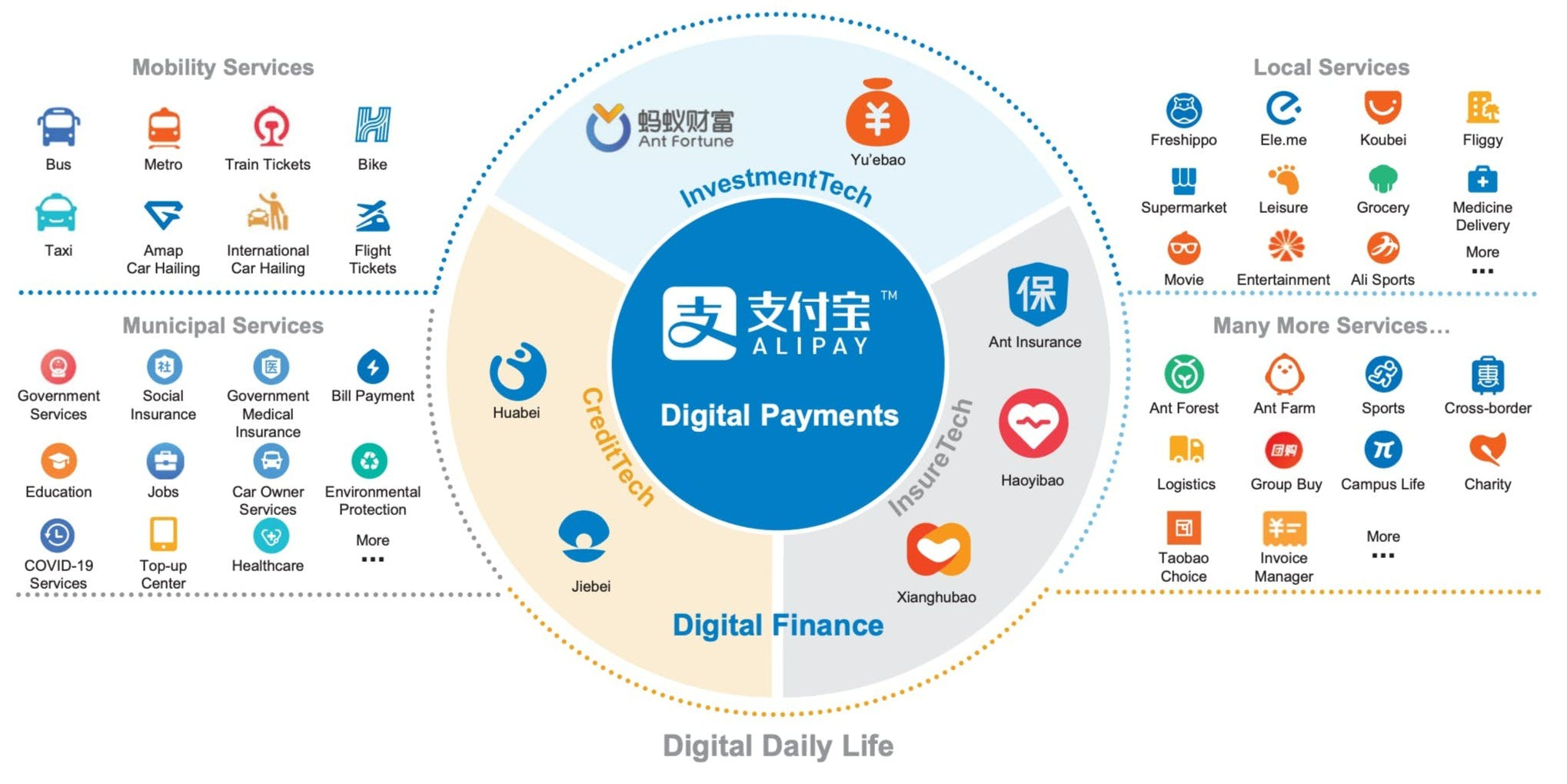

In 2004, Jack Ma had a trust problem. Chinese consumers wanted to shop on Taobao (Alibaba’s consumer marketplace), but buyers didn’t trust sellers, and sellers didn’t trust buyers. There was no established online payment infrastructure, no credit card penetration to speak of, and no culture of transacting with strangers on the internet.

Ma’s solution was elegantly simple: Alipay, an escrow service. The buyer sends money to Alipay. Alipay holds it. The seller ships the goods. Once the buyer confirms receipt, Alipay releases the funds.

But Alipay didn’t stop at payments. And this is where the story gets really interesting.

2013: The Yu’e Bao moment. Ant launched Yu’e Bao, literally “Leftover Treasure”, which allowed users to invest their idle Alipay wallet balance into a money market fund. The minimum investment? 1 yuan. That’s roughly ₹10 in 2013. Within six months, 49M users had parked their money in it, accumulating $36.5bn in assets. The fund was offering 4-6% yields at a time when China’s state-run banks were paying 0.35% on savings deposits.

By 2018, Yu’e Bao had swelled to RMB 1.7tn ($247bn) in AUM with 600M users, the largest money market fund in the world, bigger than any single fund in the US. (It’s since been capped by regulators and has plateaued around RMB 700bn, but that initial explosion is what matters.)

From there, Ant kept layering services on top of its payments base:

Huabei (a virtual credit card / BNPL product with 500M+ users and $140bn+ in annual volume)

Jiebei (cash loans serving 200M+ users)

Ant Fortune (wealth management hosting 5,000+ mutual funds from 150+ asset managers, with AI-driven robo-advisory and a Vanguard joint venture for mass-market investing)

Ant Insurance (partnering with 100+ insurers to offer 2,500+ products, processing 7.25M health claims in 2024 alone with 96% AI automation), and

MYbank (a fully cloud-native digital bank that underwrites SME loans using satellite imagery and AI, with a “3-1-0” model i.e. 3 minutes to apply, 1 second to approve, 0 human intervention). MYbank has served over 50M small businesses, 80% of whom are first-time borrowers who’d never had a bank loan before.

