Gold at $5,000 | Fintech Inside - Edition 102, 16th Feb 2026

Why gold crashed 9% in a day, why central banks are buying at all-time highs, and what it means for India's $4.5 trillion gold paradox.

Hi Insiders, I’m Osborne, an investor in early stage startups.

Welcome to the 102nd edition of Fintech Inside. Fintech Inside is the front page of Fintech in emerging markets.

Gold is at $5,000 and behaving in ways it never has before. Central banks are buying at all-time highs. The real yield relationship is broken. India is sitting on ₹380 lakh crore ($4.5tn) worth of gold, more than our GDP.

The price volatility over the last few weeks told us more about the state of the global financial system than any earnings call or policy speech this year.

In this edition, I’m breaking down what seems to be happening with gold, why the old rules stopped working, what it means for India’s $4.5tn gold hoard, and what we should be watching over the next 12-18 months.

This is a long, data dense one - grab a cuppa with my song recommendation in the background.

Thank you for supporting me and sticking around. Enjoy another satisfying week in fintech!

Considering angel investing? I get a bunch of fintech founders reaching out to me for investors. I’d be happy to put you in touch. Send me a DM here.

🤔 One Big Thought

Gold at $5,000: What Broke, What It Means, and What to Watch

Quick disclaimer: I'm a private markets investor trying to make sense of macro, markets, and the global economic machine. The world order is far too complex for my brain to comprehend in its entirety. I'm sure I've gotten things wrong here. If you spot errors in the analysis please drop me an email or DM.

I asked a jeweller about gold recently. He said, the weight surprises you first. Holding a standard 10 gram gold bar feels less like holding metal and more like holding frozen time. “It feels final,” he says. In early February 2026, as gold traded around $4,960 per ounce, more than double its price from mid-2023, that physical weight became impossible to ignore.

But the price isn’t the story. The story is what happened in late Jan, 2026.

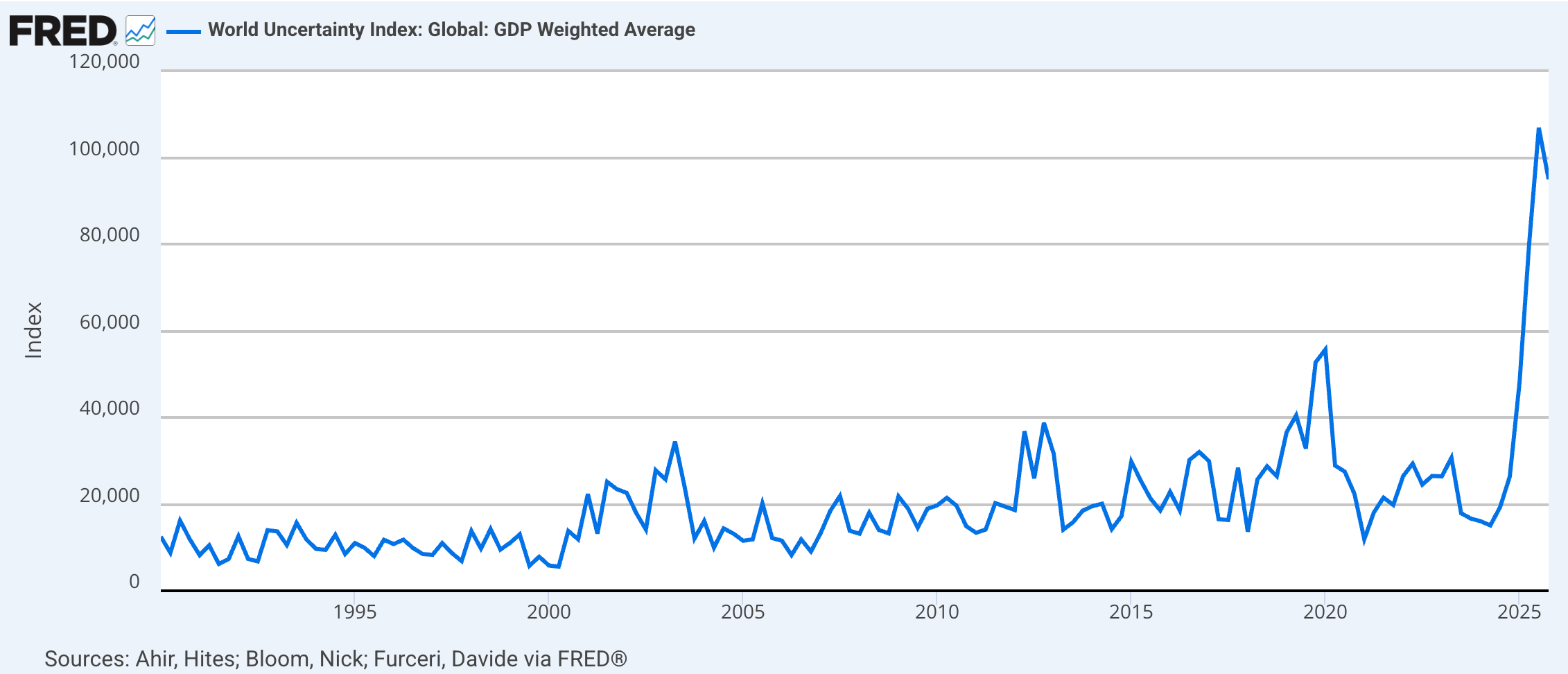

Gold dropped 9% in a single day. Not over a week. Not during a gradual selloff. In one trading session, gold erased over $600 per ounce, wiping out roughly $600 billion in value. Silver crashed even harder - 26% in the same session. These aren’t normal market corrections. These are “something in the system is off” moves.

