No Country for Risk | Fintech Inside #106

Near-zero defaults. Record provisions. Reducing unsecured lending. India's financial system is the safest it's been in decades, and a war nobody predicted might prove why.

Hi Insiders, I’m Osborne, an investor in early stage startups.

Welcome to the 106th edition of Fintech Inside. Fintech Inside is the front page of Fintech in emerging markets.

Every quarter, I spend a couple of weeks reviewing investor presentations and analyst call transcripts of public financial companies to understand how user behaviour is changing, where the industry is headed and what these large institutions are doing to navigate the future. I published a report covering the period Q1 FY26. Would you want to see the report for Q3 FY26? Let me know, will publish it.

When reviewing the data for Q3 FY26, I started noticing a trend - default rates at record lows, provision buffers growing, lending mix increasingly conservative, unsecured credit in free fall and more. Almost as if… Indian financial institutions forgot how to take risk.

But then the West Asia conflict happened. And suddenly it seems like this risk aversion might be what shields the Indian economy from economic shocks.

The irony is uncomfortable. In normal times, I'd criticise these numbers, institutions sitting on record capital buffers, retreating to gold loans, starving MSMEs of credit. But with oil at $100 and supply chains fracturing across the Strait of Hormuz, the most overcautious financial system in decades might also be the most resilient one. That tension is what this edition is about.

This edition is best read with your favourite cuppa. Let’s get into it!

Happy new financial year to those who celebrate!

Thank you for supporting me and sticking around. Enjoy another satisfying week in fintech!

Considering angel investing? I get a bunch of fintech founders reaching out to me for investors. I’d be happy to put you in touch. Send me a DM here.

🤔 One Big Thought

India’s financial institutions forgot how to take risk

It might be what shields India in the short term

Like most of you, I’ve been glued to the news from West Asia. The Iran conflict isn’t abstract for me, I have friends, family and founders across countries in the region, and the first few days were spent checking in on people.

But once the immediate personal concerns settled, the fintech investor in me kicked in. I was following the politics from a distance, but the economic impact? That’s my lane for curiosity. And the question that kept nagging me was simple: How can this war impact us in the Indian fintech ecosystem?

So I did what any venture capitalist would do - I put on my 2-weeks-only armchair economist hat and went deep. I pulled Q3 FY26 investor presentations from every major Indian bank and NBFC. I cross-referenced them with RBI’s long-term asset classification data going back to 1997. I read through CareEdge’s latest credit and deposit research.

I watched Neelkanth Mishra’s sobering analysis on the Strait of Hormuz (he’s the Chief Economist at Axis Bank and one of the sharpest macro thinkers in the country). I’ve listened to every Odd Lots podcast’s Iran coverage, interviewing experts going deep on topics across fertilisers, ammunitions, oil, logistics, insurance and more.

What I found was interesting. The Indian financial system is the strongest its been in decades, by every metric. But the more I dug into the data and the narratives, a different story emerged. A story about a financial system that has become so obsessed with safety that it may have forgotten what it’s supposed to do i.e. take risk.

And the irony of it all? That very same excessive caution, the caution I’d normally criticise, might be the thing that protects us from what’s happening in West Asia.

The case that banks are playing it too safe

Bad loans have practically vanished. Banks make money by lending - ~85% of banking income is interest income. I’ve done a whole deep dive in Edition 65 covering the revenue split of banks in India.

Sometimes borrowers don’t pay back. When a borrower stops paying for 90+ days, that loan becomes a “Non-Performing Asset” or NPA, a bad loan sitting on the books. The percentage of loans that go bad is the Gross NPA ratio, think of it as the bad loan (default) rate.

