Free Sample Economics | Fintech Inside #112

Why the best fintech companies win trust the same way Indian supermarkets win customers i.e. free samples first, big purchases later. A framework for sequencing value in financial services.

Hi Insiders, I’m Osborne, an investor in early stage startups.

Welcome to the 112th edition of Fintech Inside. Fintech Inside provides nuance and insight to the big trends shaping financial services. It’s the fintech newsletter for people who don’t have time to read five fintech newsletters.

I love spending time at a clean, well-organised supermarket. Just adult things, I guess. There’s something fun about walking down the aisles, seeing the products, discovering new ones, physically adding them to cart and checking out (sounding like my parents). While doing so, for some reason, my mind wonders why a certain product is placed there, why not somewhere else, what’s at the checkout, and so on.

Recently I checked out the free sample counter at Nature’s Basket. Not because I needed that sweet jam they were offering, but because I couldn’t stop thinking about why it’s there. The person handing it out didn’t care if I was a “qualified buyer” before they gave it to me. It’s free, it’s small, and it exists to do exactly one thing: get me to taste before I trusted the brand.

The more I looked, the more I realised the most successful consumer companies run on the exact same instinct. This edition is my attempt to model that instinct for financial services — tracing it across Jar, Kreditbee, Chime, Alipay and others — and answering the question that actually matters if you’re building one of these products: how do you know when you’ve earned the right to stop giving and start asking?

Funny enough, I bought the jam, when I’m supposed to be off sugar.

Thank you for supporting me and sticking around. Enjoy another satisfying week in fintech.

— Written with Wispr Flow #ad

Considering angel investing? I get a bunch of fintech founders reaching out to me for investors. I’d be happy to put you in touch. Send me a DM here.

Wispr is offering Fintech Inside readers 3 months free access to the Pro Plan. Try it here now or use the code WISPRINSIDE. #ad

🤔 One Big Thought

Free Sample Economics

Why the most successful financial products give before they take and how to know when it’s time to ask

The Supermarket Instinct

Walk into a Nature’s Basket, DMart, Reliance Fresh or any other supermarket on a weekend and you’ll find someone standing at the end of an aisle, handing out a cube of cheese on a toothpick or jam on a bread or chip with a dip. Nobody asked for it. Nobody had to prove they deserved it. It’s free, it’s small, and it’s designed to do exactly one thing: let you taste the product before you’re asked to trust the brand with your money.

Financial services runs on the same instinct, even though almost nobody in the industry describes it that way. I call it Free Sample Economics, because once you see it, you start noticing which firms are playing this game well and which ones are skipping the sample and going straight for the sale.

I’ve been circling this idea since I wrote about Time to Value (Edition #103) i.e. the principle that the speed of a user’s first “aha” moment decides whether they stick around long enough to become a customer. That piece was about speed. This one is about direction. Specifically: which way is the money moving when a user has their first meaningful interaction with your product?

Two questions every product asks

Strip away the branding, and every financial product/service is really asking the user one of two questions.

Question 1: “How quickly can I make your financial life better?”

Save you money. Make you money. Lend you money. Simplify a payment. Show you a gain. These are outflow moments i.e. the company puts something into the relationship first, before asking for anything back.

Question 2: “Will you trust me with your money?”

Invest with us. Insure with us. Save with us. Park your assets here. These are inflow moments i.e. the company is asking the user to hand over something real: capital, a long-term commitment, insurance and so on.