For Indian fintech founders, finance executives, and investors, what’s happening with gold matters. Gold stopped following its own rules. And when a 5,000-year-old asset starts behaving in ways it never has before, it’s worth paying attention.

The rules that stopped working

Gold has always been simple to understand. It pays no interest. It generates no cash flow. Prices increase over time because of demand/supply movement. But gold has always been used as currency because it’s not too rare or too common.

Moreover, gold’s not used in industry as much as other metals - 90% of gold is used as jewellery or financial asset. So if the economy tanks, the value of gold doesn’t get affected, since industry doesn’t use it as much.

So when government bonds offer attractive returns after accounting for inflation, what economists call “real yields”, investors avoid gold. Why hold a metal that does nothing when you can earn 5%+ safely from a treasury bond?

This logic has broadly governed gold pricing for decades. When real yields rise, gold falls. When real yields fall, gold rises.

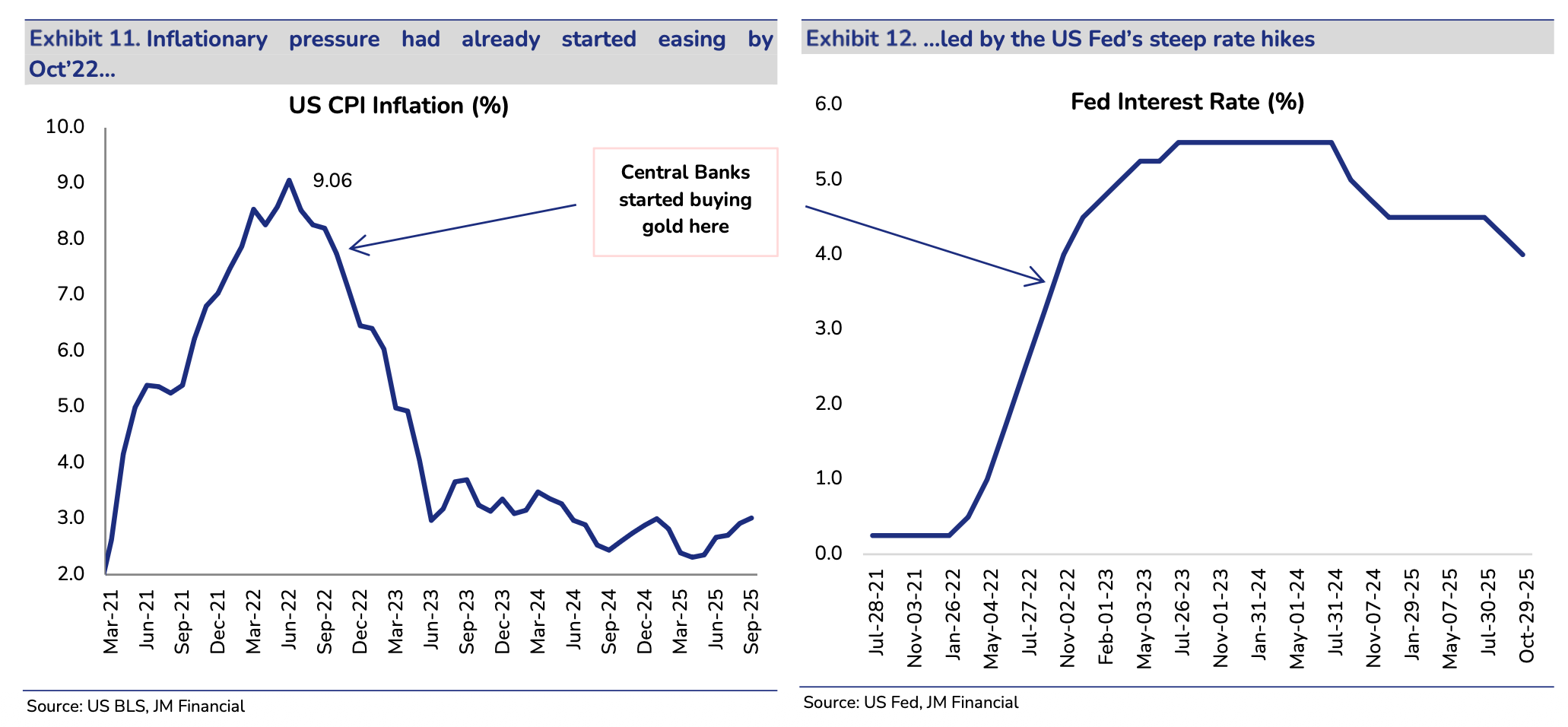

But something broke in 2024 and 2025.

Gold’s rally began when real yields were low, which made sense. But then gold kept climbing even as real yields in the US rose toward 2%. That shouldn’t have happened. Multiple market analysts noted that gold’s “long-standing inverse relationship with real yields seems to have broken down.” In 2025, gold posted its sharpest annual gain since 1979, averaging $3,431 per ounce, up 44% from 2024’s average of $2,386, despite real yields staying near multi-decade highs.

