Correspondent Banking, OpenUSD, and Stablecoins | Fintech Inside #111 7th Jul, 2026

OpenUSD, the GENIUS Act, and the layer of banking nobody defends anymore. $300 billion says correspondent banking's slow decline just got a start date.

Hi Insiders, I’m Osborne, an investor in early stage startups.

Welcome to the 111th edition of Fintech Inside. Fintech Inside provides nuance and insight to the big trends shaping financial services. It’s the fintech newsletter for people who don’t have time to read five fintech newsletters.

For the last few decades, the world moved toward globalisation. People, capital, goods, services, technology, data - all of it flowed freely across borders. The assumption underneath most of it was that this flow was basically uni-directional and basically permanent.

That assumption is under real strain right now. And I think most of the fintech commentary on stablecoins is missing why.

This week’s edition is about correspondent banking, stablecoins, economics, sovereignty and what India is missing out on.

Thank you for supporting me and sticking around. Enjoy another satisfying week in fintech.

Considering angel investing? I get a bunch of fintech founders reaching out to me for investors. I’d be happy to put you in touch. Send me a DM here.

🤔 One Big Thought

The Slow Death of Correspondent Banking?

The swing back toward sovereignty

China spent two decades proving that a country can build its own internet, its own chip stack, its own AI models, largely walled off from the rest of the world’s infrastructure. That used to sound implausible. It doesn’t anymore.

The US has been making the same point from the other direction. Anthropic had to suspend access to its Fable and Mythos models on June 12 this year to comply with US Department of Commerce export controls, then restored access on July 1 once those controls were lifted. Whatever you think of the policy itself, the mechanism is the point: the US government demonstrated, in real time, that it’s willing to use export controls to decide who gets access to their frontier technology. Can’t remember the last time this happened. Technology sovereignty isn’t just a Chinese project anymore. It’s a live lever.

Data sovereignty has followed the same arc, data localisation laws and data residency requirements have gone from a niche India/EU concern a decade ago to fairly standard practice across most large economies today.

Which brings us to the layer underneath all of those: capital.

This is where things move at a much slower, much less visible pace. On the surface, there’s been a lot of noise - sovereign wealth funds getting more assertive, reserve currency diversification, tariff fights, the odd tax skirmish. Underneath, actual capital sovereignty is glacial, because money is the most globally interconnected thing we have, and the switching costs are complex and enormous.

But watch the two biggest economies play the same game from opposite ends.

China has spent over two decades building demand for the renminbi the slow way (see Edition #102): financing ports, railways and power grids across 150+ countries, mostly through RMB-denominated loans, currency swap lines with roughly 50 economies, oil settled in RMB with Saudi Arabia, its own SWIFT alternative (CIPS) now linking close to 4,800 banks across 185 countries. It isn’t subtle about the goal either, Xi Jinping has publicly called for building a “powerful currency” with global reserve status. I’ve written in Edition #105, how Ant Group is going global by following Chinese global citizens - travellers and immigrants.

The US, meanwhile, tried something more direct and blunter: a provision in last year’s tax bill, nicknamed the “revenge tax,” that would have raised US taxes on investors from countries with tax regimes it considered unfair to American companies. It was dropped within weeks after a G7 deal, so it never became law. But the fact that a G20 economy floated using access to its own capital markets as retaliatory leverage tells you where the appetite is right now, law or no law.

And then there’s the GENIUS Act, which is where this gets genuinely counterintuitive.

The GENIUS Act is US domestic legislation. It regulates who can issue a compliant dollar stablecoin inside the US and what has to back it. On paper, it has nothing to do with any other country’s monetary sovereignty. In practice, it’s arguably the single most effective de-dollarisation defence mechanism the US has built in years — because a well-regulated, dollar-backed stablecoin is exactly the kind of instrument an emerging market’s businesses and citizens reach for the moment their own currency wobbles. US Treasury Secretary Scott Bessent has said as much, plainly: stablecoins are a tool to keep the dollar dominant. A country can launch its own stablecoin, feel like it’s building sovereign digital infrastructure, and still end up more dollarised than before, because the stablecoin sitting on top of that infrastructure is backed by dollars either way.