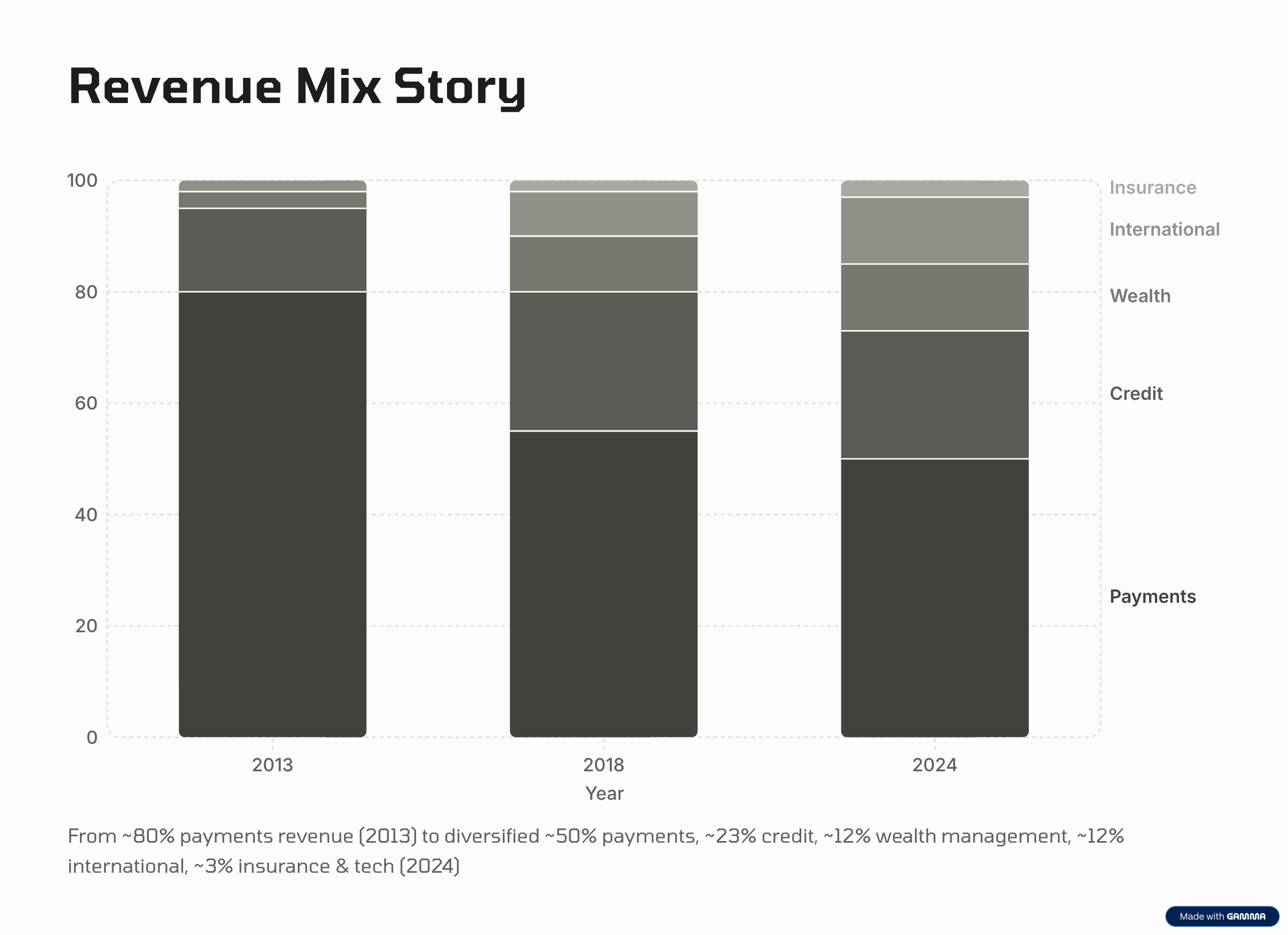

The revenue mix tells the story of just how deep the ecosystem runs: roughly 50% from digital payments, 23% from credit products, 12% from wealth management, 12% from international operations, and the rest from insurance and tech services.

By the time Ant was ready to go public in 2020, it had become a financial walled garden - once a user entered the ecosystem for one service, the gravitational pull of convenience kept them there for everything else. Payments, credit, savings, insurance, investments - all in one app. The Holy Grail for any financial company.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

The $315bn IPO that never was

In late 2020, Ant Group was preparing for a dual listing in Shanghai and Hong Kong. The target valuation: ~$315bn. It would have been the largest IPO in human history. The order books were oversubscribed. The listing was two days away.

Then Chinese regulators pulled the plug.

The narrative often reduces this to a single cause: a speech Jack Ma gave in October 2020 at the Bund Summit in Shanghai, where he called China’s banking regulations “a seniors’ club” and accused Chinese banks of having a “pawnshop mentality.”

But while the speech could have been the spark, Chinese media reported the reason as being systemic financial risk that regulators had been watching for years.

Through Huabei and Jiebei, Ant was originating enormous volumes of consumer loans. But it was keeping almost none of the risk on its own balance sheet. Ant was funding just about 2% of the loans with its own capital and offloading the rest through an Asset-Backed Security (ABS) loophole.

The mechanics were straightforward but the scale was breathtaking.

