Credit Card on UPI | Fintech Inside - Edition #63 - 13th June, 2022

In this edition: details on RBI's recent proposal of credit card on UPI. What it means for the fintech ecosystem, credit card adoption, merchant acquiring and more.

Hi Insiders, Osborne here.

Welcome to the 63rd edition of Fintech Inside. Fintech Inside is the front page of Fintech in emerging markets.

Recently RBI, the Indian central bank, proposed linking credit cards with UPI. This is a big deal and will have impact on credit card adoption, merchant acquiring, bank and NBFC products and many more. This week's edition is about Credit Card on UPI - the next big thing!

The edition ended up becoming very detailed and covers a bunch of topics. Tried to make this very comprehensive and so couldn't cover other topics which I also wanted to cover - more on BNPL, Apple's pay later and others. Will do so in the next edition!

If you're building in fintech or have an idea that you'd like to riff on, I'd love to speak with you. Write to me at connect@osborne.vc.

Enjoy another week in fintech!

🤔 One Big Thought

The Next Big Thing - Credit Cards on UPI

"The most complex problems often have the simplest solutions".

At its latest Monetary Policy Committee (MPC) meeting, the Reserve Bank of India (RBI), India's central bank, proposed to link credit cards with UPI. For a while now, the industry has requested UPI to have credit rails as well, to further increase credit penetration in the country. To cope with the regulatory uncertainty, the industry has largely resorted to very complex implementations (e.g. just-in-time credit cards) or half broken solutions so far.

IMO, this proposed implementation of credit cards on UPI is a simple and elegant solution. It's simple because there's no reinvention required, no complex implementation required, no separate regulation required, nada. It's elegant because it satisfies the requirement of virtually every stakeholder in this stack of credit based payments. Of course there are kinks or details to be ironed out and that will happen in time.

What is credit cards on UPI? For that, let's first understand what UPI is.

Unified Payments Interface (UPI) is an instant payments system. Think of UPI as a "pipe" that enables transfer of value from the entity paying (user or merchant) to the entity receiving (user or merchant) money. This "pipe", so far, has facilitated the transfer of money from a user's pre-funded bank account to that of the receivers. A UPI handle can be linked to multiple bank accounts from which a user can pay with.

UPI is all about convenience. With UPI, the sender only needs to know the receivers mobile number or UPI handle (e.g. firstname@bankhandle). It usually takes me less than 15 seconds to make a successful UPI payment. Only cash has better "time to money"! UPI is so simple and convenient that within 6 years since launch, it now (as of May, 2022) boasts of 260+mm unique users, 60+mm merchants, ~185mm QR acceptance points and a network of 323 banks. The UPI network processes ~6bn transactions worth $135bn in value per month! That's enviable scale! It is also important to know that UPI is free - as in there is no cost for the user while paying nor the merchant while accepting payments.