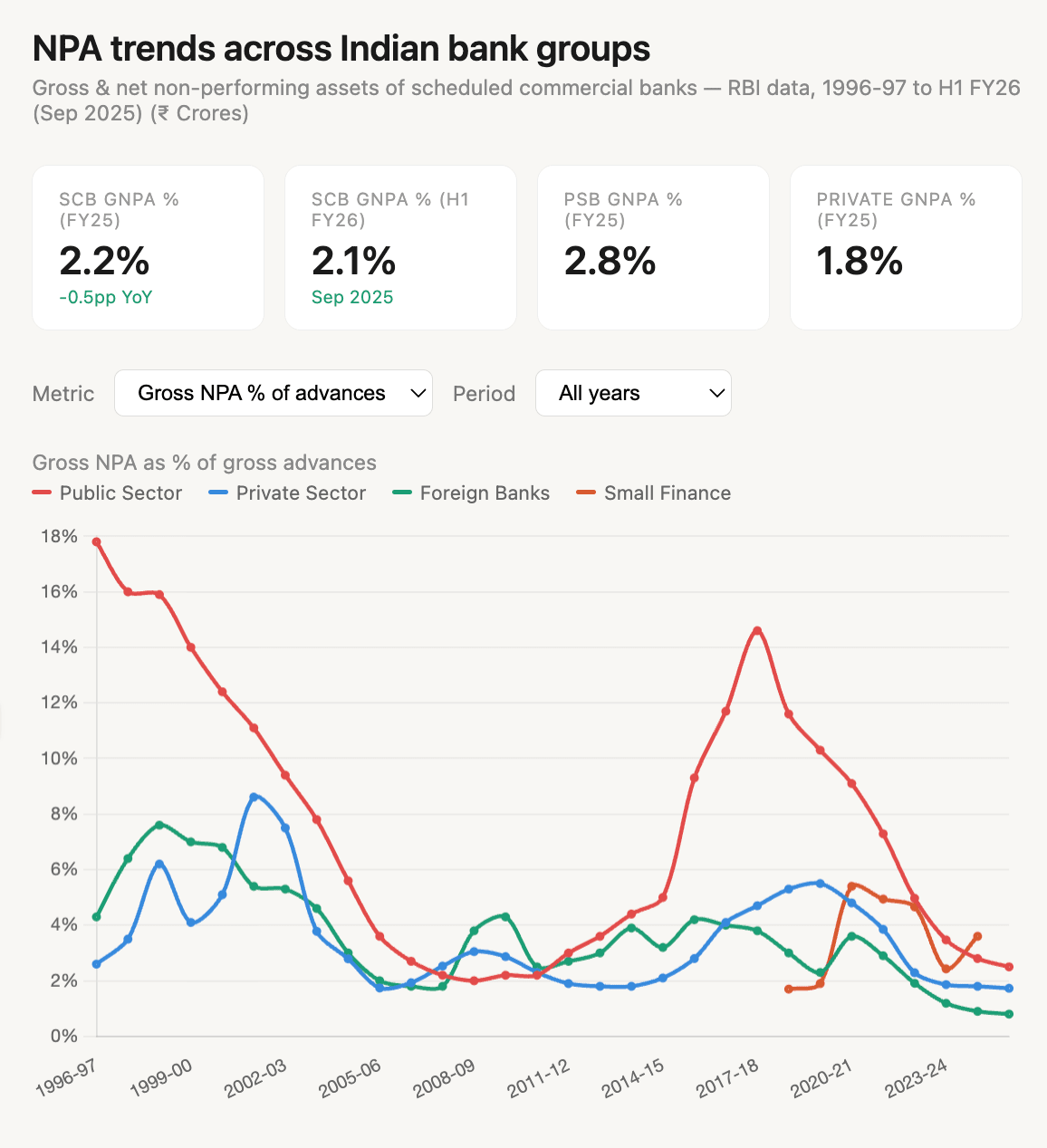

In 2018, India’s system-wide Gross NPA (GNPA) ratio peaked at 11.2%. For government-owned banks (Public Sector Banks), it was a catastrophic 14.6%. For context, anything above 4% is considered really bad. Above 7-8% is a crisis. India was deep in crisis territory.

Today? The system-wide GNPA has collapsed to 2.2%, the lowest since 2008. Public sector banks have gone from 14.6% to 2.6%. Private banks sit at 1.8%.

The NPA chart from RBI data tells this story visually, three decades of bank defaults, and the current numbers are at the absolute floor.

A 2.2% default rate sounds great. It means 97.8% of all loans are being paid back on time - maybe some delinquencies (delays), maybe debt collections platforms are showing better collections efficiency.

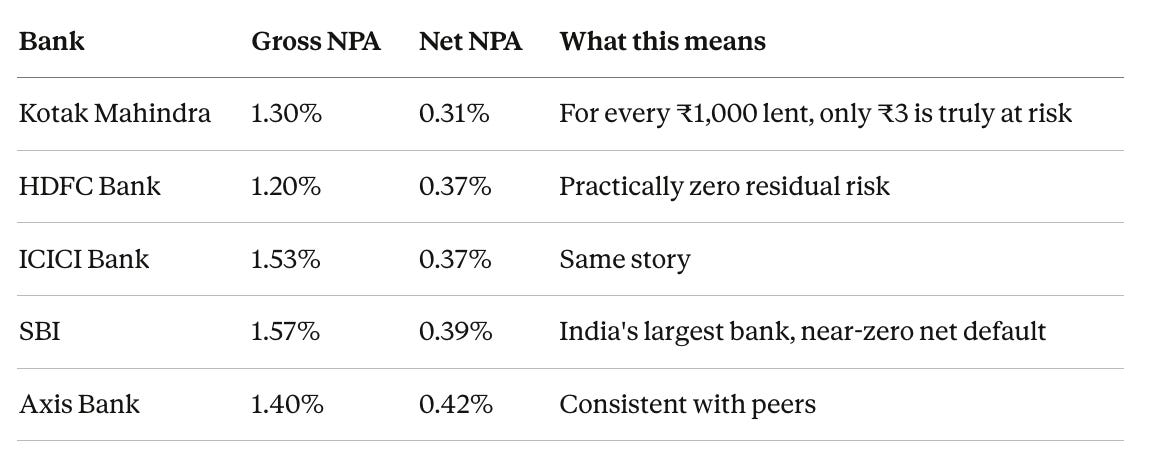

The Net NPA numbers are even more extreme. Net NPA strips out the provisions banks have already set aside for bad loans, it’s the actual residual risk on the books. Here’s what Dec, 2025 (Q3 FY26) looks like for India’s top banks:

Net NPAs of 0.3% to 0.4%. Even the NBFCs (Non-Banking Financial Companies, lenders that operate outside the traditional banking structure) are showing extreme discipline: Bajaj Finance at 0.44% net NPA, Sundaram Finance at 1.06%, HDB Financial at 1.25%.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

It seems like India’s financial system has become risk averse - too terrified of making a bad loan.

A quick caveat on the percentages. The last time system-wide GNPA was at 2.2% was in 2008 and 2010-11. But back then, the total loan book was roughly ₹20 lakh crore ($460bn at 43.3 USDINR) . Today it's nearly ₹198 lakh crore ($2tn at 94.0 USDINR), 10x larger in INR terms. So 2.2% today translates to roughly ₹4.4 lakh crore in absolute bad loans, compared to ₹68,000 crore in 2008-09.

The percentage is at a historic low, but the rupee value of bad loans is still substantial. What's different this time is the provision buffer sitting underneath, banks have set aside 75-92% of those bad loans in cash reserves. The absolute exposure is bigger, but the net risk after provisions is the lowest it's ever been.