That’s the paradox worth sitting with. Everyone is fighting for sovereignty, over technology, over data, over capital. And a loosely effective countermove any single country has found so far isn’t a wall. It’s a stablecoin.

Which is exactly the terrain India has been standing on for a while, without fully realising it.

UPI proved something the world needed to see

UPI showed that instant, real-time settlement is not just possible, it’s the right default for a mobile-first world where plastic cards were never going to matter the way they did in the US or Europe. That’s a genuine, undersold achievement, India built the payments rail the rest of the world is still catching up to.

But exporting UPI has been a slow, country-by-country slog. Bilateral agreements, one regulator at a time, one central bank relationship at a time. It’s real progress, but it hasn’t yet found the kind of traction that turns a domestic rail into global default infrastructure. And in a world where sovereignty over money is suddenly back on the table for everyone, that slow pace is starting to look like a cost, not just a rollout detail.

Which is what makes the recently launched OpenUSD worth paying close attention to right now.

First, what OpenUSD actually is

On June 30, an entity called Open Standard announced OpenUSD (ticker: OUSD), a stablecoin, backed by more than 140 businesses, which is an unusually broad coalition for anything in this space. The list is worth sitting with for a second: Visa, Stripe, Mastercard, Amex, BlackRock, BNY, Standard Chartered, Coinbase, Shopify, DoorDash, Google, Samsung. Payment networks, global banks, big tech, and crypto infrastructure, all on the same cap table.

When National Payments Corporation of India (NPCI) was formed it was promoted by a consortium of public and private sector banks in the country. The ten core promoter banks include the following entities - State Bank of India, Canara Bank, Punjab National Bank, Union Bank of India, Bank of Baroda, Bank of India, HDFC Bank, ICICI Bank, HSBC, Citibank.

Open Standard is the NPCI of USD stablecoins.

Three design choices separate OUSD from existing stablecoins like USDT and USDC:

No fees, no volume caps: Businesses can mint and redeem Open USD at no cost, with no artificial ceiling on volume, a direct jab at the mint/redeem fees that make existing stablecoins expensive at scale.

Partners keep the yield: Reserve earnings flow back to the partners, minus a small fee to run the thing, instead of being captured entirely by the issuer the way they are with Tether or Circle today.

Nobody owns it: It’s run by an independent company with a board made up of its partners, not a single issuer calling the shots.

On the surface, it seems like this isn’t Stripe launching a stablecoin. It’s Stripe, Visa, Mastercard, and 140 others agreeing that no single company should own the rails everyone plans to build on. OpenUSD goes live later this year (2026).

That’s the news. Here’s why it matters more than it looks.