If a wave of defaults hit, Ant would walk away with its fees while state-backed banks would absorb the systemic damage. Chinese regulators saw this and acted, even if the timing and manner of intervention were heavy-handed by any standard.

The aftermath was painful. Ant was forced to restructure into a financial holding company subject to bank-like capital requirements. The rectification demands were sweeping: establish a licensed consumer finance entity with proper capitalisation, cease regulatory arbitrage in lending, enhance consumer protection, restrict cross-selling, cap Yu’e Bao’s size, and most dramatically - restructure corporate governance so that the board had a majority of independent directors.

Jack ceded control entirely: his voting rights were slashed from 53.4% to just 6.2%, and ten major shareholders agreed to vote independently. Hangzhou’s city government took a 10% stake in the consumer finance subsidiary. Ant’s valuation cratered from $313bn to roughly $79bn in a 2023 share buyback. And in July 2023, regulators imposed a RMB 7.12bn ($1bn) fine - one of the largest penalties ever levied on a Chinese internet company - formally closing the chapter on the crackdown.

Then came the rebound

By 2024, Ant had adapted. Net profit grew 61% YoY to an estimated $5.3bn on roughly $25bn in revenue. The company’s valuation recovered to roughly $103bn by 2025. The business model pivot was real: 98% of consumer loans are now funded by partner banks (versus the pre-crackdown model where Ant was originating on its own balance sheet), and the company has shifted decisively towards B2B tech infrastructure - its distributed database OceanBase now serves 2,000+ enterprise customers, and its blockchain, AI, and cloud services are growing 40%+ annually.

Most importantly, Ant International, the company’s Singapore-headquartered global arm, generated nearly $3bn in revenue in 2024 (up 35% YoY), grew another 20-25% in 2025 to an estimated $3.7bn (roughly 10% of group revenue), and has now produced eight consecutive profitable quarters. It has its own independent board and is being prepared for a potential standalone spinoff and IPO.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

The diaspora strategy or, how to build global rails

This is where the Ant Group story shifts from an interesting Chinese tech narrative into something with direct geopolitical implications. And it’s the part I find most relevant for India. I’ve briefly written about this in Edition 102 - Gold at $5,000, Edition 91 - Trade, Tariffs and Finance and other editions.

For decades, cross-border payments have been controlled by a US-centric architecture: SWIFT for banking messaging, Visa and Mastercard for card rails, correspondent banking for settlement. These systems work, but they’re slow, expensive, and, critically, controlled by institutions that sit under American regulatory jurisdiction. The US has demonstrated repeatedly (Iran sanctions, Russia’s SWIFT disconnection) that it’s willing to weaponise this infrastructure.

Ant Group’s international strategy doesn’t directly challenge this system with rhetoric or government backing. It bypasses it. And the bypass mechanism is simple: follow the Chinese diaspora.

Ant International runs on a three-pillar structure, each pillar targeting a different layer of global financial flows:

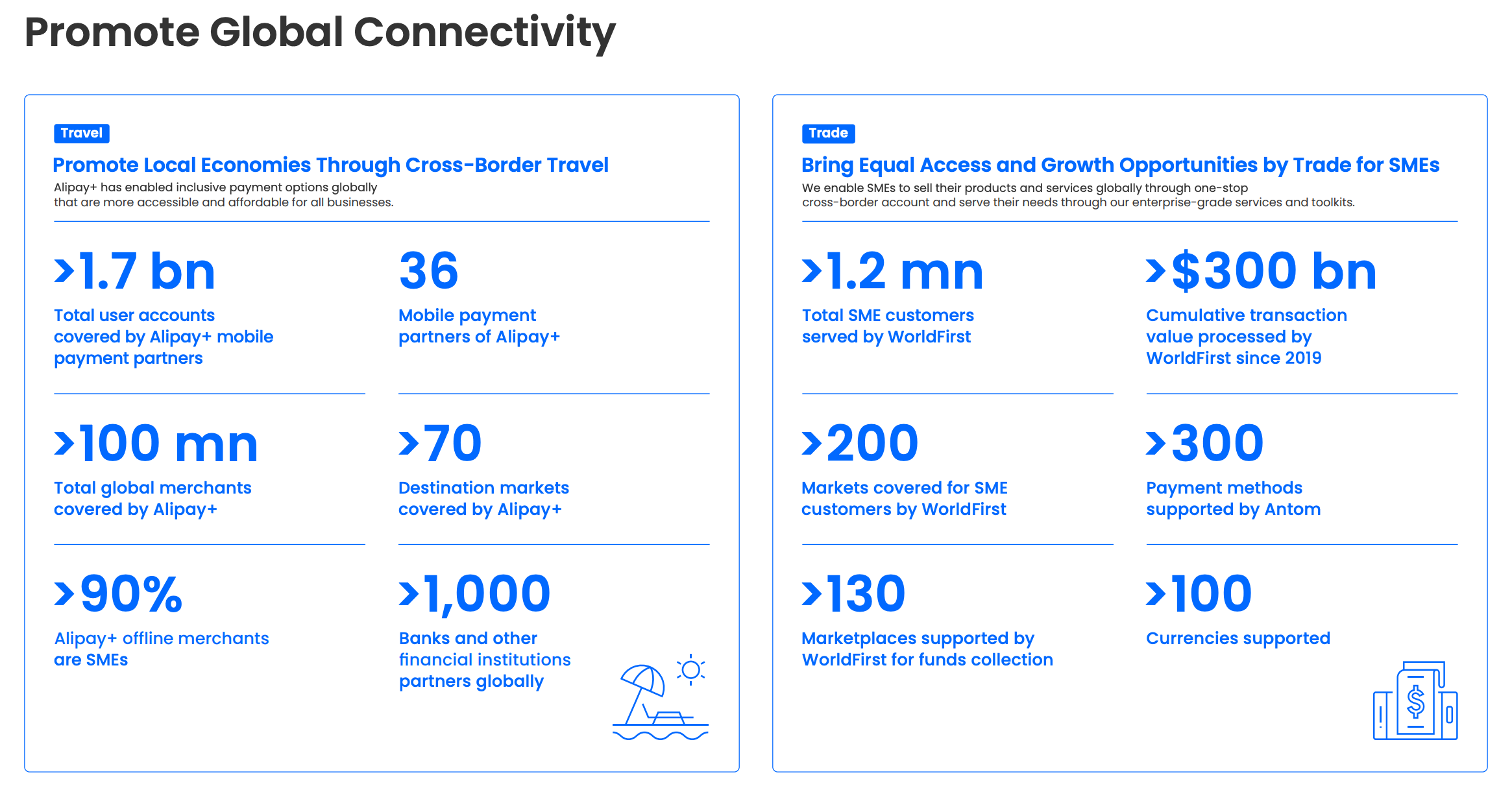

Pillar 1: Alipay+ (the consumer gateway). This is the cross-border payment and digital solutions platform, connecting local e-wallets globally so consumers can “pay like a local” anywhere. More on this below, because it’s the most strategically important piece.

Pillar 2: Antom (the merchant infrastructure). A one-stop acquiring and payment orchestration platform for global merchants. Through a single integration, a merchant can accept 250+ payment methods from across Asia and beyond i.e. bank cards, digital wallets, online banking, BNPL. Antom also offers an AI-powered “Payment Copilot” that automates payment interface integration, drastically reducing the technical barrier for merchants going cross-border. Think of Antom as Ant’s version of Stripe but built for Asia-first commerce.

Pillar 3: WorldFirst (the B2B engine). Acquired from the UK in 2019 for $700M, WorldFirst provides multi-currency “World Account” services for SMEs and cross-border sellers. A small exporter can manage up to 42 currencies in one account, connecting with markets in 200+ countries, collecting payments, converting currencies, making supplier payments, and accessing supply chain financing. Over 38,000 merchants used WorldFirst for cross-border e-commerce payments in 2025.

Beyond these three pillars, Ant also runs a digital bank in Singapore, Alipay wallets for Hong Kong and Macau, and has recently launched Bettr, a lending platform piloting in Hong Kong and Thailand.

The international operation follows it’s domestic strategy - acquire and grow via digital payments but soon diversify into a broader financial services business.

The tourist as a Trojan Horse. In 2025, roughly 87% of Chinese tourists abroad used Alipay as their preferred payment method. Ant went to merchants in Japan, South Korea, Southeast Asia, Europe, and the Middle East with a simple value proposition: “Want Chinese tourist spending? Accept Alipay.” Today, over 150M global merchants do. Ant’s Smart Tourism initiative alone powered payments for 18M Chinese travellers across Europe and Asia. No Visa acquiring agreement needed. No Mastercard interchange. Just a QR code.

The B2B export engine. Through its 2019 acquisition of UK-based WorldFirst and the launch of Antom (its merchant payment and digitisation services arm), Ant built a cross-border collection and disbursement platform for global merchants and SMEs. A small factory in Vietnam selling to Chinese buyers? Ant handles the payment, the FX, the settlement, across 42 currencies in a unified ledger.

Cross-border payment volume grew 25% in 2025, reaching over $350bn. And the partnerships keep expanding: a 2025 Shopify integration enabled 250,000 merchants to accept Alipay from Chinese shoppers worldwide, and collaborations with Uber (85+ countries), Starbucks (12,000 stores), AirAsia MOVE, and Booking.com are embedding Alipay into the travel and commerce workflows that Chinese consumers already use.