The traditional thermometer broke. And nobody is quite sure why.Three forces changing the game

Three Forces Changing the Game

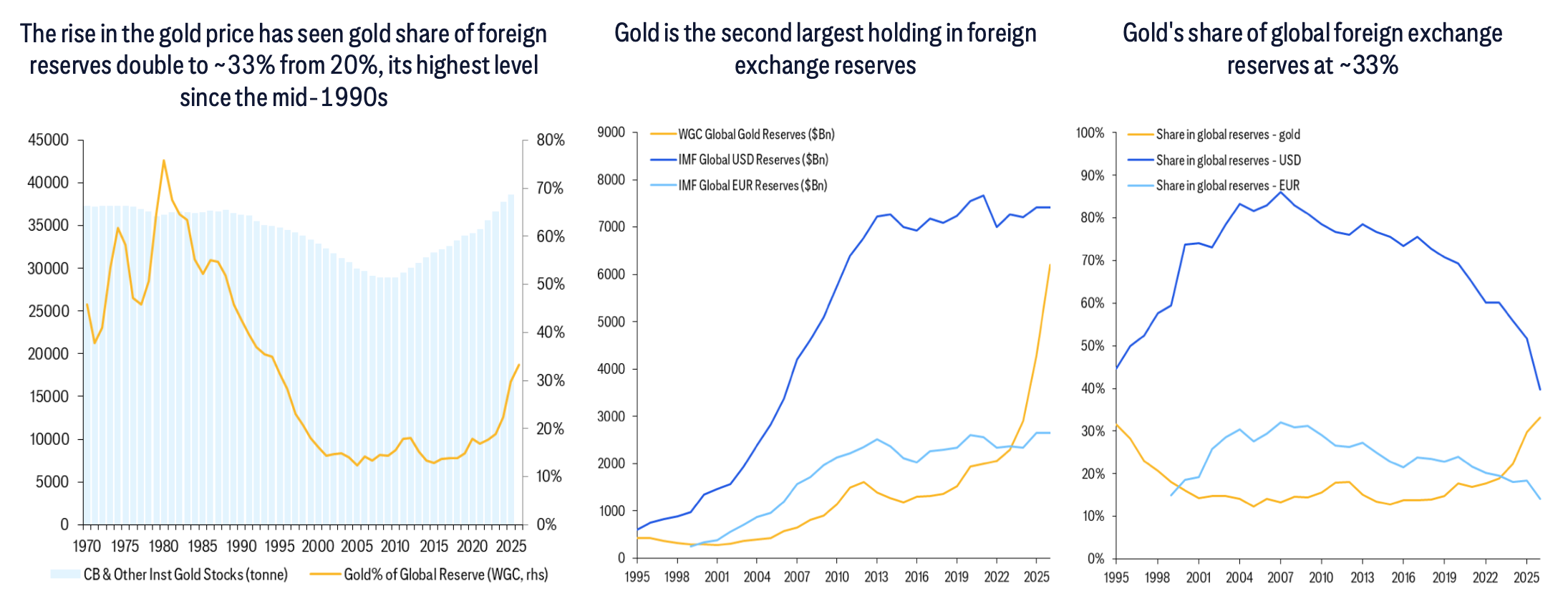

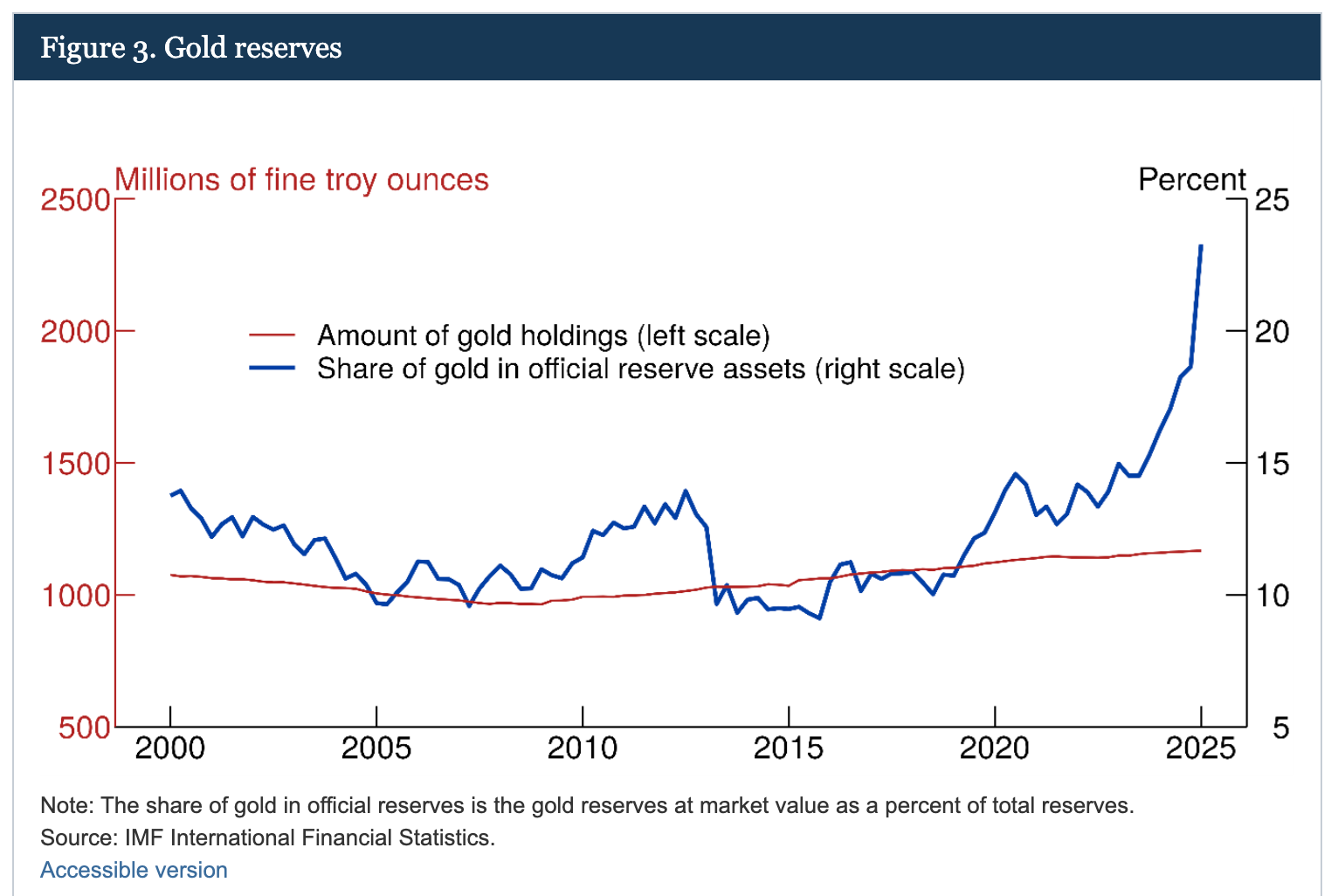

The most common explanation points to central banks. Since 2022, emerging market central banks have increased their gold purchases fivefold. China’s central bank bought gold every single month for over two consecutive years, even as prices hit record highs. They weren’t trying to buy low and sell high. They were building something else.