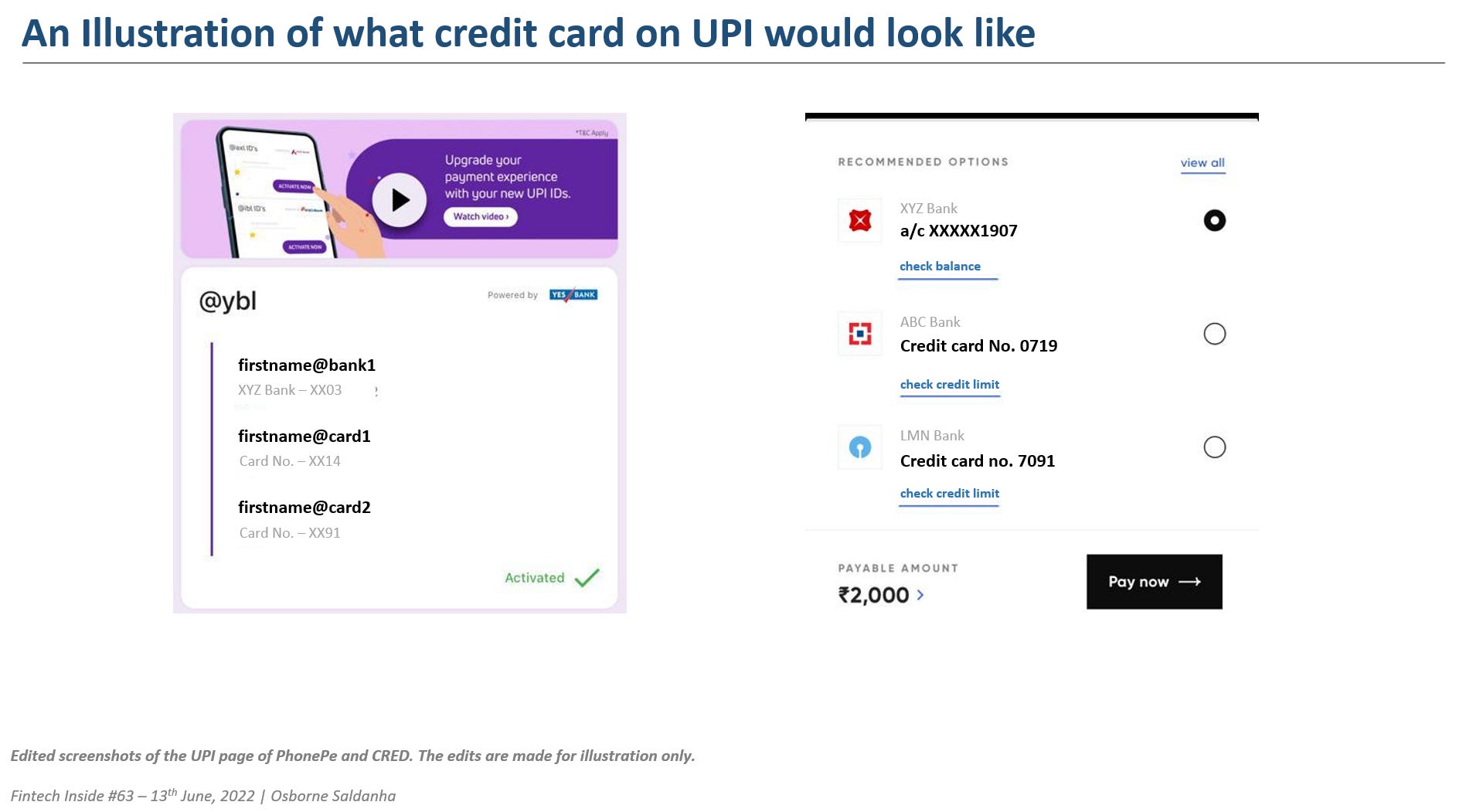

Credit card on UPI is basically adding another "input" in the "pipe" to transfer value. Basically, along with a pre-funded bank account, a UPI handle can also be linked to a credit card. There will be pre-funded and credit based payments on UPI. With credit card on UPI, users can pay at a merchant by scanning their QR code, selecting credit card and paying with credit. An implementation could look like below:

The big caveat about the current proposed implementation of credit card on UPI is that in the first phase, only RuPay credit cards will be linked with UPI. RuPay, launched in 2014, is a homegrown card payment network, just like Visa, Mastercard, Diners Club and others. Some news reports claim that 10-15% of all new cards issued are on RuPay but and RuPay credit cards account for less than 5% of transaction value. It has a few million credit cards in circulation accounting for less than 20% market share. The RBI is expected to open up credit cards on UPI to other card networks too. Oh also, RuPay debit cards are free as well (credit cards have some low MDR).

Why is credit card on UPI the next big thing:

Cards have seen limited innovation since invention in 1960's: physical card form factor has been largely the same since invention. That's also because it just works. But in digital world there are some challenges - storage, tokenisation, hacks etc. etc. Credit Cards on UPI solves for a lot of those worries and UPI has proved to work well on mobile devices irrespective of device type, network type and more.

POS device distribution is not scalable: POS device is the big brick you stick your card into to make your payment.

Better risk management: As mentioned, credit cards just work. The ecosystem is clear on unit economics, risk management is well understood, underwriting is standardised, card outstanding statements run like clockwork and collections is figured out. The form factor of using a credit card is all that changes - everything else remains the same.

Requirements of all stakeholders in the stack are addressed: RBI is the most important stakeholder here and their concern of risk and education is addressed here. Personal loans cause the regulator anxiety as it is easy to disburse but very tough to collect. Merchants are happy as credit helps them sell more and with higher cart size. Users get to use credit at checkout. Financial firms facilitating the transaction also benefit.

Familiar interface will drive adoption: UPI is familiar and credit card is familiar. The combination makes paying with credit a breeze. This familiarity and trust will help users demand credit cards which in turn will drive adoption.

Credit card is a consumption payment products: Have sort of addressed this above, with credit cards, the loan is transferred directly to the merchants (receivers) account. The credit card is used at the point of sale. Personal loans are transferred into the bank account of the user (borrower). The borrower can use it for non-productive/consumption needs as well. This is a big difference between the two which makes credit cards on UPI much less riskier than credit on UPI.

The success of credit card on UPI depends on a few things:

a. Increasing credit cards in circulation: There are ~75mm (Apr, 2022) credit cards in circulation but only 30-35mm unique credit card users. In Apr, 2022, these 75mm credit cards reported a cumulative monthly spend of $14bn, compared to 920mm debit cards with cumulative monthly spends $8.7bn (the spends numbers don't include cash withdrawals at ATM or POS). Some reports estimate that credit card spends could grow at a CAGR of 22% FY22-26 to reach $285bn. For that to happen, the number of credit cards in circulation needs to improve significantly and cover a larger portion of the population. Only with a credit card, will a user able to use credit card on UPI.

b. Merchant opt in for MDR: To explain this part, let's first understand how a credit card company makes money.

A credit card company largely has two income sources. There are other sources as well, but it's 5-7% of overall revenue, as you'll see later on.