And then came the masterstroke: Alipay+

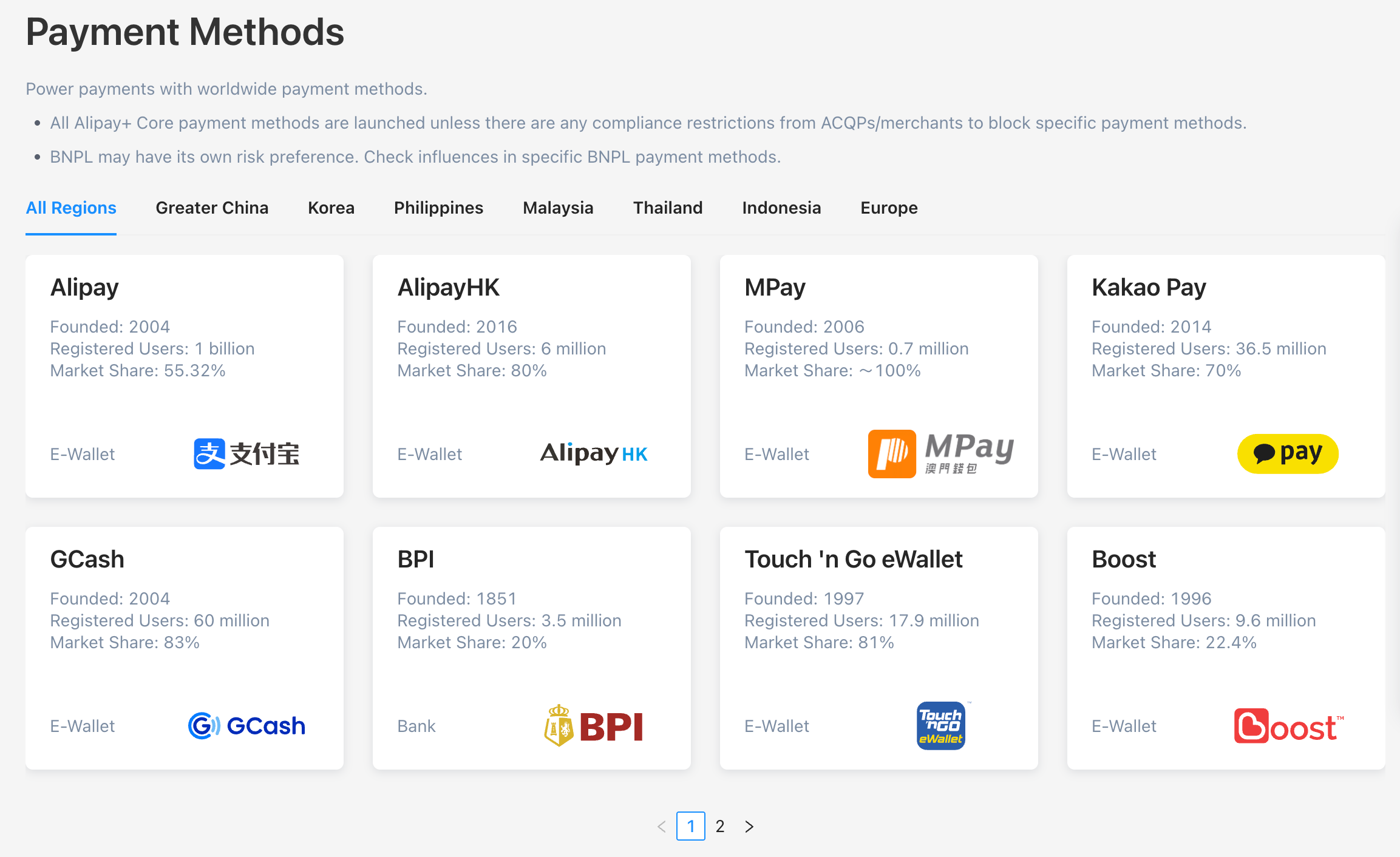

Launched in 2020, Alipay+ is a cross-border payment gateway but not for Alipay users alone. It connects local e-wallets from around the world into Ant’s global merchant network. Here’s how it works in practice: a Filipino tourist travels to Japan. She doesn’t have Alipay. She doesn’t need it. She opens GCash (the Philippines’ leading e-wallet and partly owned by Ant Group), scans a PayPay QR code at a Japanese convenience store, and the transaction is routed, converted, and settled via the Alipay+ backend. The merchant never knows the difference. The tourist pays in her home wallet. Ant clips the transaction fee.

As of mid-2025, Alipay+ connects 40 partner wallets and banking apps to merchants in over 100 markets, with 1.8bn connected user accounts. The scale of the individual partners is what makes this network so formidable:

PayPay in Japan (60M users, 3 million+ merchants, owned by Softbank an early Alibaba investor),

GCash in the Philippines (80M users),

Kakao Pay in South Korea (45M users),

Touch ‘n Go in Malaysia (20M users),

TrueMoney in Thailand (20M users),

ZaloPay in Vietnam (15M users),

plus OCBC Digital in Singapore, Vipps in Norway, Bluecode in Germany and Austria, and Tinaba in Italy.

That’s a long list of integrations across Asia and Europe.

Alipay+ also partnered with national QR code operators PayPay in Japan, DuitNow in Malaysia, SGQR in Singapore, ZeroPay in South Korea, KHQR in Cambodia, NepalPay QR in Nepal and many more, so that partner wallet users can pay at virtually any merchant in these countries without the merchant needing to do anything special. Over 90% of Alipay+ merchants are MSMEs. In the first half of 2025 alone, 6.5M consumers used Alipay+ cross-border payments for the first time, and intra-Asia transactions by partner wallets grew 32% YoY.

The regional strategy is also differentiated, which is worth noting.

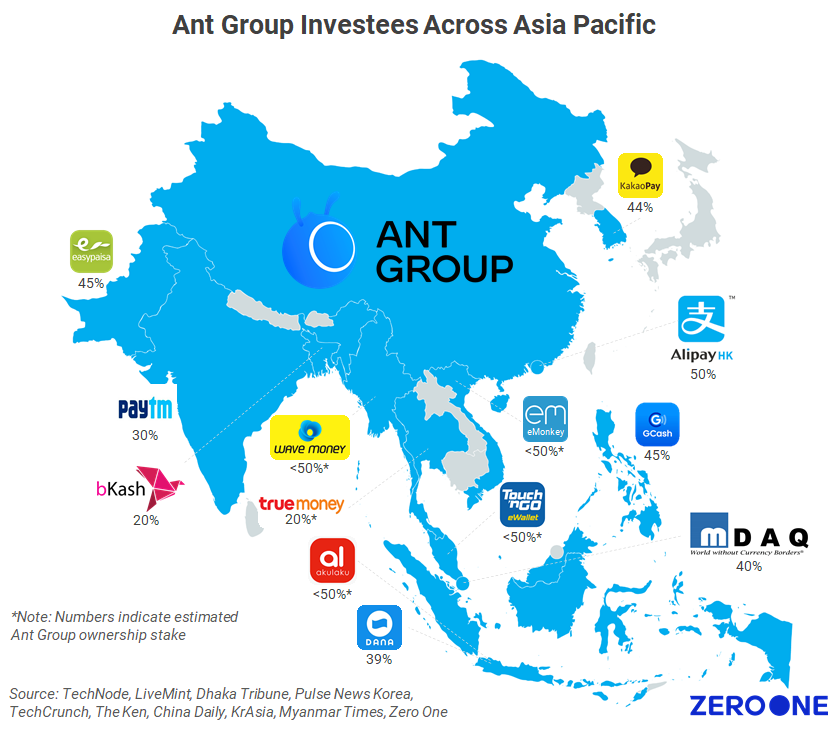

In Southeast Asia, Ant goes deep by investing directly in local fintechs (Ascend Money in Thailand, GCash in the Philippines, earlier Paytm in India), providing wallet technology infrastructure, and integrating across e-commerce and financial services.