Provision buffers built for a crisis that already ended

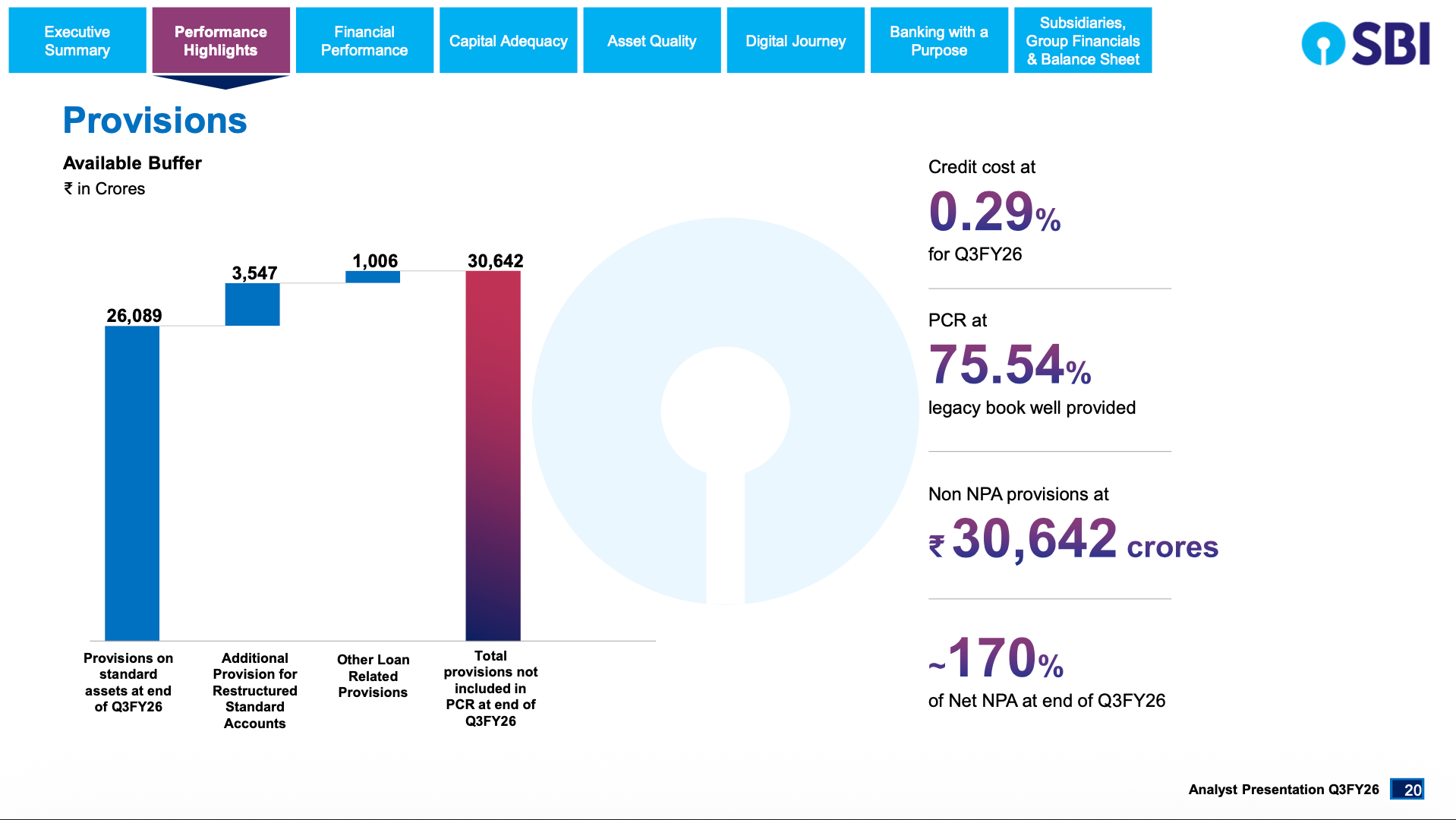

The Provision Coverage Ratio (PCR) measures how much cash a bank has set aside to cover bad loans. If a bank has ₹100 in bad loans and has set aside ₹75, that’s a 75% PCR. Think of it as an insurance reserve.

During the 2018 IL&FS crisis, PCR was 50-60%. Banks were caught underprepared. Fair enough, they learned a painful lesson. But the crisis ended eight years ago. Bad loans have fallen by 80%. And yet, provision coverage keeps climbing.

Major banks are running PCR of 75-83%. SBI’s coverage, including certain recovery accounts, is 92.4%. For every ₹100 of bad loans on SBI’s books, loans that already represent just 1.57% of the portfolio, ₹92 is covered.

Where the lending is actually going

The clearest evidence of safety-first thinking isn’t in the NPA data. It’s in what banks are choosing to lend for.

Following RBI’s tightening measures, unsecured personal loan growth has collapsed from 21.1% YoY in FY24 to 7.0% YoY in December 2025. These are loans without collateral, the kind that fund small business expansion, consumer purchases, aspirational spending. Banks have slammed the brakes.

Meanwhile, loans against gold surged 127% YoY. The fastest-growing loan category in Indian banking is one backed by physical gold sitting in a vault. Muthoot Finance, the largest gold loan NBFC, has delivered 40% stock returns this year riding this boom.

Personal loans now make up roughly 35% of all bank credit, up from 19% a decade ago. Industry lending has fallen from 45% to 23%. And even within the personal loan category, banks are retreating from anything unsecured.

Capital buffers that are almost absurdly thick

Banks need to maintain a minimum capital ratio, CRAR (Capital to Risk-Weighted Assets Ratio), essentially the cash cushion relative to the risks they take. India’s regulatory minimum is 9%.

Today, all 78 scheduled commercial banks are above 10%. Zero below 9%. Zero in the danger zone. Kotak sits at 23.3%, more than 2.5x the minimum. SBI Card at ~27%. Even SBI, with the country’s largest loan book, has a comfortable 14%.

When every single bank is over-capitalised and simultaneously posting the lowest default rates in history, the capital is sitting idle when it could/should be funding growth.