Interest income: Income from charging interest of 2.5%-3.5% per month to users after the 30-45 day interest-free period. This is typically charged to "revolver" customers who do not pay the entire credit card statement outstanding at the end of the interest free period.

Fees and commission income: This revenue stream includes commission income from the payment made at POS by charging the merchant and income from late fees, penalties etc charged to the user.

The fee income is an important source of revenue as 99% of spends on a credit card happen at POS/online (1% is withdrawn as cash) and the issuer (credit card company) is taking risk on you (credit card user) every time you swipe your card. 19% of debit card spends happen at POS/Online, rest is withdrawn as cash. As illustrated in Edition #58 (Nuts and Bolts of Payments), of the roughly 2% Merchant Discount Rate (MDR) charged to the merchant on the transaction value, a large portion (~60%) of it goes to the credit card company.

Let's take the example of SBI Card, the credit card subsidiary of SBI Bank (India's largest bank) and the only listed credit card company. For Q4FY22 (Jan-Mar 2022), out of total revenue from operations of $380mm (INR 2,850 cr), it made 44% from interest income, 50% from fees and commissions and 6% from others (insurance cross sell, incentives etc.). 50% from charging MDR to merchants and other fees to users! There's a lot more fascinating information on the credit card industry in this quarterly earnings presentation.

Another example of how important credit cards are in the payment flow is the priority stacking of payment options at the time of checkout. Cards are up top across payment gateways!

All this is to say that MDR is important in the credit card ecosystem. There's no getting away from MDR. The question of who bears the cost of MDR should, IMO, be left up to the ecosystem. RBI and the government should not make this free, which if done, will not help credit cards on UPI succeed.

IMO, the status quo should be maintained and MDR should be borne by the merchants, if they so choose to opt in to accept credit cards on UPI. Of the total 30-40mm merchants that accept UPI/QR, even if 10% accept, that's a big win.

c. Consumer education around credit being used as a payment product: The infamous Jamtara UPI scams are well known, so much so that there's a whole Netflix show about it. Many users have been ripped off of millions of dollars via these scams, in part, thanks to UPI's convenience and "presenceless" features. Now, layer on credit and the issue could become much worse. There's a scary dark pattern in some fintech apps as pointed out by Chandra Ramanujan where the pre-funded account and credit account are clubbed together at the point of checkout. Without proper consumer awareness and education, this product can be misused and mis-represented for various reasons. The user can easily end up with a pile of credit outstanding that they will not want to pay back, or worse, a bad credit score. With ease of disbursal comes difficulty in collections. This is my biggest worry with credit card on UPI and implementation and awareness campaigns could potentially address it.

How will this impact Banks, NBFC's and fintech startups? Credit card on UPI further enforces the position of banks and NBFC's as central to payment flows. Banks were initially made central to UPI as well. So, there's nothing changing that with credit card on UPI. The more interesting update is RBI potentially allowing NBFC's to issue credit cards. This could potentially mean that fintech startups with an NBFC license could issue their own credit cards. Fintech startups being able to issue their own credit cards along with the UPI linking will mean a lot of innovation. But, and this is a decent sized but, RBI will conditionally take specific applications for credit card issuance approvals only from NBFC's with minimum capital of INR 100 cr ($13.3mm). This requirement keeps out the smaller fintech startups that may not have that much capital. This is the first real opportunity to make money out of UPI, an opportunity that has not existed for over six years since UPI's launch. Bank's and larger NBFC's aren't going to give this opportunity away so easy.

I'm very excited about credit cards on UPI and how new products can be created, as distribution is largely solved for. If I may be so bold, I think this could be India's version of a BNPL product!

What do you think about credit cards on UPI? Will it have the intended impact? Let me know what you think. I'm on Email, Twitter or LinkedIn.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🌏 International

FTX CEO Sam Bankman-Fried has spent $30mm on political donations during the 2022 US primaries election cycle to prop up candidates who favor crypto deregulation. Global crypto funds dropped 29% to $34bn. Insufficient funds caused 27% of consumer payment declines in April, 2022 in US. PayPal launched a feature allowing users to transfer cryptocurrencies between wallets. Apple set up a new subsidiary Apple Financing LLC to oversee credit checks and make loan decisions internally.

Looking for the news digest? Read all the week’s fintech news and updates in India and SEA over at This Week in Fintech - India and SEA Edition.

🏷️ Other Notable Nuggets

Predictably Unpredictable: Navigating the Volatility of Transactional Revenue

Private Equity Are Being Rewarded —or Penalized — for Taking Illiquidity Risk

The Mother of All Demos, presented by Douglas Engelbart (1968)

Quarter in Review: Top 3 key Fintech developments in Q2 2022

🎵 Song on loop

Fintech updates can get boring, so here's an earworm: This Girl (Kungs vs. Cookin’ on 3 Burners). Incredible beats to get me going. On Spotify and Youtube.

👋🏾 That's all Folks

If you’ve made it this far - thanks! As always, you can always reach me at connect@osborne.vc. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.