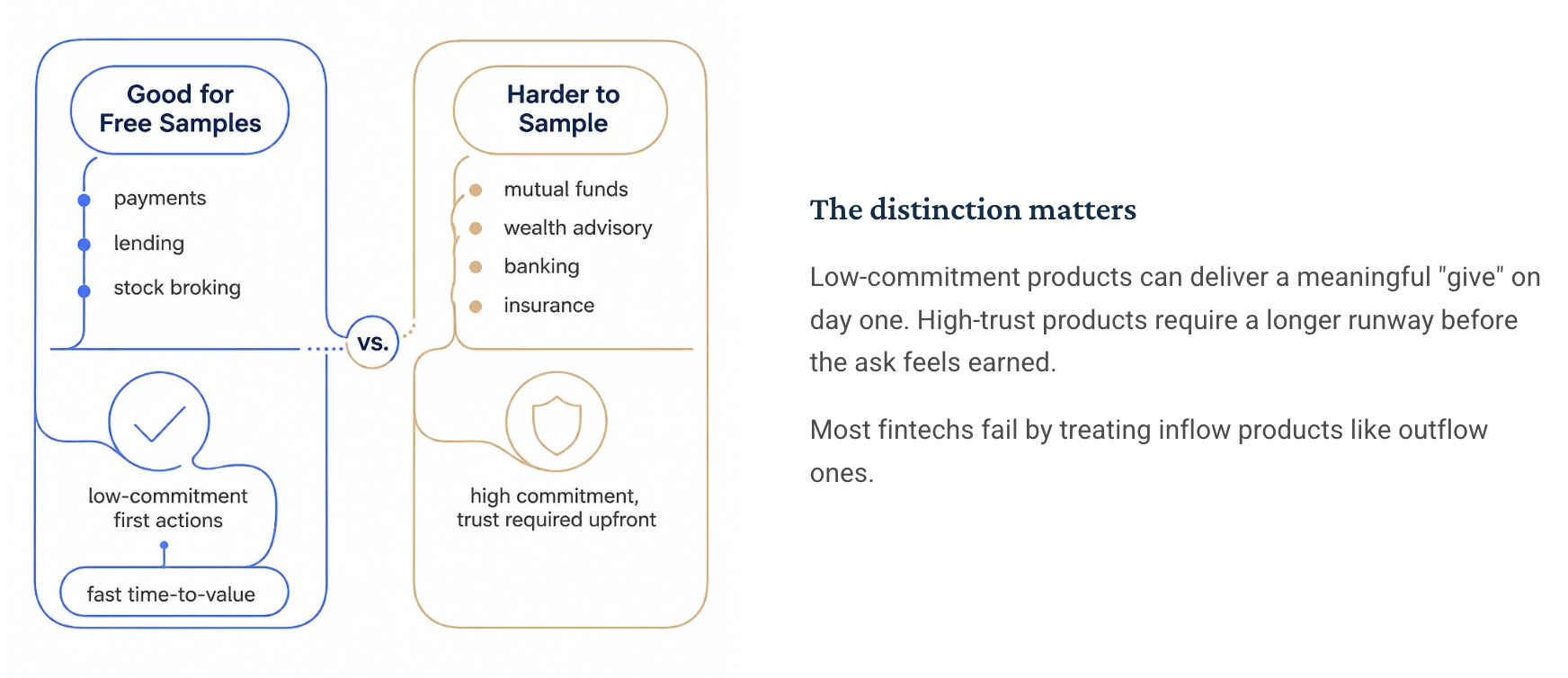

The mistake I keep seeing, across pitch decks and cap tables alike, is founders trying to ask Question 2 of the user before they’ve earned the right to. You cannot sell a mutual fund SIP to someone who hasn’t yet decided your app deserves a permanent place on their home screen. Trust is not a marketing output. It’s a compounding balance, and free samples are how you make the first deposit.

Financial products/services that lend themselves well to the free sample model include payments, lending, stock broking and so on. Products/services that don’t lend themselves well to the free sample model include mutual funds, wealth advisory, banking, insurance and so on.

Free Sample Economics, in practice

I’ve noticed I look for this pattern/framework when evaluating companies. The interesting thing about this framework is how visible it is once you start looking for it, across Indian and global fintech alike.

Jar used to let users invest in digital gold within 60 seconds and with small amounts. First saving action, executed within 60 seconds, compared to mutual funds, stocks and other investment/savings products. Rounding up spare change into gold is a free sample of investing behaviour itself. The user isn’t handing over a lump sum on day one. StableMoney gave users investments in fixed deposits on similar lines. Users are tasting what it feels like to accumulate, in amounts small enough that trust is never really on the table. By the time Jar or StableMoney can credibly pitch a bigger savings or investment product, the user has already run the experiment on themselves, for weeks or months.