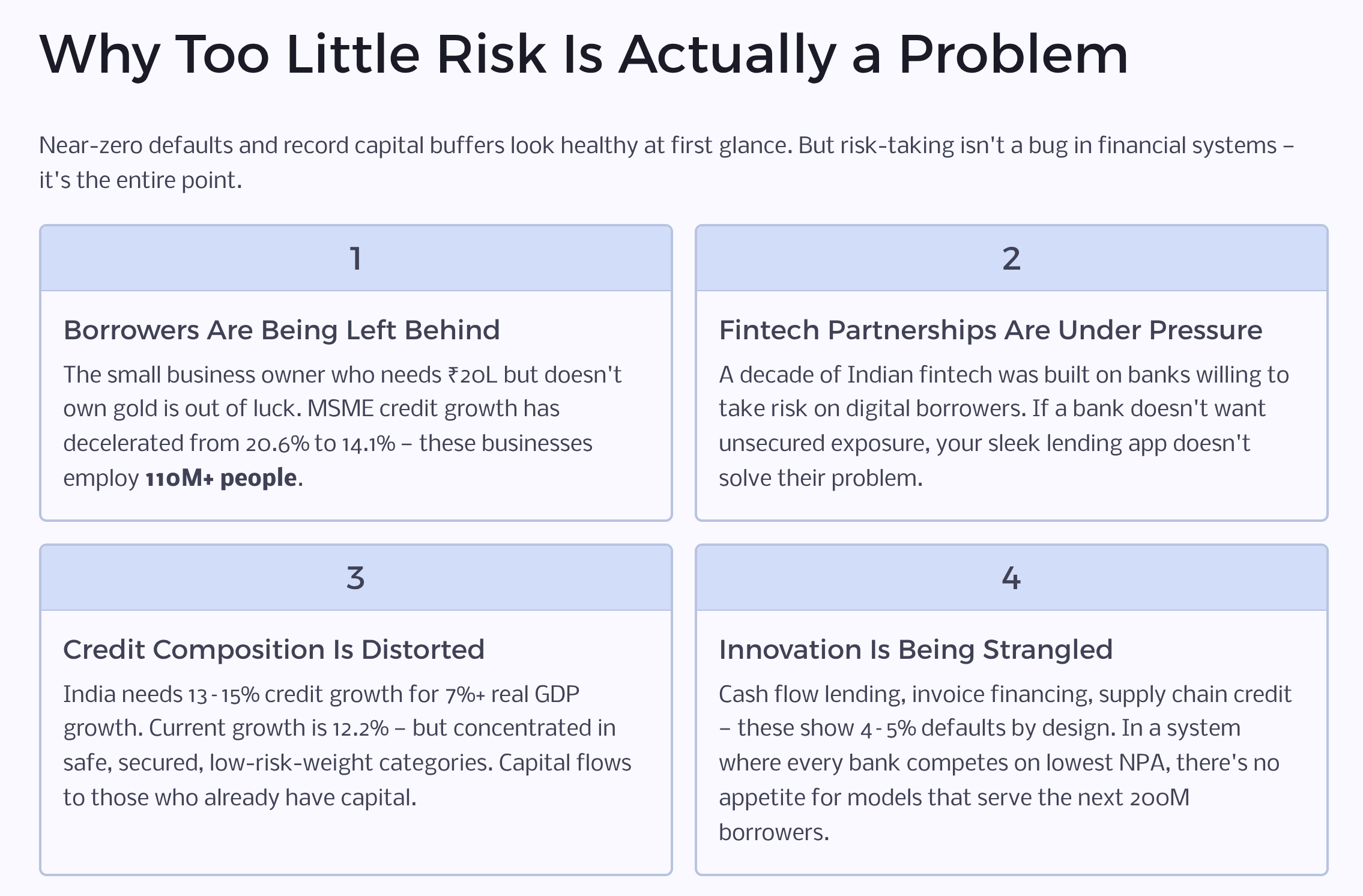

Why too little risk is actually not great

This is worth pausing on. There’s a temptation to look at near-zero defaults and record capital buffers and think “great, the system is safe.” But risk-taking is not a bug in financial systems. It’s the entire point.

Banks exist to intermediate risk, to take money from depositors and deploy it toward productive activity that grows the economy. When they stop doing that effectively, the consequences ripple outward.

For borrowers, the credit squeeze is real. The small business owner who needs ₹20 lakhs to buy equipment but doesn’t own gold or property is increasingly out of luck. The first-generation entrepreneur without a credit history can’t get a working capital line. The consumer who needs a personal loan to bridge a medical emergency faces fewer options. When unsecured lending growth drops from 21% to 7%, that’s millions of Indians who could have been borrowers, aren’t. MSME credit growth has decelerated from 20.6% to 14.1%. These are businesses that employ 110M+ people.

For fintechs, the partnership model is under pressure. The last decade of Indian fintech was built on a thesis: technology companies would originate, underwrite, or distribute credit on behalf of banks and NBFCs. Co-lending, digital lending partnerships, FLDG arrangements, all of these depend on banks and NBFCs being willing to take risk on the underlying borrower. If a bank doesn’t want unsecured exposure, your sleek digital lending app doesn’t solve their problem.

For the broader economy, credit growth drives GDP growth. India needs 13-15% credit growth to sustain 7%+ real GDP growth. Credit is currently growing at 12.2%, which is adequate. But the composition matters, the growth is increasingly coming from safe, secured, low-risk-weight categories. The sectors that need credit most are getting proportionally less. When banks only lend where they can’t possibly lose money, capital flows to those who already have capital. That’s not financial deepening.

For innovation, excessive caution kills experimentation. Cash flow-based lending, invoice financing, supply chain credit - these models have higher default rates than gold loans. That’s by design. They serve riskier segments at higher yields, and when done well, the portfolio economics work. But in a system where regulators are raising risk weights on unsecured lending and banks are competing on who can have the lowest NPA, there’s no institutional appetite to underwrite models that might show 4-5% defaults even if they’re highly profitable.