Stablecoins stopped being a crypto story

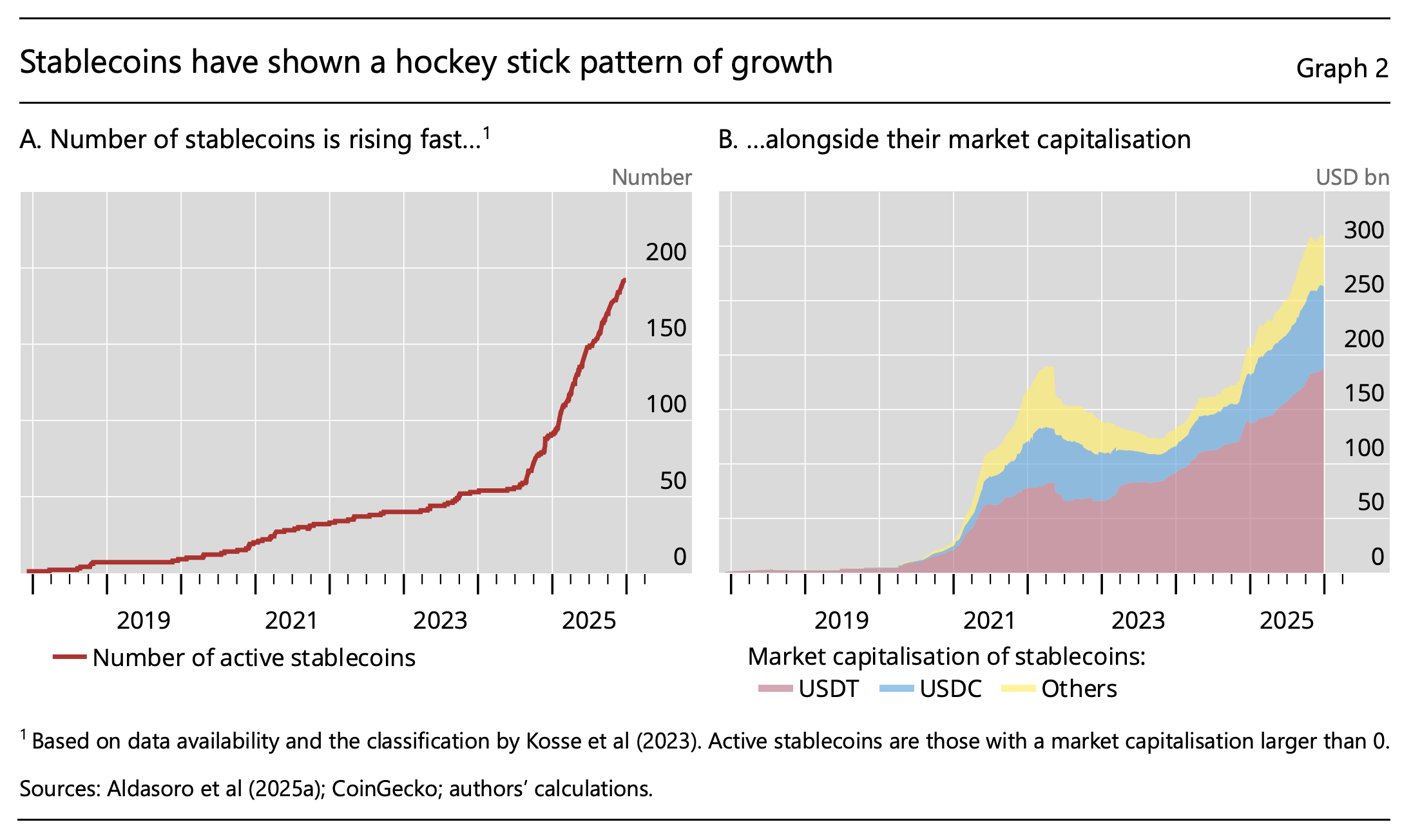

Zoom out from OpenUSD and look at the last eighteen months. Stripe acquired Bridge. PayPal launched PYUSD. Visa and Mastercard are wiring stablecoin settlement into their networks. Coinbase, Robinhood, and Circle keep expanding stablecoin products. This is consensus, not a coincidence.

The global stablecoin market crossed $310–320bn, more than doubling in under two years. That’s now larger than the foreign exchange reserves of over 90 countries, including developed economies like the UK and Canada. BNY’s own product chief recently projected the category could reach $1.5tn by 2030.

Five years ago, “stablecoin” meant one thing: crypto trading. Today it means cross-border payroll, treasury management, B2B settlement, remittances, and increasingly, the rails AI agents will use to transact with each other. The use case moved from speculation to infrastructure, and most of traditional finance is not noticing the shift happen in real time.

You don’t have to take anyone’s word for it. The market already voted with $300bn.

Here’s the piece of evidence I think is the most underrated in all this, and it isn’t from a central bank at all. It’s from Wall Street’s own reaction to the GENIUS Act actually passing.

A March 2026 IMF working paper did something clever: instead of asking economists what they think stablecoins will do to payments, the authors watched what investors actually did with their money in the ten trading hours around the decisive House vote on the GENIUS Act, on July 17, 2025. Comparing listed payment firms to the rest of the financial sector, and correcting for how much the market had already priced in beforehand, they estimate the vote wiped out 18% of incumbent payment firms’ market value i.e. roughly $300 billion. That’s a bigger hit than the market impact of the Durbin Amendment (debit card fee caps) or the ECB’s digital euro announcement on US firms, the two benchmark “stablecoins are disruptive” precedents people cited before this paper existed.