In Japan and South Korea, they primarily serve inbound tourism through merchant QR acceptance.

In the West Asia, they’re building out teams in Dubai and Riyadh and introducing Antom for local payment digitisation.

In Europe and North America, they mostly serve outbound Chinese tourism and cross-border trade.

Each market gets a tailored approach, deep cultivation in emerging markets, technology export and network connection in developed ones.

I want to pause and let that sink in. Ant has, effectively, built a parallel Visa network for Asia, except it runs on QR codes and smartphones instead of plastic cards, it’s interoperable across dozens of local wallets, and it completely bypasses the traditional card schemes.

And the way they built it was through a deliberate invest-and-integrate strategy that started in 2015-2017: Ant invested $857M+ in Paytm (India), $200M in Kakao Pay (South Korea), strategic stakes in GCash/Mynt (Philippines), Ascend Money (Thailand), Touch ‘n Go (Malaysia), TrueMoney (Thailand), and ZaloPay (Vietnam). They even tried to acquire MoneyGram for $880M in 2017, but were blocked by US regulators on national security grounds.

Each investment came with technology transfer, Ant’s Wallet Tech platform helped these local wallets evolve from simple payment tools into super-apps.

I had a whole section on Alipay becoming a Super App in China, but it made this edition too long (5,000+ words). I deleted it, but would you want to read about that too? Write to me.

The tech moat — AI, NFC, and Blockchain

Ant Group’s R&D spending in 2024 was RMB 23bn ($3.26bn), an 11% increase YoY. About 40% goes to AI and machine learning, 20% to blockchain, 15% to their distributed database (OceanBase), 15% to security and biometrics, and 10% to cloud infrastructure. They hold over 23,550 patents globally (96% are invention patents), with the world’s largest blockchain patent portfolio at 10,000+.

AI-powered commerce. In February 2026, Alipay announced that its “AI Pay” feature had surpassed 120M weekly transactions. The use cases are expanding fast: AI agents embedded in apps and mini-programs, voice-activated payments through smart glasses, and most ambitiously, the Agentic Commerce Trust Protocol launched in January 2026 with Alibaba’s Qwen AI app and Taobao Instant Commerce. Users simply chat with an AI, with payment handled seamlessly in-agent.

Ant has also built its own foundation models Ling-Plus and Ling-Lite, with 100 bn+ parameters, targeting finance and healthcare applications. Their AI financial assistant Zhi Xiaobao serves 70M monthly active users, and AI-powered fraud detection has reduced fraudulent activity by 83% compared to legacy systems.

Hardware innovation. “Alipay Tap!” an NFC-based contactless payment solution launched in 2024, recently crossed 100M daily transactions (as of January 2026).

The experience has been specifically designed for accessibility - embraced by younger users, older adults, and people with visual impairments.