The result: the very lending innovations India needs to reach the next 200M borrowers are being strangled in their infancy.

How did we get here? trauma and regulation

The overcorrection is a product of two forces.

The NPA PTSD: The 2015-2018 NPA crisis was brutal. Banks, especially public sector ones, were loaded with bad loans from reckless infrastructure lending. The cleanup through RBI’s asset quality reviews, and forced recapitalisation, was long and painful.

The RBI’s regulatory tightening: The bigger driver is regulatory. The RBI systematically tightened the screws over the past two years. Increased risk weights on unsecured lending (Nov 2023), tighter norms for NBFC lending, particularly around co-lending and digital partnerships, stricter asset classification rules, Enhanced KYC and compliance requirements that increase the cost of onboarding new borrowers, particularly in underserved segments.

The RBI isn’t wrong to be cautious. They’re the ones who had to orchestrate the 2018 cleanup. But regulation has a cost. When you make unsecured lending expensive, you make it harder for the borrower who doesn’t own gold or property to get a loan. When you tighten NBFC norms, you constrain the institutions designed to fill gaps traditional banks can’t.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

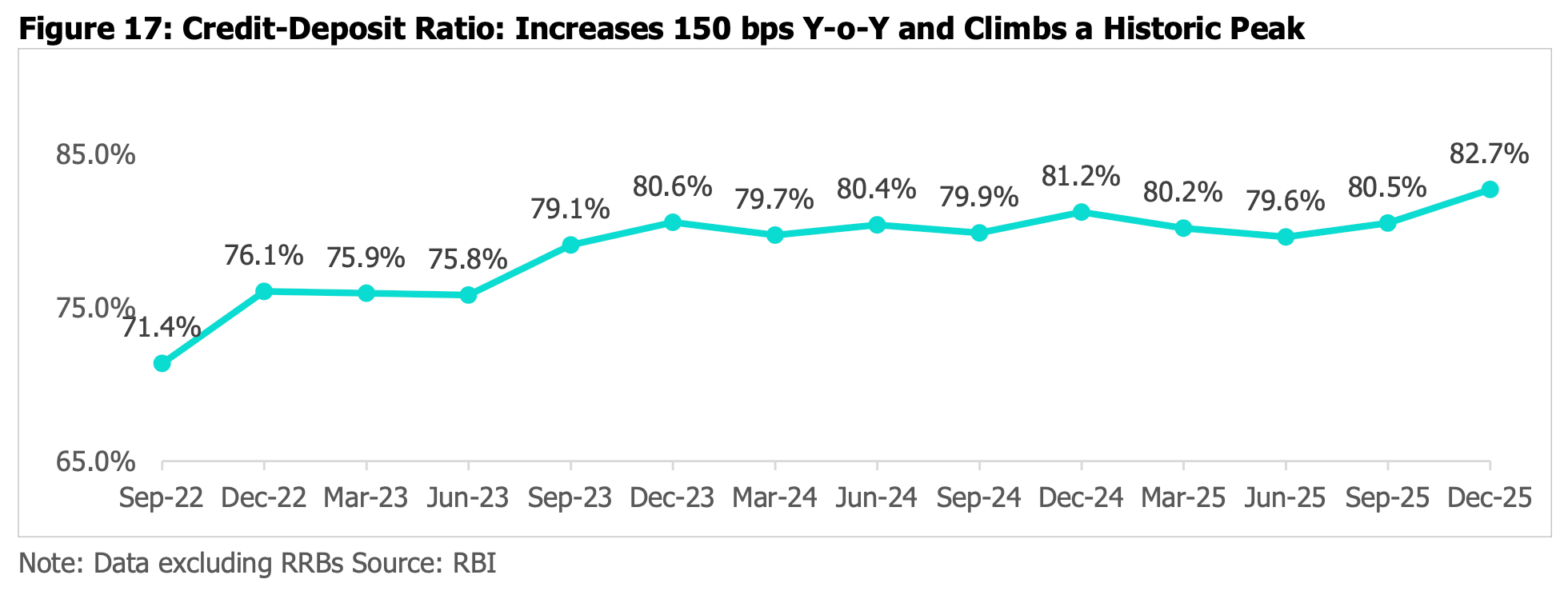

The deposit war is forcing conservatism

There’s a structural squeeze too. India’s Credit-to-Deposit ratio has hit a historic peak of 82.7%. Banks are lending faster than they’re collecting deposits. Credit is growing at 12.2%. Deposits at just 10.2%.

The CASA ratio, the share of lower cost current and savings account deposits, has dropped to ~38%. Retail investors have found better options: mutual funds, equities, higher-yielding fixed deposits. Banks are fighting a brutal war for deposits, which keeps funding costs sticky even as the RBI cuts rates.