The part that matters more than the headline number is where the damage concentrated. Firms whose primary business is cross-border payments got hit hardest with an estimated 27% wipeout, more than double the sector average. Firms with strong existing network effects (Visa, Mastercard, the card networks) saw no significant hit at all. Neither did firms that had already engaged with crypto assets before the vote i.e. PayPal, Block, Fiserv. The market isn’t betting that stablecoins destroy payments broadly. It’s betting they gut the slow, expensive correspondent-banking layer specifically, while leaving network-effect moats and early movers largely untouched.

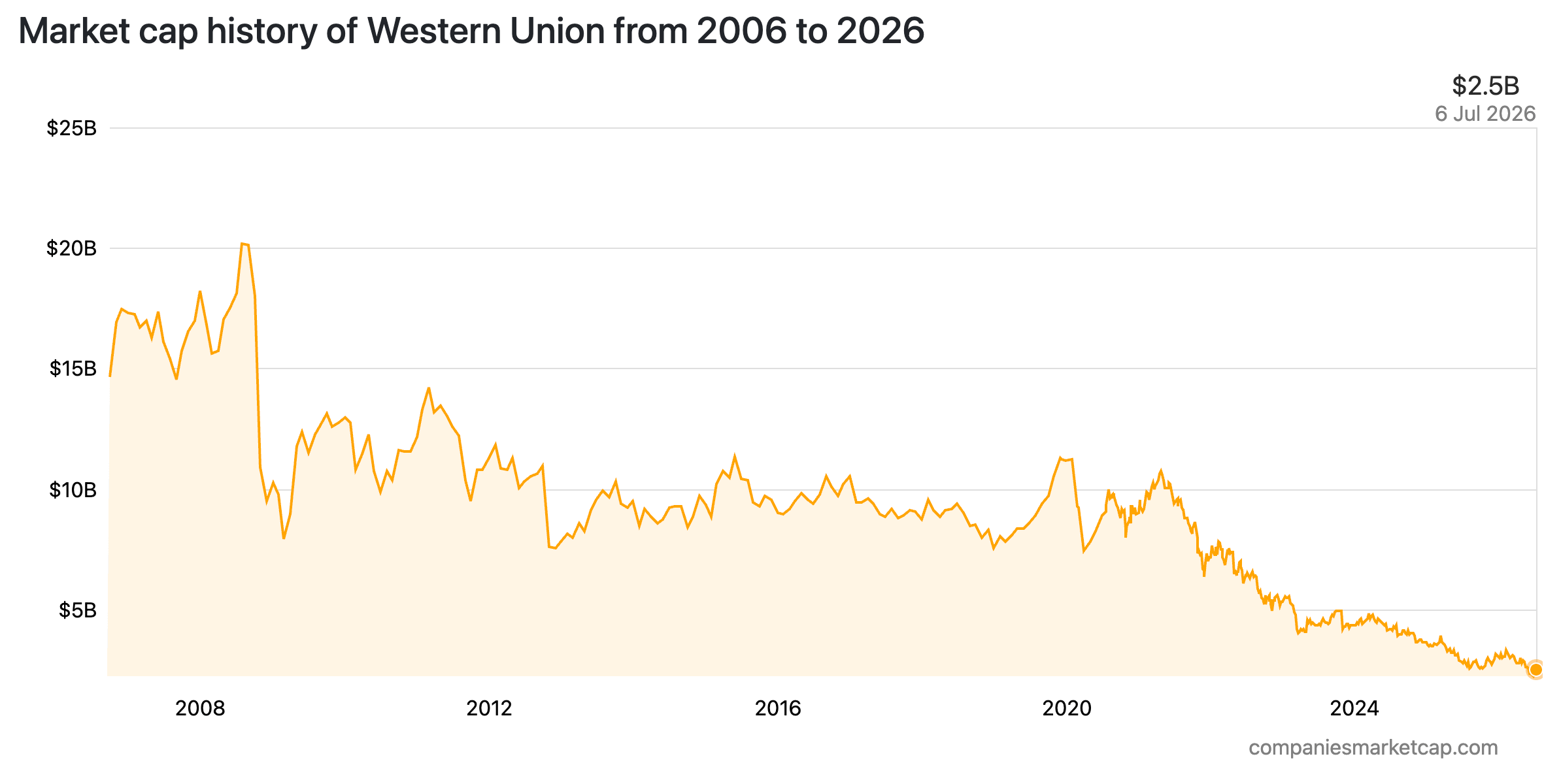

You can watch this prediction play out in real time. Western Union, about as pure a cross-border correspondent as exists, announced in October 2025 that it would launch its own stablecoin. Its own earnings calls tell the story of a company changing its mind in real time: in May 2025, before the Act passed, a Western Union executive was calling stablecoin economics “operationally challenging and expensive.” By July, weeks after the Act passed, the same company was “actively revising our position” with a “clear regulatory framework and guaranteed redemption value.” Same company, same underlying technology, completely different posture, the only thing that changed was the law.

Worth sitting with for a second: UPI’s dominance inside India functions a lot like Visa’s network effect inside the US. If the market’s read is right, that’s exactly the kind of moat that holds up against stablecoin competition. The exposure isn’t to UPI as a domestic system. It’s to whatever tries to move money across India’s borders the old, slow way.

Stablecoins to disrupt correspondent banking?

While the US companies and regulators are focussed on launching standards, regulations and products for stablecoins and crypto, the global institutions it manages, seem to have the opposite view.