To understand what, you need to understand what happened in February 2022.

The Russia precedent: when digital became “revocable”

After Russia invaded Ukraine, Western governments froze approximately $300 billion in Russian central bank reserves. These weren’t physical bills in a Moscow vault. These were digital holdings, numbers on screens in banks in London, New York, and Frankfurt. With a few keystrokes and some coordinated phone calls, Russia’s foreign reserves became inaccessible.

Central banks in China, Turkey, Poland, India, and dozens of other countries watched this and learned a harsh lesson: if your national wealth is a number on a screen in someone else’s country, it isn’t truly yours. Digital reserves, they realised, are essentially “revocable permissions” granted by Western governments.

This wasn’t theoretical anymore. It was demonstrated capability. Add to it, the fact that there are several wars ongoing, governments being toppled and more, countries being acquired, tariff threats and more. Pick your poison - this is a very volatile time for the global economy.

So central banks started buying gold. Not as an investment. As insurance against a world where your reserves could be frozen if you end up on the wrong side of a geopolitical environment.

Central banks as “institutional preppers”

According to World Gold Council data, central banks purchased 250 tonnes of gold in Q1 2025 alone - the highest quarterly purchase ever recorded. This buying continued into 2026 even as gold prices surged past $5,000. If you’re trying to maximise returns, you don’t buy an asset at all-time highs. But if you’re building a parallel financial infrastructure that no one can freeze, sanction, or turn off remotely, price becomes secondary to quantity.

Gold seems to have reassumed its historical role as the “final settlement asset” - the one asset that requires no intermediary, no clearinghouse, no permission from a foreign government to use. Every other major asset, from bank deposits to Treasury bonds to corporate stocks, represents someone else’s promise to pay. Gold just exists.

The geopolitical fragmentation accelerator

Add AI dominance to this mix and you have the world reorganising into competing blocs. The US and its allies on one side. China and its partners on another. A large group of countries trying to stay neutral in between. As this fragmentation accelerates, the question every central bank faces is: whose currency do we trust for the next 50 years?