Kreditbee and consumer lending more broadly run on the same instinct, inverted. The “give” isn’t a discount, it’s speed and access. A small-ticket loan disbursed in minutes, to a user where a bank would take a week to underwrite, is the “sample”. The company absorbs the underwriting risk first. Only after a few cycles of on-time repayment does the relationship justify a bigger ticket size, a longer tenure, or a cross-sold product. A few years ago I would hear of unsecured lending startups initially offering a credit limit of ₹2,000. Last year I heard, some are offering ₹200 credit limit!

This is the main reason digital, challenger banks globally have been able to earn trust of their users when their first product was a consumer loan. I haven’t come across a large challenger bank globally that started with anything but a loan product.

Payment companies like Paytm, PhonePe, CRED and others have also amassed large user bases by offering “free samples” by way of discounts. Sure, the payment successfully going through instantly via UPI is a great experience, but if the underlying technology (UPI) is commodity, why will the user come back to the app? The instant cashback or discounts invites the user to come back, use the app and make paying with the app a habit. We forget that cashbacks and discounts were typically “post paid” and the users would never see the value in them. That’s changed now.

Chime, in the US, made its name on a feature that cost the company money on every single use: fee-free overdraft up to a small cap, and paychecks that land up to two days early. Neither is a revenue line. Both are free samples of what banking without punitive fees feels like — and they’re the reason Chime converted a fee-fatigued, underbanked demographic that traditional banks had spent decades failing to earn trust with.

Alipay, at a different order of magnitude, ran the same mechanic at the scale of a payments network. Instant, frictionless QR payments with no cost to the merchant or consumer were the sample that got hundreds of millions of users transacting daily. Only once that habit was locked in did Ant Group introduce Yu’e Bao, letting idle payment balances earn a return, turning a payments app into the largest money market fund on earth. The free sample wasn’t a discount at all. It was convenience, handed out at a scale no bank could match.

Notice what’s common across all five: the “give” isn’t charity, and it isn’t even always a discount. Sometimes it’s speed. Sometimes it’s a fee waived. Sometimes it’s the simple experience of a task that used to take a week now taking a day. The form changes. The direction doesn’t.

When free samples don’t convert

I have to be honest about the limits of this framework too, because I’ve watched it fail as often as I’ve watched it work.

The Indian food-delivery discount wars are the cleanest cautionary tale. Billions of dollars of “free sample” were handed out in the form of subsidised delivery and inflated cashback, and for years it looked identical to trust-building. It wasn’t. It was just a subsidy. The moment the discounts stopped, so did the loyalty, because nothing about the underlying product had actually earned trust, the price had simply been temporarily hidden from the user.

The same trap catches neobanks that spend aggressively on welcome bonuses and cashback, and then wonder why deposits never show up. If the “give” doesn’t sit inside a product experience the user actually values on its own merits, it’s not a free sample. It’s a discount. And discounts train users to expect the next discount, not to trust you with their savings.

The distinguishing question is simple: if you took the incentive away tomorrow, would the user still come back? If the answer is no, you were running a customer acquisition subsidy with better branding.