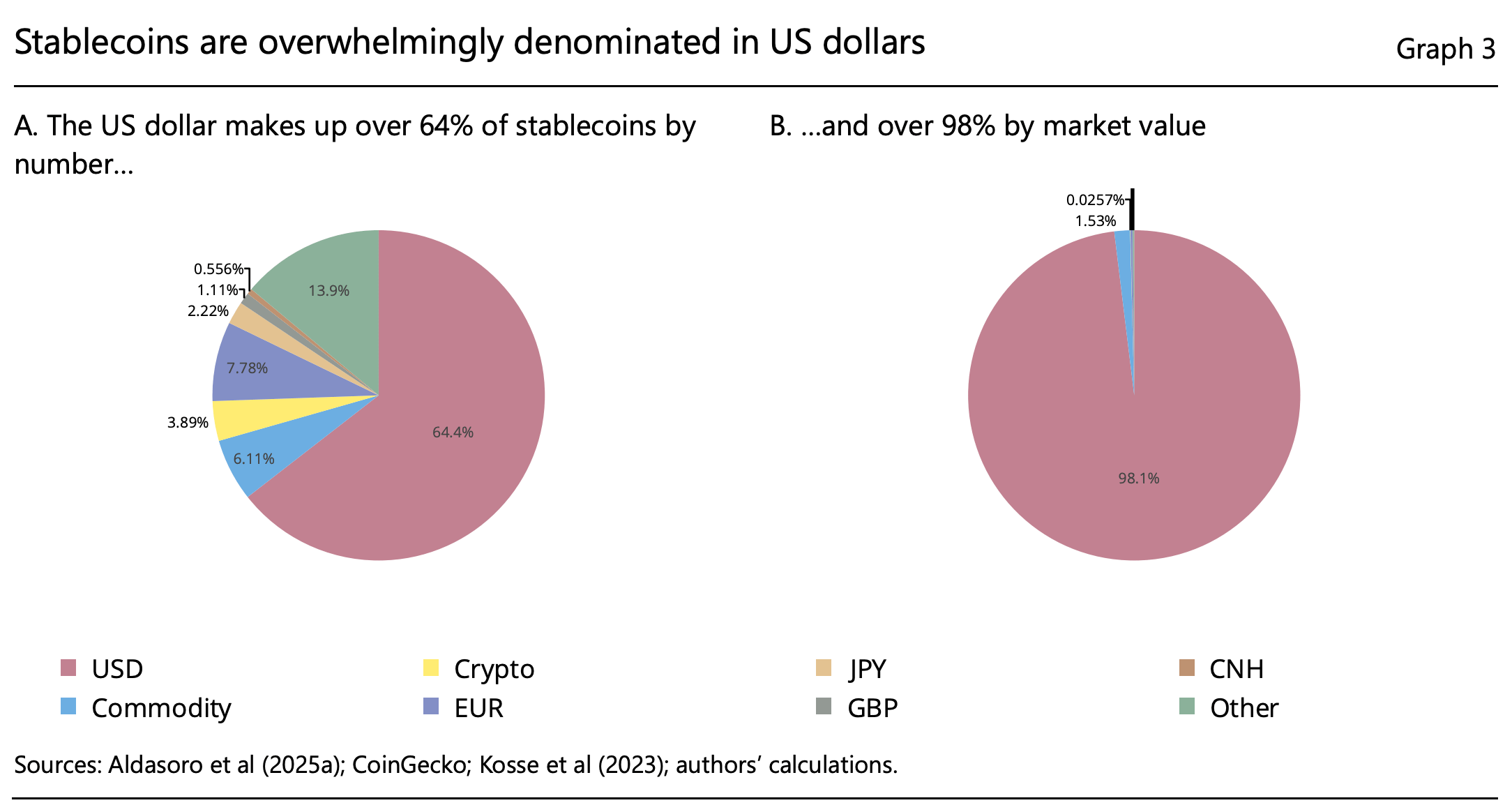

According to the Bank for International Settlements’ 2026 Annual Economic Report, 99.4% of all fiat-backed stablecoin value is now denominated in US dollars. Every other currency combined accounts for the remaining 0.6%. That’s near-total dominance.

On June 28 2026, the BIS went further, formally declaring that stablecoins fail the basic tests of money i.e. singleness, elasticity, interoperability, and warned explicitly about “digital dollarisation,” the risk that dollar-denominated stablecoins become the default cross-border infrastructure for emerging markets, quietly weakening their monetary sovereignty in the process.

That’s a strong statement from the central bank of central banks. It reads less like commentary and more like a line being drawn.

Why this matters beyond crypto

Strip away the crypto framing for a second, because I think that’s what’s making this hard to see clearly.

This debate isn’t really about crypto. It’s about whether the next generation of internet-native businesses settles in dollars by default, simply because dollars are the easiest rail available.

Picture an AI agent paying another AI agent for compute, data, products, services etc, with no human in the loop to pick a currency. Picture a SaaS platform paying out thousands of creators or gig workers across a dozen countries in one settlement run. Picture a marketplace clearing merchants across twenty countries overnight instead of over days.

None of these care about correspondent banking relationships. None of them are going to route around a currency because a central bank prefers a different rail. They care about whichever settlement layer is easiest to plug into. Right now, that’s overwhelmingly dollar rails. Every one of these use cases is a small vote for that status quo, and there are going to be a lot more of them, a lot sooner than most central banks are planning for.

The great paradox

What’s fascinating here is that no single institution designed this outcome.

The BIS worries about financial stability. The IMF worries about monetary sovereignty. Stripe wants easier internet payments. BlackRock and BNY want to serve institutional demand for tokenised dollar exposure. The US Treasury quietly benefits from anything that extends dollar reach without it having to do anything at all.

Different institutions, different objectives. And yet all of it reinforces the same outcome: a more internet-native dollar, whether anyone intended that or not. That’s a more interesting story than “America wins.” Nobody planned this. It’s just what happens when everyone’s separate incentives point in the same direction.

Three different answers to the same question

Strip away the noise and three governments are running three different experiments on the exact same problem, how do you keep control of money as it goes digital, when the best available technology is being built somewhere else?