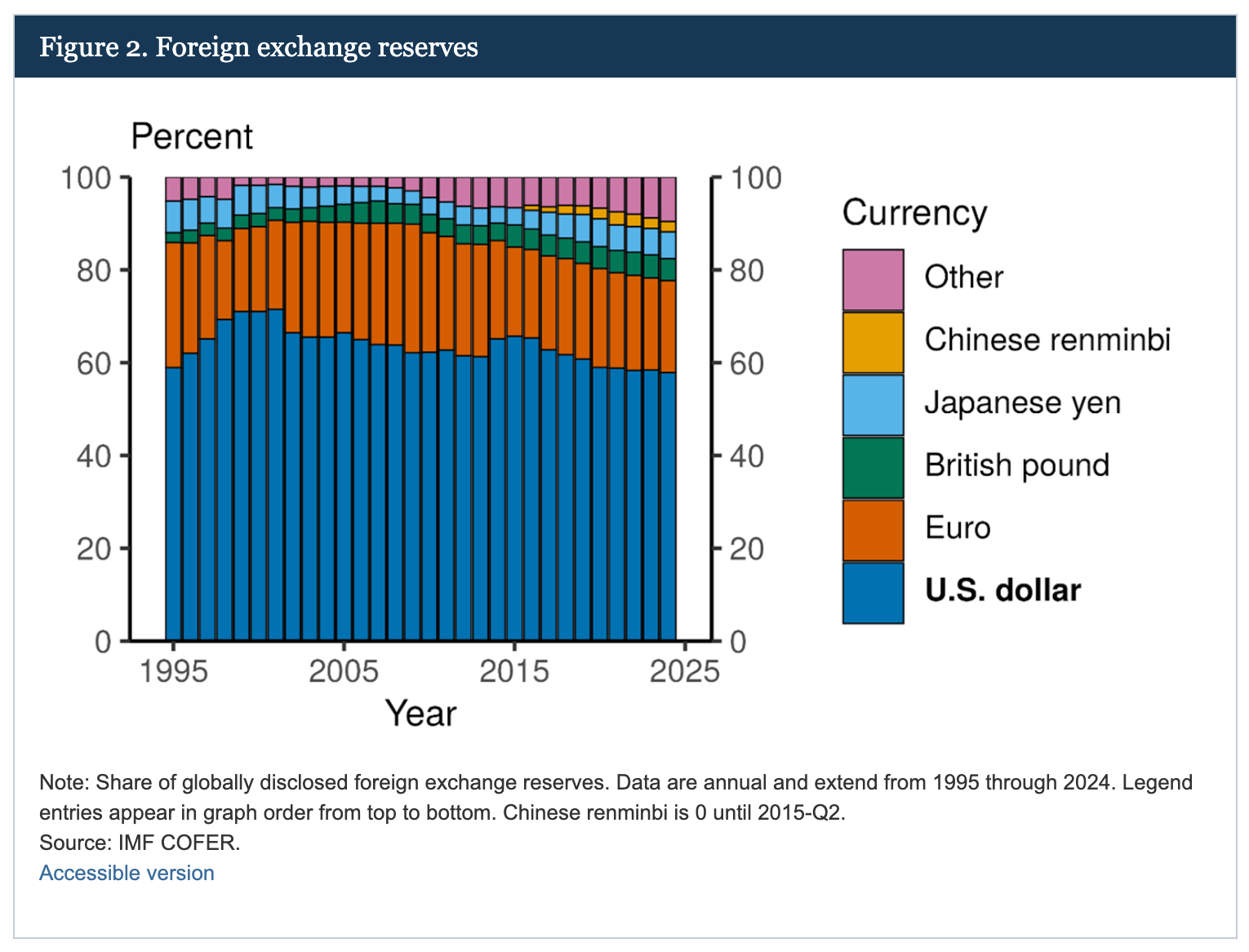

The dollar still dominates with roughly 59% of global foreign exchange reserves are held in US dollars. But that dominance is eroding. The euro’s share is stable. The renminbi’s share has doubled from 2% to nearly 5% in five years. Gold’s share has been creeping up.

When central banks fear their reserves can be frozen, as the Russia precedent demonstrated, the traditional calculation around gold’s “opportunity cost” completely breaks down. Gold’s zero yield stops mattering when the alternative might be total confiscation.

This is why gold kept rising despite higher interest rates. The risk being priced shifted from “will inflation erode my wealth?” to “will the system even let me access my reserves?”

What this means for India: The $4.5 trillion question

India sits at the centre of this story in a unique way.

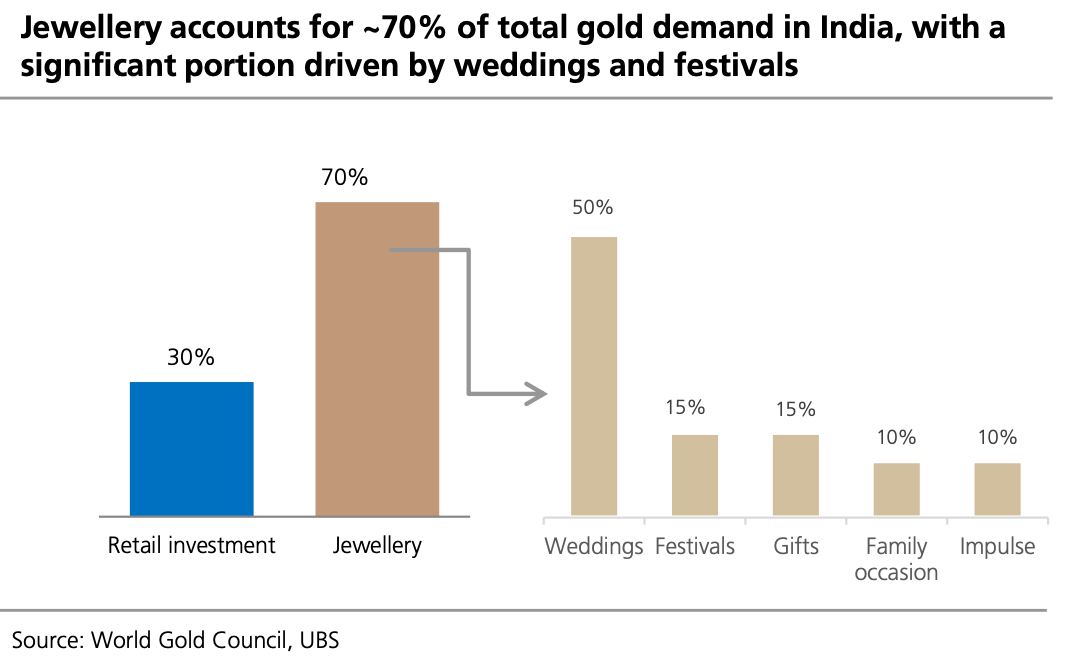

India holds the largest private stock of gold in the world. Between households, temples, and family vaults, Indians collectively own an estimated 28,000 tonnes. At current prices, this hoard is worth approximately $4.5 trillion, larger than India’s entire projected GDP of $4 trillion for FY2026.

Now, this isn't comparing apples to apples. GDP is annual economic output (a flow). Gold holdings are accumulated savings (a stock). But that's precisely the point. Generations of Indian families saved in gold, and that gold just doubled in value over two years.

This became a problem for the Indian government that issued its Sovereign Gold Bonds (SGB). Price increases meant, the Indian government’s liability increased dramatically i.e. average +79% from its issue price to ₹1.2tn ($13.3bn). With only 17 tonnes of gold redeemed out of 147 tonnes issued since 2015, the government stopped issuing new SGB tranches since Feb 2024. This bond was supposed to give the government easy money, with low (<3% annual interest cost) liability, but it quickly ballooned to become a $13bn liability (as of 2024) because the SGB value was pegged to the value of gold.

Other than stopping new SGB issuances, the government also recently added tax caveats to the earlier tax-free redemptions. As of the 2026 budget speech, only primary subscribers holding until full 8-year maturity retain tax-free capital gains status. Secondary market purchasers face 12.5% long-term capital gains tax without indexation, even if held to maturity.

And the retail investor entered this party too. As of January 2026, gold ETF inflows jumped 106% MoM to a record ₹24,040cr (~$2.65bn), slightly higher than equity mutual fund inflows of ₹24,029cr (~$2.65bn). Read that again. Gold ETFs beating equity mutual funds. That's a sentiment shift.