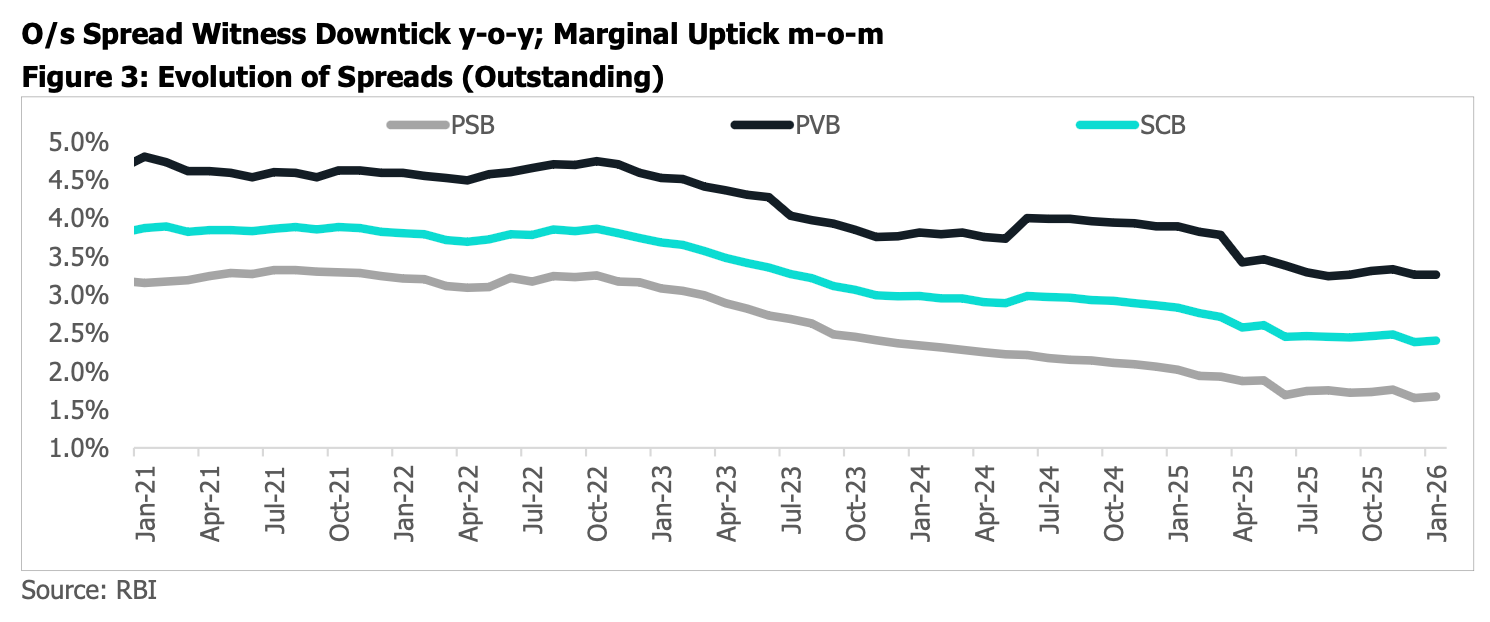

The spread (net interest margin) between what banks earn on loans (9.04%) and what they pay on deposits (6.64%) has narrowed by 43 basis points to just 2.40%. When margins compress, you get more selective about the loans you make. You don’t take chances on borderline credits when every basis point of spread counts.