America’s answer is private stablecoins, regulated just enough to be trusted, precisely because a trusted dollar stablecoin is the best de-dollarisation defence the US could have built. Europe’s answer, under MiCA, is regulated private money deliberately steered toward the euro rather than the dollar — the BIS calls this a live test case for whether a “domestic currency integration” path can actually work. China’s answer is neither: an outright ban on crypto and stablecoin trading, reasserted as recently as February 2026, paired with the e-CNY as the state-backed alternative. Three different bets on the same underlying question, none of them proven yet.

Back to India and why “just export UPI” isn’t a full answer anymore

India is not the only country facing this. Indonesia, Brazil, Nigeria, Mexico, Turkey, and Vietnam are all sitting on some version of the same tension - real-time domestic rails that work brilliantly at home, and a much harder, much slower path to making that infrastructure matter beyond their own borders. India just happens to be the sharpest example, because it also built Aadhaar, DigiLocker, and the Account Aggregator framework alongside UPI, arguably the best public digital infrastructure stack anywhere.

But now, where the rest of the world’s private sector ran toward stablecoins, India, like most large emerging economies, leaned toward CBDCs instead. Different philosophy, same underlying question every one of these countries is quietly asking: how do you keep control of money as it goes digital, when the alternative infrastructure is being built by companies you don’t regulate, sitting inside a country whose regulators just showed they’re willing to switch access on and off?

UPI was built for Indian bank accounts, Indian regulators, Indian settlement rails, Indian identity infrastructure. The internet has none of those defaults, and increasingly, when a developer somewhere else needs to plug into a settlement rail, the honest, easiest answer is a dollar stablecoin, not a domestic real-time payments system, however good that system is.

Here’s where I want to correct something I nearly got wrong in an earlier draft of this piece, because it’s a genuinely important nuance, and it comes straight from the RBI rather than from me. It’s tempting to frame this as “India just needs its own rupee stablecoin.” RBI Deputy Governor T Rabi Sankar gave a keynote at BIS in December 2025 that closes that door explicitly, and it’s worth relaying accurately.

His argument: stablecoins fail the basic tests of money. They’re not fiat, they’re not “single” (there could be hundreds of competing private monies instead of one trusted one), and there’s no guarantee the issuer’s promise to redeem at par is even a legal liability. On every claimed benefit i.e. cross-border efficiency, financial inclusion, bridging crypto to the real economy, he argues India’s existing rails (UPI, RTGS, NEFT) already deliver it better, without the risks of currency substitution, capital account leakage, bank disintermediation, and a quiet transfer of seigniorage (the profit a government normally earns from issuing its own currency) to private stablecoin issuers, most of them foreign.

And crucially, he rejects the “just make it a rupee-denominated stablecoin” compromise too. In his view, a domestic-currency stablecoin still carries the currency-substitution, disintermediation and seigniorage risks, it isn’t the foreign-currency exposure that’s the core problem, it’s the private issuance itself. As he put it, the bigger threat is a stablecoin that works well.

India’s actual stated strategy has four pillars: preserve trust in the rupee and the existing payment system, safeguard monetary sovereignty, push CBDC adoption and cross-border CBDC corridors, and interlink India’s fast payment systems directly with partner countries rather than build a private alternative on top. That’s a real, coherent bet, not a policy vacuum waiting for a stablecoin to fill it.

Worth noting separately: India already has a functioning compliance apparatus for crypto activity regardless of where the stablecoin debate lands. Since 2026, exchanges and wallet providers dealing in virtual digital assets have been brought under the same anti-money-laundering law that governs banks, KYC, suspicious transaction reporting, the works. So “India has no rules for this” isn’t quite right. The AML plumbing exists. The monetary policy question is the one still being fought over.

The same open question i.e. CBDC and FPS interlinking versus some form of private digital rail, applies just as directly to the real, the rupiah, the naira, and the lira, even where those central banks haven’t stated a position as clearly as India has.

So what should emerging markets actually do?