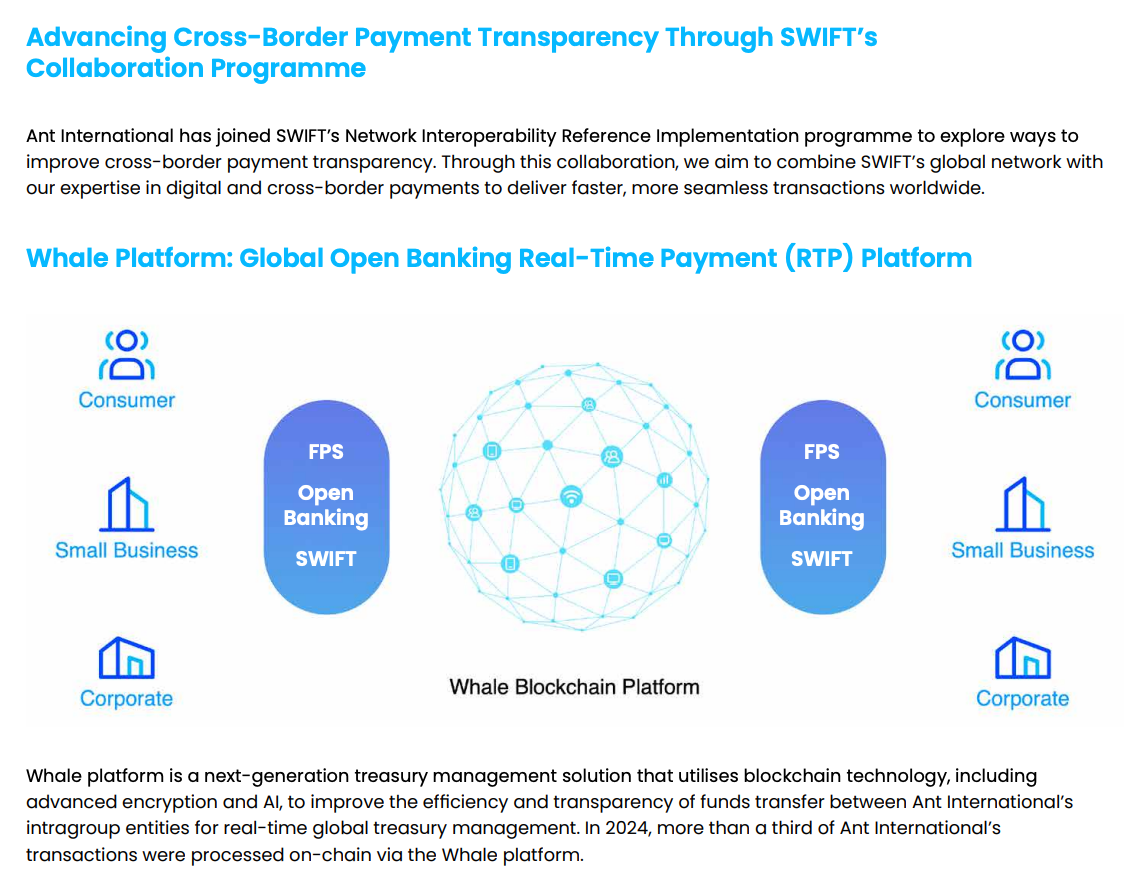

Blockchain and tokenisation. Through AntChain, Ant processes 100M+ daily data uploads with consensus performance exceeding 100,000 TPS. They’re cutting cross-border remittance times by 45% by bypassing correspondent banks entirely. And they’ve launched the Jovay Network (an Ethereum Layer 2, hybrid ZK + TEE architecture, targeting 100,000 TPS) to help banks issue digital bonds and tokenise real-world assets.

Ant also built OceanBase, a distributed database that handles 61M+ queries per second (it holds the TPC-C world record) and is now used by 2,000+ enterprise customers outside of Ant, including banks and telecoms. OceanBase is to Ant what AWS was to Amazon, an internal infrastructure product that’s becoming a standalone business.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

The Ant playbook - what founders can take away

The four points above are mostly about policy and ecosystem design. But I want to go deeper into what Indian and global fintech founders can specifically learn from how Ant was built - the operational and strategic decisions that turned an escrow button into a $100bn ecosystem.

These are the lessons I’d want in front of me if I were starting a fintech company today. I’ve talked about these in several past editions, and you’re probably tired of listening to me like a broken record.

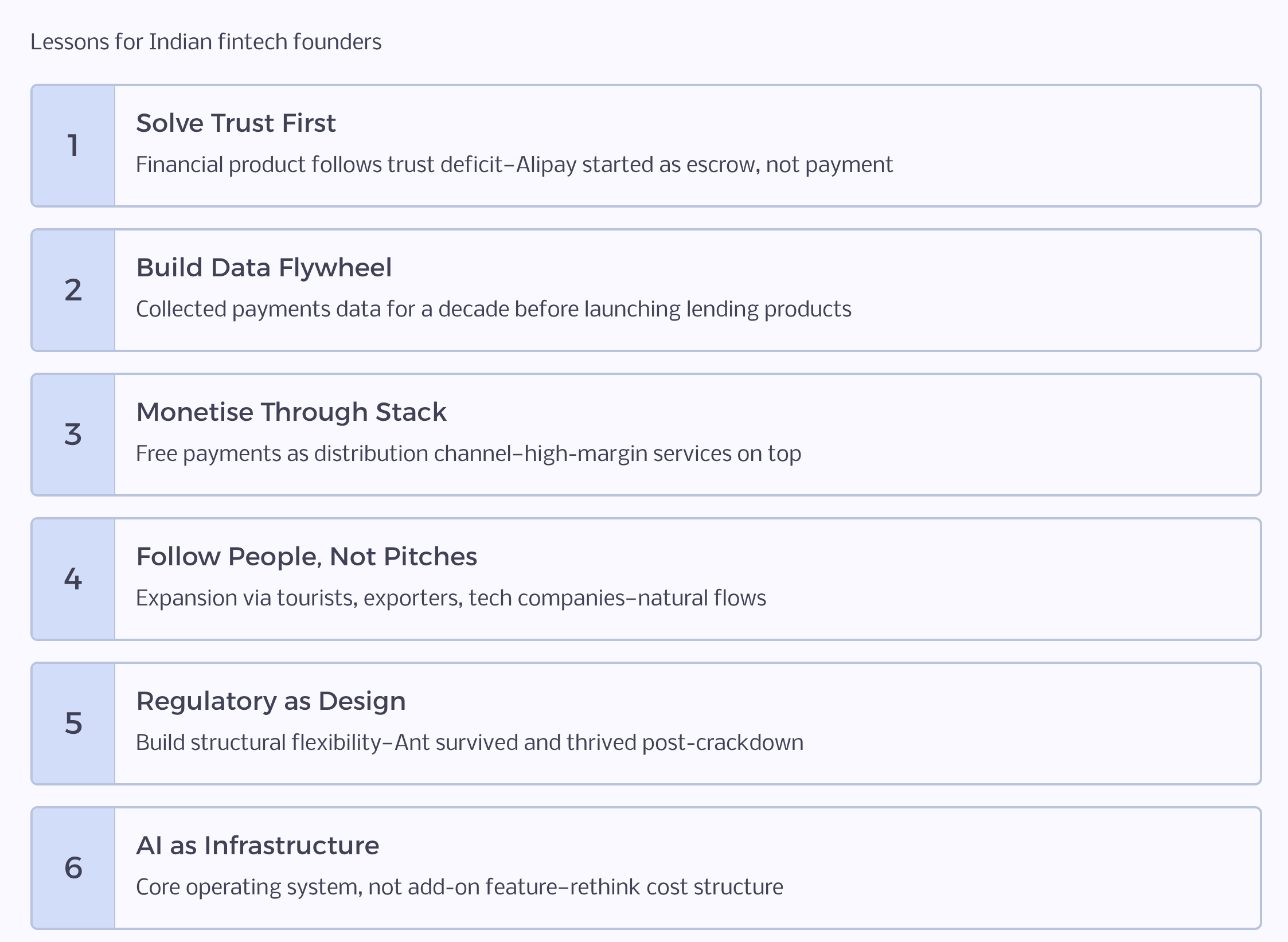

1. Solve the trust problem first. The financial product comes second.

Alipay wasn’t created because someone wanted to build a payments company. It was created because buyers and sellers on Taobao didn’t trust each other.