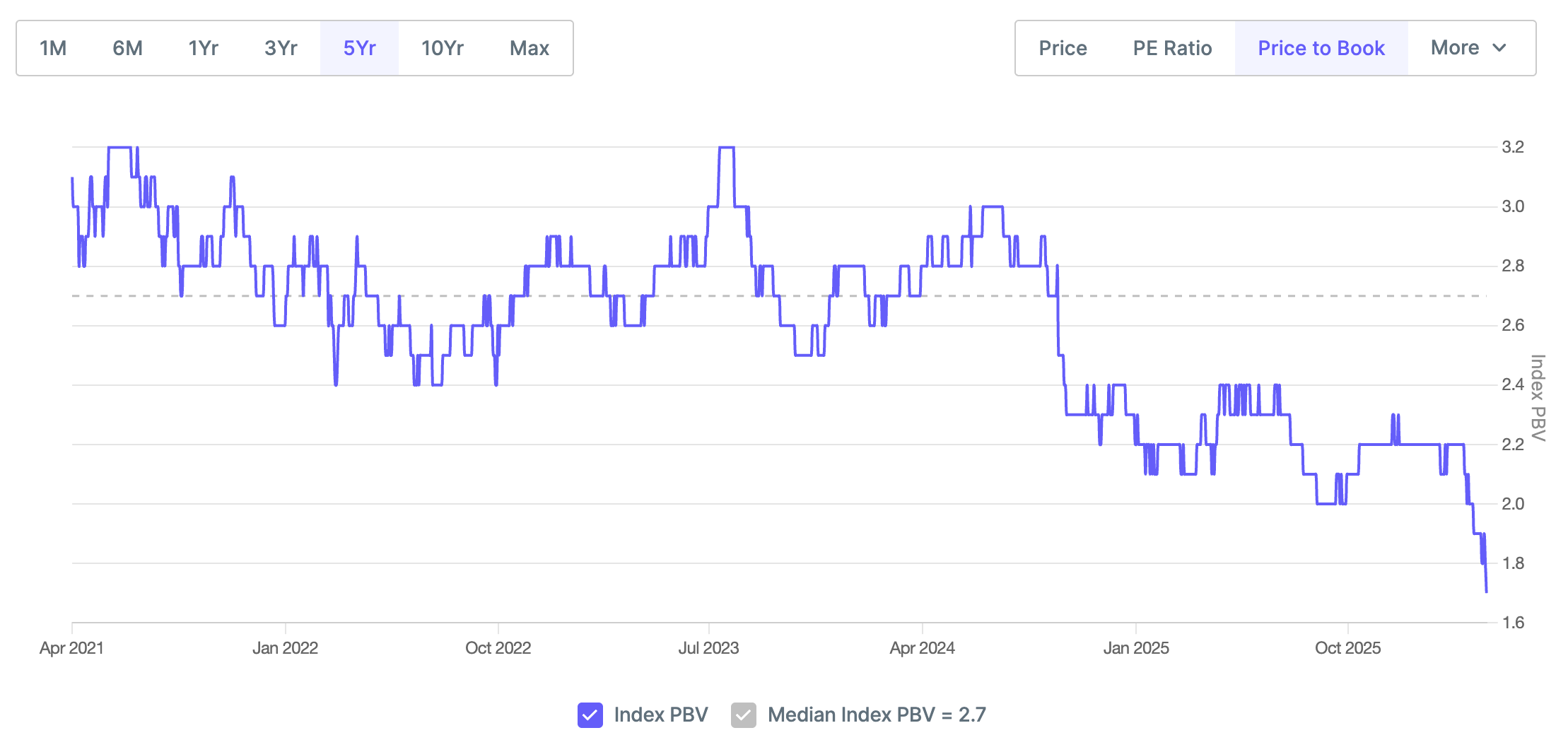

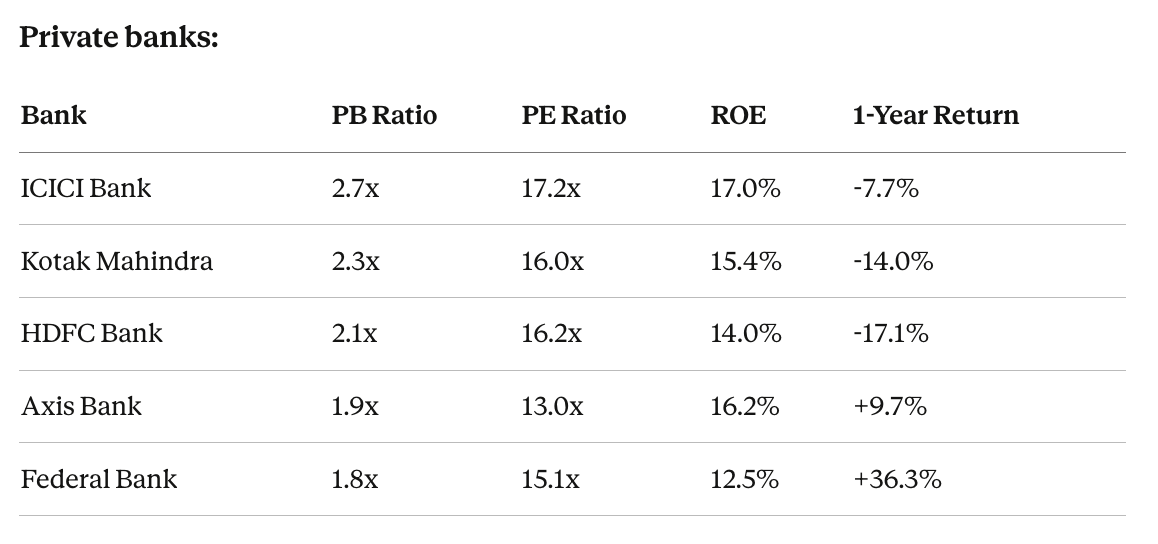

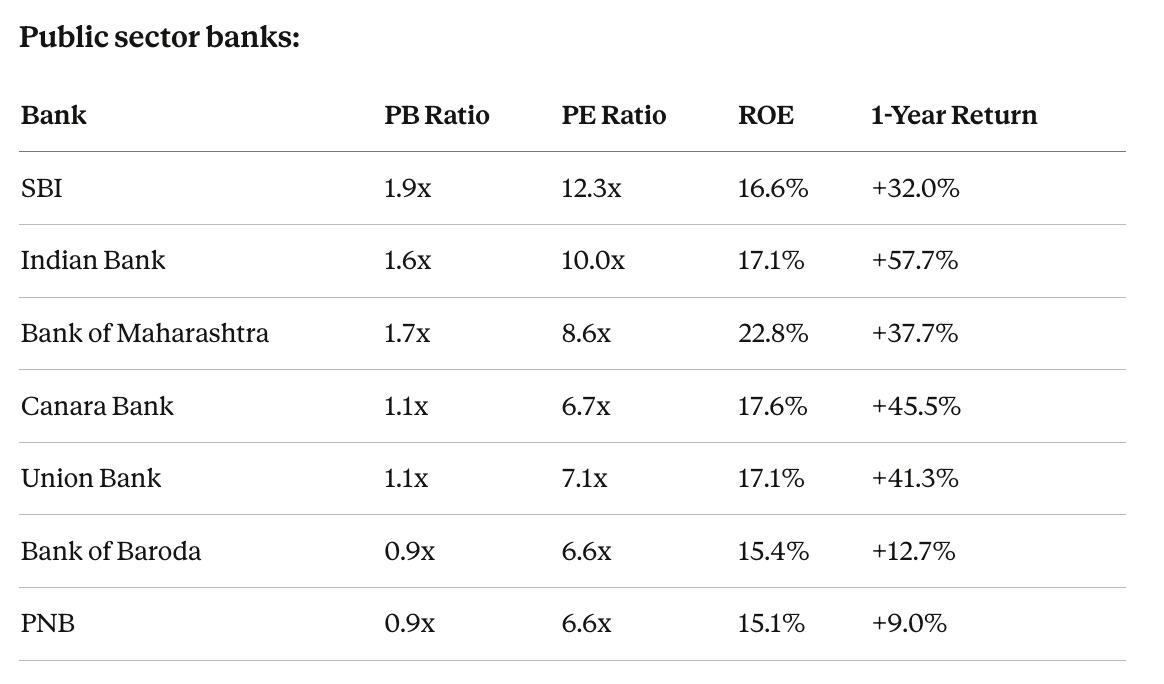

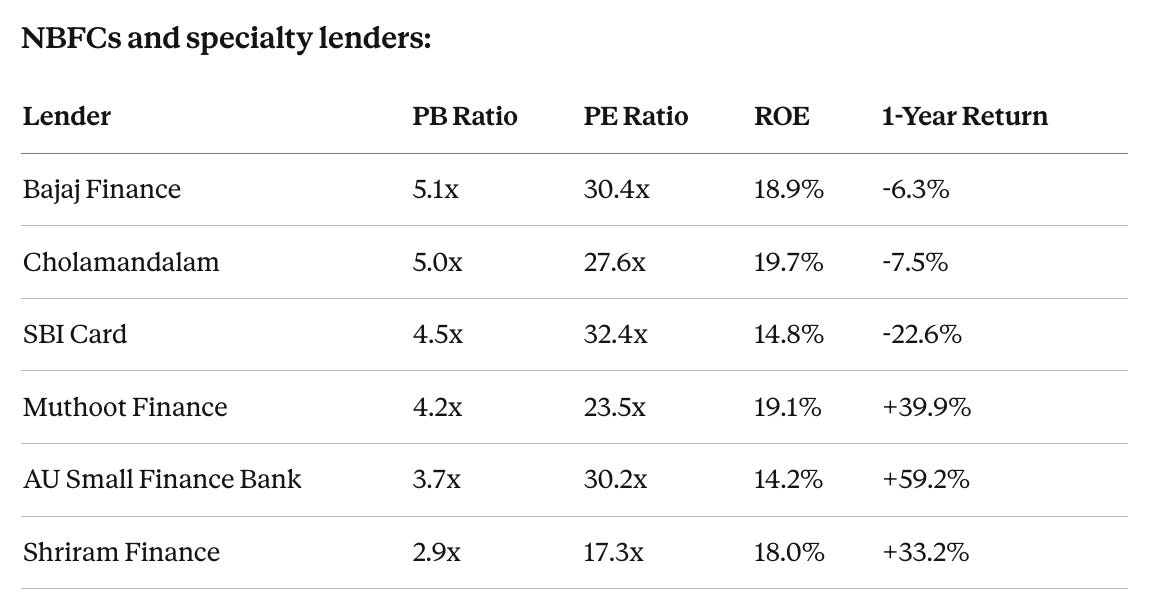

What the market is paying for all this safety

The Price-to-Book (PB) ratio tells you how much investors are paying for each rupee of a bank’s net assets. A PB of 1.0x means the market values the bank at exactly its book value (assets minus liabilities). Above 1x means investors believe the bank will generate returns above its cost of capital. Below 1x usually signals distrust.

The Bank Nifty currently trades at about 2.2x PB. Over five years, this has ranged from 1.6x (COVID panic, March 2020) to 3.2x (2023 bull run). We’re in the middle of the range i.e. not cheap, not euphoric, but trending downwards.

HDFC Bank at 2.1x is notable. This bank historically commanded 3-4x book because of its perceived governance premium. Between merger integration, NIM compression, and a recent governance episode, the market has taken roughly 50% off the valuation premium.

PNB and Bank of Baroda at 0.9x book. Sub-book-value with 15%+ ROE and net NPAs under 0.5%. Five years ago these banks were genuinely distressed, sub-book made sense. Today, the balance sheets are clean and the market still doesn’t fully trust them. Either the deepest value in Indian equities, or the market correctly pricing in the risk that PSU bank management will eventually find a way to squander the turnaround.

The market is paying 5x book for Bajaj Finance and 0.9x for PNB. Both have ROEs between 15-19%. The gap isn’t about asset quality anymore, it’s about trust in management, growth trajectory, and the ability to deploy capital productively.

The standout story: Muthoot Finance at 4.2x PB and 40% returns, built entirely on the gold loan boom. The lender who holds your gold in a vault and gives you 70% of its value is outperforming everyone. What does that tell you about this system’s appetite for risk?

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

Enter the storm

So here’s where I landed after two weeks of spreadsheets: Indian banks are playing it too safe. Default rates too low. Provision buffers too fat. Lending mix too conservative. Unsecured credit in free fall. Gold loans booming because nobody wants to take a chance. MSMEs being rationed out. Fintechs losing their bank partnership foundation.

And then the West Asia conflict changed the calculus.

The Iran conflict put the Strait of Hormuz in play. And suddenly, all that excessive caution started looking less like a problem and more like preparation.