I don’t think there’s one clean answer, and I’d be suspicious of anyone who claims there is. The BIS’s own research sketches out why this is a live, unresolved question rather than a settled one. Researchers there lay out three scenarios for where this goes: stablecoins stay a niche crypto-trading tool with limited real-world adoption; stablecoins become the de facto cross-border payment rail across emerging markets, with real damage to monetary policy and capital controls; or countries successfully build regulated domestic-currency stablecoins that interoperate with existing payment rails and CBDCs, capturing the efficiency gains without the sovereignty costs. They’re honest that the third path requires more regulatory capacity than most emerging markets currently have.

India’s bet i.e. CBDC plus interlinked fast payment systems, no private stablecoin at all, sidesteps that capacity problem entirely by not needing it. Whether that wins depends on whether CBDCs can move as fast internationally as private capital and developer tooling move by default. That’s not a question any single regulator can answer alone, and if the market’s repricing of Western Union is any signal, the companies that actually move money across borders may answer it faster than the regulators do.

The goal isn’t chasing crypto for its own sake. The goal is making sure local currencies stay relevant on rails that are increasingly internet-native by default, not government-native.

The bigger point

Every era gets the monetary infrastructure it builds for itself. The Bretton Woods era ran on correspondent banking and fixed exchange arrangements. The internet era is going to run on programmable money, and the standard-setting for that infrastructure, OpenUSD being the latest example, is happening right now, largely outside any emerging market’s control.

India has already proven that a government can build digital public infrastructure that rivals, arguably beats, anything the private sector has shipped elsewhere. That was the first payments revolution, and India won it decisively, the same way a handful of other emerging economies won their own versions of it.

The next one is a different contest. It’s no longer about building the best domestic payments system. It’s about building, or choosing, the monetary infrastructure the rest of the internet decides to use by default, especially the part that moves money across borders, which is exactly where the market’s own $300bn repricing says the pressure is landing first. UPI isn’t going anywhere at home. The real question is whether the rupee, and its equivalents elsewhere, become native to that internet on their own terms, or whether the internet just quietly transacts in someone else’s digital currency instead, the way most cross-border flows already quietly do, without anyone noticing it happened.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🎵 Song on Loop

Good background songs to listen as you read Fintech Inside: This weekend I was at a bar and I heard a song I hadn’t heard since college - Black Betty by Ram Jam (Spotify / Youtube). Full nostalgia trip. Enjoy! 🎶

✨ Call Outs

[Video] AI x FinTech: Voice, Agents & Year 1 in a Decade of Change | SummitUp by Elevation

[Product] Wiretap.us - use AI to scan social media for mentions of your brand

[Video] How to build a full body ultrasound

[Video] The Truth about Space Data Centers

[Book] What I learned about investing from Darwin

👋🏾 That’s All Folks

If you’ve made it this far - thanks! As always, you can always reach me via DM at osborne.vc/dm. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.

Hi Osborne,

Great to connect! I've been following your work through Fintech Inside and really enjoy your insights on the fintech ecosystem, especially your perspectives on India's evolving financial landscape and startup ecosystem.

I also write about fintech, digital banking, crypto, blockchain, and payments. I've subscribed to Fintech Inside and look forward to learning from your content.

I'd love for us to support each other's work by engaging with our posts. If there's an opportunity to collaborate in the future, I'd be happy to explore it.

Looking forward to staying connected!

The systems that enabled unprecedented wealth creation open markets, fast capital flows, global connectivity are now being exploited at scale.

This is a moment of exposure. Financial networks, supply chains, and digital platforms are increasingly interlinked, creating risk vectors that move faster than traditional oversight can keep pace with. The question is no longer whether disruption will occur, but how prepared your systems are to absorb and respond to it.

The path forward demands decisive action: invest in AI-driven risk intelligence, ensure full transparency across asset flows, strengthen cross-border compliance architectures, and actively participate in building real-time information-sharing ecosystems with regulators and partners. Act now to build resilience. It is no longer a defensive strategy; it is a core requirement for preserving capital and influence in a system under pressure.

Act early to protect your assets and help shape the emerging financial order. Delay, and you will face a system where control has already shifted.