I see too many Indian fintech founders start with the financial product - “we’re building a savings product” or “we’re doing cross-border remittances” or “we’re making tax filings easier”. In my evaluation and diligence, I’m always asking founders what trust deficit they’re solving and how.

The best fintech companies in India have followed the Ant pattern, often without realising it. Zerodha solved the trust problem of “is my broker ripping me off with hidden charges?”. Slice solved it for young Indians who couldn’t get a credit card from a bank.

Start with the trust gap. The product will reveal itself.

2. Build the data flywheel before you build the lending product.

Ant didn’t start with lending. They collected payments data for nearly a decade before launching Huabei and Jiebei in 2015.

The lesson isn’t “collect lots of data.” It’s that the best lending businesses are built on top of proprietary distribution and data advantages that take years to accumulate. In India, the companies best positioned to become the next Ant-like lenders aren’t necessarily the ones with NBFC licenses today, they’ll be the ones sitting on the richest transaction data.

The question is whether they’ll have the patience and the regulatory room to make that transition.

3. Monetise through the stack, not the transaction.

Ant’s revenue breakdown is instructive. The payment itself is a low-margin, high-volume anchor. The real business is everything that sits on top of it.

I think about this a lot in the Indian context. UPI made the payment layer essentially free. A lot of founders look at that and see a problem, “how do I monetise if payments are free?”. But Ant’s playbook shows that free payments are a feature, not a bug. They’re the distribution channel. The question is what high-margin service you can attach to the payment flow that the customer actually needs.

The merchant doesn’t need to leave the ecosystem. Every layer is a monetisation opportunity. Indian fintechs that obsess over payment MDR are missing the forest for the trees.

4. International expansion follows people, not pitches.

This is perhaps the most actionable learning for Indian founders thinking about global markets. Ant went global by following three natural flows: Chinese tourists spending abroad, Chinese exporters selling cross-border, and Chinese tech companies expanding internationally. Every international product maps directly to one of these flows.

The Indian equivalent of these flows exists, and it’s arguably larger: 32 million NRIs sending $135+bn in remittances annually, Indian IT services companies operating in every major market, Indian students at universities worldwide, and rapidly growing outbound tourism.

5. Regulatory survival is a design principle, not an afterthought.

Ant’s story includes what is probably the most dramatic regulatory intervention in fintech history - something we, in India are all to familiar with. Ant survived. Not just survived, thrived. Profits surged 61% the year after the crackdown ended.

The lesson for Indian founders: build your company assuming the regulatory environment will change significantly during your lifetime. Don’t optimise for today’s rules, build structural flexibility into your capital structure, and your partnerships from day one.

6. AI is infrastructure, not a feature.

This is the lesson most relevant to right now. Ant is spending on core AI products.

Indian fintech founders building today should be asking: “If AI were not an add-on but the core operating system of my business, what would my cost structure look like? What markets could I serve that are currently uneconomical?”.

The bottom line

While the West continues to view global finance through the lens of plastic cards and SWIFT codes, Ant Group is already processing trillions through QR codes, AI agents, and blockchain rails. The infrastructure of the future isn’t being debated in Washington or Brussels. It’s being built in Hangzhou and Singapore.

For Indian builders and policymakers, the question isn’t whether to pay attention to Ant Group. It’s whether we can learn fast enough to build India’s version of this story, using our own extraordinary assets (UPI, India Stack, the diaspora, the trade flows), before the window closes.

I’m optimistic we can. We need to move faster. And we need to think bigger. We need to ask ourselves “how do I build the financial operating system for the next billion users?”

That’s the question Ant answered for China. It’s India’s turn to answer it for the world.

Which of the founder lessons resonates most with what you’re building? I’d love to hear your thoughts - hit reply or find me on Twitter/LinkedIn.

If you enjoyed this deep dive, share it with a friend who’s interested in fintech, geopolitics, or just wants to understand what the world’s most important company you’ve never heard of is actually doing. And as always, thank you for reading.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🎵 Song on loop

Fintech updates can get boring, so here’s an earworm: Dracula by Tame Impala (Spotify / Youtube) has been on loop lately. Classic Tame Impala song - good beats to groove to. Let the party never end!

✨ Call outs

[Video] Petrodollars: Important post given the current environment. Understanding petrodollars is understanding geopolitics. Worth your time.

[Report] Pandora’s Bog: the global energy shock of 2026 by JP Morgan. According to the report, a ~20% disruption to global energy supply has triggered a broad commodity shock, driving inflation, pressuring corporate margins, and increasing downside risk for global equities.

[Project] This is a Claude Cowork skill built by Ameya Pimpalgaonkar. It’s a “…plugin that decodes any technology or market signal into 2nd and 3rd order business insights — using layer-by-layer question sequencing that takes you from noise to structured understanding.”

[Report] 220-slide report by Persistence Capital in India highlighting key trends and insights from 8 sectors of companies in the public markets. Worth a read through for the signal.

👋🏾 That’s all Folks

If you’ve made it this far - thanks! As always, you can always reach me via DM at osborne.vc/dm. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.

ANT group is to be studied and their systems can be adopted and introduced in any country..

Here’s a great read for those with interested in fintech startups

https://iruafeimi.substack.com/p/fintech-mvp-development-explained?r=57lqd9&utm_medium=ios

Thoroughly loved it! It begs the question, how many patents have major fin-tech firms in India have filed in the last decade? Or they relying and have become dependent on proprietary technology of another group (for ex- Ant) that invests in them?