The wealth effect that doesn’t quite work

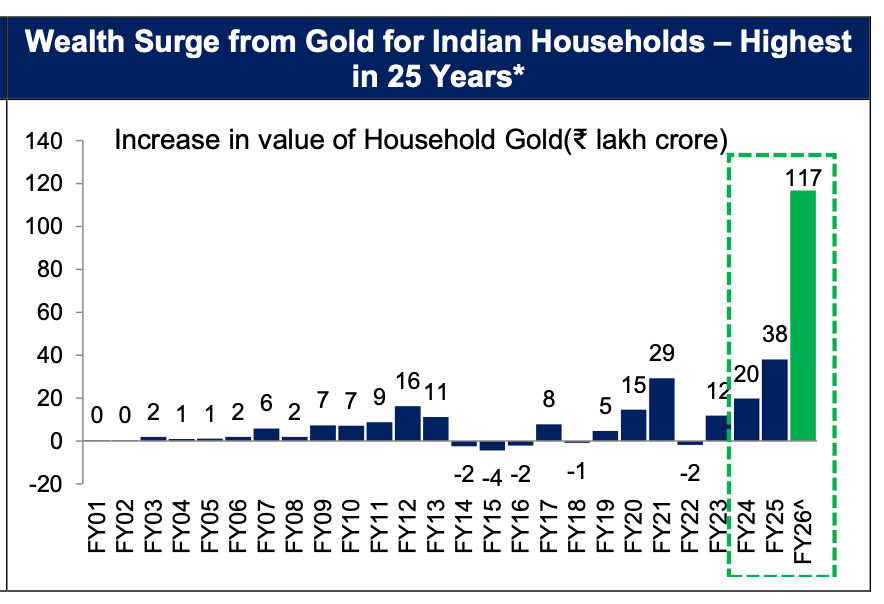

For Indian households that accumulated gold over decades at prices ranging from $300 to $1,500 per ounce, this represents a massive wealth gain. Every ₹1,000 per gram increase in gold prices adds nearly ₹1 lakh to average household wealth through mark-to-market gains.

But what’s strange is Indians aren’t selling. Unlike stock market rallies that often trigger consumption booms, gold price increases in India primarily expand credit capacity rather than spending. Gold in India isn’t just wealth, it’s insurance, inheritance, social security, and cultural identity rolled into one physical asset.

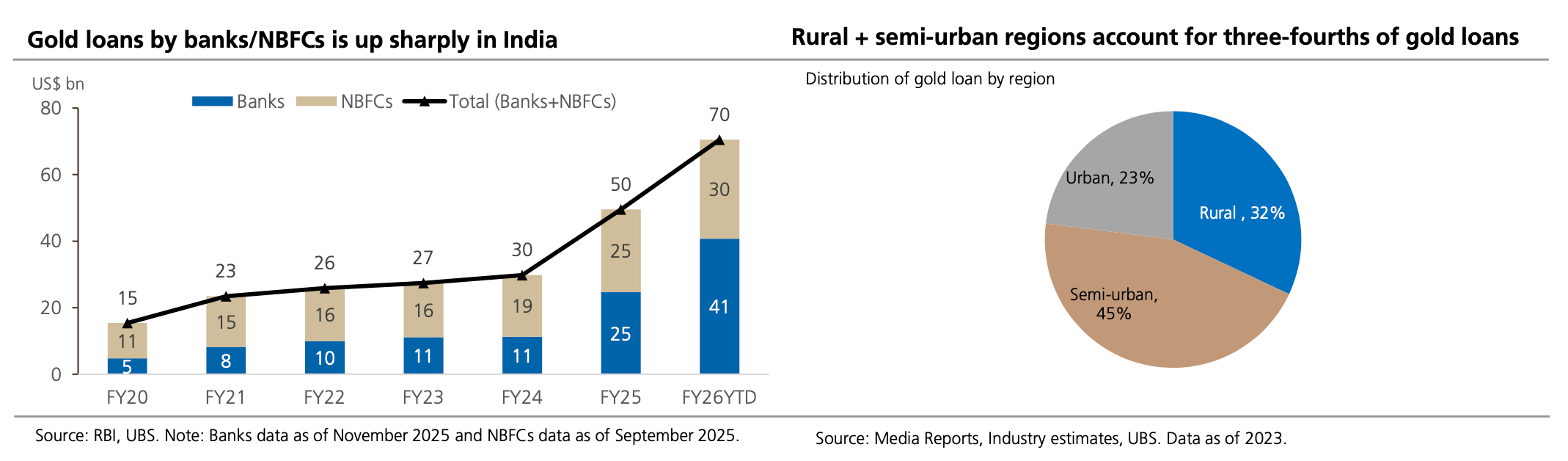

Loans against gold in the personal loan segment, grew 128% YoY and 86% FY YoY growth, reaching ₹3.83 lakh crore ($42.3bn). Borrowers are just able to borrow much more, even with limits on loan to value (LTV).

The banking sector is generally suffering from a problem of lower net interest margins (NIM), driven partially by the RBI’s clamp down on unsecured lending in 2023, which is why this gold price increase was an ideal scenario for banks to grow gold backed loans. The problem could be, if gold’s price swings the other way. Reductions in gold prices, could impact the loan-to-value of the gold backed loans, potentially causing issues for lenders.

This creates a liquidity multiplier throughout rural and semi-urban India. But it comes at a cost.

The import trap

India imports roughly 87% of its gold consumption. When gold prices rise, the import bill rises accordingly, assuming volumes stay constant, which they largely have. Indian demand for gold is remarkably price-inelastic. Weddings still need jewellery. Festivals still drive purchases. Cultural practices don’t adjust quickly to price signals.

The arithmetic is brutal: a 10% rise in global gold prices increases India's gold import bill by roughly 10%. All else equal, this can widen India's current account deficit by approximately 15 basis points of GDP. Higher gold prices mean more pressure on the rupee and more imported inflation.