The exit condition

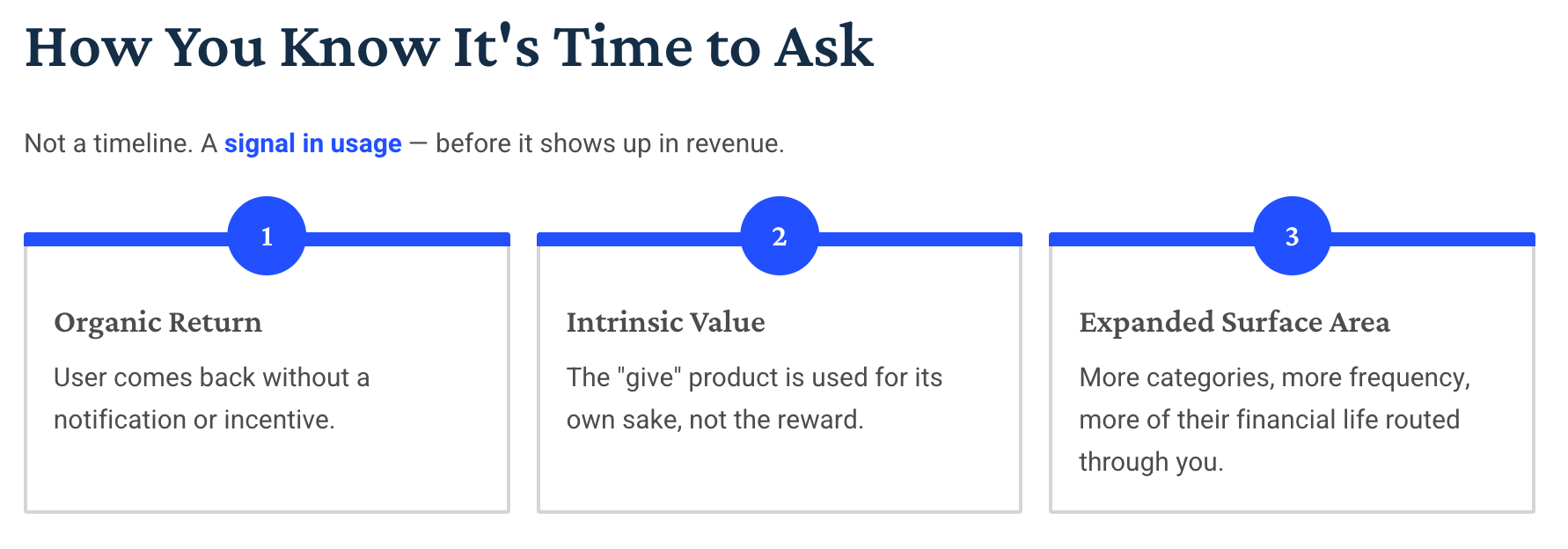

This is the question the earlier draft of this framework skipped, and it’s the one that actually matters if you’re a founder reading this: how do you know when you’ve earned the right to ask the user to trust you with their money?

I don’t think it’s a timeline. It’s a signal, and it shows up in usage before it shows up in revenue. It looks like:

The user is coming back without being prompted by a notification or an incentive.

The “give” product is being used for its own sake, not for the reward attached to it.

The user has, on their own, expanded the surface area of their relationship with you, more categories, more frequency, more of their financial life routed through your app.

That’s the moment the flywheel is allowed to turn from give to get. Ask before that signal shows up, and you’re not converting trust, you’re spending down a balance you never actually built.

Full circle

Financial services is one of the only industries where the sequencing of value delivery is the entire strategy. You can’t out-market distrust, and you can’t discount your way into a savings deposit. The founders building durable financial services companies aren’t the ones with the best inflow products. They’re the ones who understood, earlier than their competitors, that you have to hand out the free sample before anyone lets you near the checkout counter.

The best fintech companies don’t begin by asking customers for assets. They begin by becoming an asset to the customer.

That’s Free Sample Economics. Give first. Earn the signal. Then ask.

— Written with Wispr Flow #ad

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🎵 Song on Loop

Good background songs to listen as you read Fintech Inside: This week I discovered We are the People by Empire of the Sun (Spotify / Youtube). It's got that shimmery, anthemic synth-pop build that makes even reading about mutual fund SIPs feel a little cinematic.

✨ Call Outs

[VIDEO] TOTO's Semiconductor Secret

[INTERVIEW] What the West Gets Wrong About China | Alice Han & Trevor Noah

[ARTICLE] What you can’t say in Silicon Valley

[ARTICLE] 46 thoughts on the near future

👋🏾 That’s All Folks

If you’ve made it this far - thanks! As always, you can always reach me via DM at osborne.vc/dm. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.

Insightful read! I appreciate the depth and clarity of your analysis. We’re also active in the fintech ecosystem and would love to explore collaboration opportunities around content, research, or founder conversations. Looking forward to more posts!