This puts the Reserve Bank of India in an impossible position. High gold prices support household wealth and credit expansion (good for financial inclusion and growth). But they also strain the rupee and fuel inflation (bad for macroeconomic stability). The RBI can either defend the rupee by raising interest rates, or accept currency depreciation and support growth by keeping rates low. It can't do both.

The obvious question is: why not mobilise the $4.5tn already sitting in Indian households? The Gold Monetisation Scheme, launched in 2015 to let households deposit physical gold with banks and earn interest, has mobilised less than 30 tonnes (as of Nov, 2024) in over a decade. That's a rounding error on 28,000 tonnes of private holdings. Doesn’t seem like Indians want to melt down family jewellery, and face making charges (8-20% of value) that make the economics unattractive. Until someone solves for trust and incentive design, India's gold stays locked in family vaults, enormous latent value.

The currency layer: Dollar, Renminbi, and the fog ahead

Gold’s rise is a symptom of currency system stress. To understand where gold might be going, let’s understand that context.

The dollar dominated global finance since Bretton Woods in 1944 (for a detailed history, read Edition #91 - Trade and Tariffs), not because it’s inherently superior, but through network effects. Oil is priced in dollars. International trade is invoiced in dollars. Financial institutions settle through dollar-based systems like SWIFT. Today, the dollar is used in 88% of all foreign exchange transactions. If you’re a Thai company buying German machinery, you’ll probably pay in dollars even though neither country uses dollars domestically.

China’s challenge: slow but methodical

China isn’t being subtle about this anymore. In early 2026, Xi Jinping publicly called for building a “powerful currency” that achieves global reserve status, his most direct statement yet on challenging dollar dominance. Beijing has been laying the groundwork for over a decade: currency swap agreements with ~50 economies, RMB inclusion in the IMF’s Special Drawing Rights basket in 2016, oil trade settlements with Saudi Arabia in RMB, and the expansion of CIPS (Cross-Border Interbank Payment System) as an alternative to SWIFT, now linking ~4,800 banks across 185 countries. Through 2024-25, RMB’s share of global payments rose from around 2.0% to 4.7%.

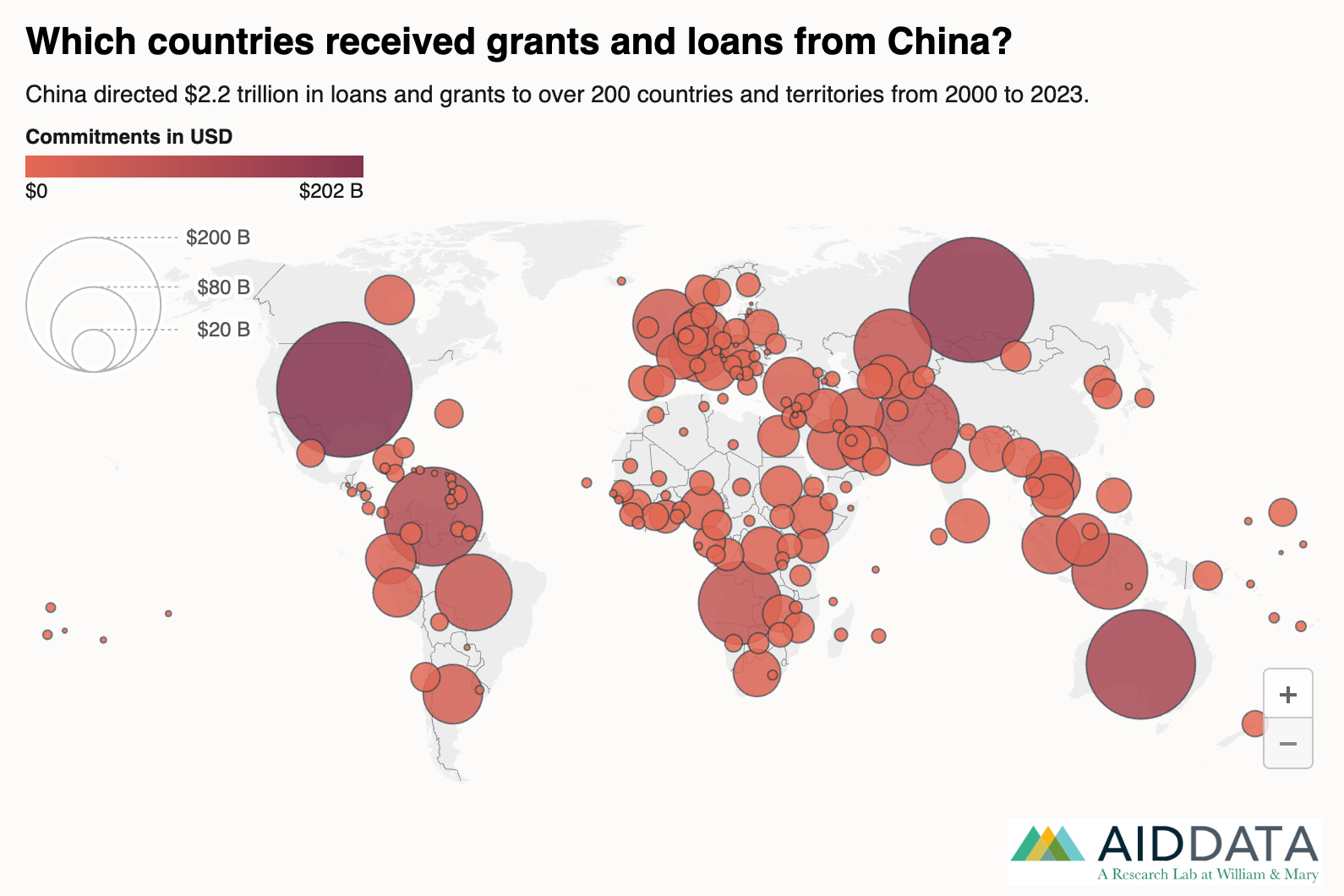

But the real ground work is in lending. According to AidData’s research, China has extended $2.2tn in loans and grants across 200 countries between 2000 and 2023, making it the world’s largest official creditor, outspending the US on a more than two-to-one basis and the World Bank by nearly $50 billion in 2023 alone. This isn’t charity. It’s infrastructure for influence. When you finance ports, railways, and power grids across 150+ countries with RMB-denominated loans, you create structural demand for your currency. The playbook isn’t new. The World Bank and IMF built dollar dependence across the developing world through the same mechanism for decades (read more, in Edition #86 - HDFC’s History). China is simply running the same play with different branding it seems. Here’s an insightful post on what will need to happen for China to have it’s way with being the reserve currency.

Despite all this, China faces fundamental barriers: capital controls that prevent deep liquid markets, an opaque and politically influenced legal system that creates a trust deficit, and convertibility restrictions that limit the RMB’s utility. As one analyst put it, Beijing’s immediate goal isn’t to replace the dollar overnight, it’s to build a “strategic counterweight that limits US leverage in a fracturing financial order.” And after watching Russia’s reserves get frozen, who trusts anyone’s digital currency system?

The Stablecoin Wild Card

Here’s where it gets interesting. There’s approximately $216 billion in stablecoins currently in circulation, with 95% pegged to the US dollar. These stablecoins hold reserves in US Treasury bonds, essentially dollar dominance 2.0, spreading dollar usage through blockchain rails rather than traditional banking infrastructure.

But the same infrastructure that enables dollar-pegged stablecoins can enable RMB-pegged or gold-backed stablecoins. If China launched a gold-backed digital yuan that could be held on any smartphone globally, suddenly the 85% of the world’s population that doesn’t live in “the West” would have an alternative to the dollar in their pocket.

China seems to be tightening its rules on stablecoins lately though.

The Unanswerable Question

Is dollar dominance eroding slowly over 20-30 years, or are we watching the early stages of rapid fragmentation into currency blocs? The slow scenario: the dollar’s share declines from 59% to 45% over a generation, volatility is manageable. The rapid scenario: a crisis causes sudden loss of confidence, trade fractures into blocs i.e. US/West (dollar), China/aligned (RMB), neutrals (maybe something else), and volatility is severe.

Gold’s behaviour suggests markets are pricing something closer to the second scenario. When gold rises despite high real yields and then crashes 9% in a single day before recovering, that’s not normal price discovery. That’s fear trading and forced liquidation.

Not sure if anyone knows which scenario plays out. That’s the honest answer.

What to watch

Three macro signals worth tracking: gold and equities falling simultaneously (forced liquidation, historically precedes funding winters) or credit spreads widening sharply (global credit tightening).

For India specifically: watch rupee volatility (sharp moves of 3-5% in a month signal stress), sustained FII outflows (three consecutive months above $5-7bn is a pattern shift), gold loan NPAs (a leading indicator of household stress despite on-paper wealth gains), and any sudden tightening of gold import duties back toward 15%+ (the current account deficit turning critical).

The only honest conclusion

This is confusing because multiple things are true simultaneously. Indian households are wealthier AND the economy is more vulnerable. Gold is a rational asset AND it signals systemic stress. There’s massive TAM unlocked AND a funding winter is likely. India benefits from geopolitical neutrality AND suffers from trade fragmentation.

These aren’t contradictions. They’re different facets of the same complex situation. And nobody has clean answers because this is the first time in 80 years the reserve currency system faces a serious challenge. Gold’s behaviour is unprecedented. India’s position is unique. The gold price crash showed that even professional traders don’t fully understand the dynamics.

For founders, investors, and finance executives, the answer isn’t “buy gold” or “avoid gold.” The answer is: operate with higher uncertainty buffers. Extend financial runways beyond what feels comfortable. Monitor macro signals, not just your internal metrics. Build flexibility into everything, fundraising timelines, hiring plans, treasury management, product roadmaps.

Gold at $5,000 isn’t the story. Gold behaving in ways it never has before, that’s the story. The rules that governed the global financial system for 80 years are under stress. Maybe they’ll hold. Maybe they’ll break. Maybe they’ll transform into something new.

There are just too many moving parts in our complex economic machine with controls for different parts in each passengers hand.

The weight of that gold bar isn’t just the weight of the metal. It’s the weight of uncertainty about the system itself.

What are you seeing in your corner of the market? I’d love to hear from you. DM me here.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🎵 Song on loop

Fintech updates can get boring, so here’s an earworm: Neat new band discovered this week: King Bee and the Stingers and their song Don’t Move so Fast (Spotify / Youtube). It’s a beautiful, soul, funk, blues, rock song - think raw harmonica, powerhouse vocals, and a rhythm section that won't let you sit still. Slow down, pay attention, don't move so fast. Felt right for this edition. :)

✨ Call outs

[AI Benchmark] N OF 1: What happens when you give an AI model a stock trading account and tell it to go wild and make you money? This benchmark is a great experiment in that direction. Fascinating to see how the models think, trade and win/lose money. h/t to reader and friend - Manan Agarwal.

[Report] Crisil and Oister report on alternate investment fund benchmarks. Good analysis and charts on the state of AIFs in India.

👋🏾 That’s all Folks

If you’ve made it this far - thanks! As always, you can always reach me at os@osborne.vc. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.

@Osborne Saldanha - very well summarized. What are your thoughts on launching gold backed stablecoin from GIFT city?