The math of the Strait (according to Mr. Neelkanth Mishra)

The Strait of Hormuz, the narrow waterway between Iran and Oman, carries about 20% of the world’s crude oil. That’s roughly 21M barrels per day, or about 40% of all globally traded oil. Additionally, 2.5% of global gas and 50% of the world’s sulfuric acid (a base ingredient for virtually all chemical manufacturing) flows through it.

A sustained blockade cuts off 7% of global energy supply. Unlike a pandemic, where demand drops to offset the shock, an energy supply cut has no natural substitute. A 7% energy shortfall translates roughly to a 7% contraction in world GDP.

What $100 oil does to India

If oil stays at $100/barrel for a sustained period, India could face three simultaneous shocks:

The spending power shock: India’s trade deficit expands. That’s approximately 2.1% of GDP being pulled out of domestic purchasing power. Money that would have funded consumer spending and business investment goes to paying for more expensive imports.

The currency shock: To bridge the resulting balance of payments gap, the rupee would need to depreciate. A weaker rupee makes imports more expensive, creating a feedback loop.

The inflation shock: Even with partial pass-through of fuel prices, consumer inflation takes a direct hit. That’s before the cascading effect on food (fertiliser disruptions, China has already halted exports), construction, auto parts, and chemicals.

The second-order effects are worse than the headline. Global supply chains carry only 2-3 weeks of inventory. India holds roughly 25-30M barrels of oil reserves. China, which anticipated disruption, holds 100 days’ worth. Mishra’s assessment: the global economy cannot sustain a disruption lasting longer than 4 weeks.

The path from oil to banking stress

Lesser oil → higher transport and input costs → higher consumer prices → RBI pauses rate cuts or tightens → borrowing costs stay elevated → consumers and small businesses under pressure → loan defaults rise → banks tighten lending further → credit growth slows → economic growth slows → more defaults.

That’s the inflation-consumption-default spiral. And it specifically hits the segments already showing early cracks i.e. MSMEs, small businesses, unsecured borrowers. Exactly the borrowers banks had already pulled back from.

The irony: too safe becomes just safe enough

Everything I flagged earlier i.e. the excessive caution, the hoarded provisions, the retreat to gold loans, the stifled risk-taking - suddenly looks like exactly the right positioning for a world where oil is at $100+ and supply chains are breaking.

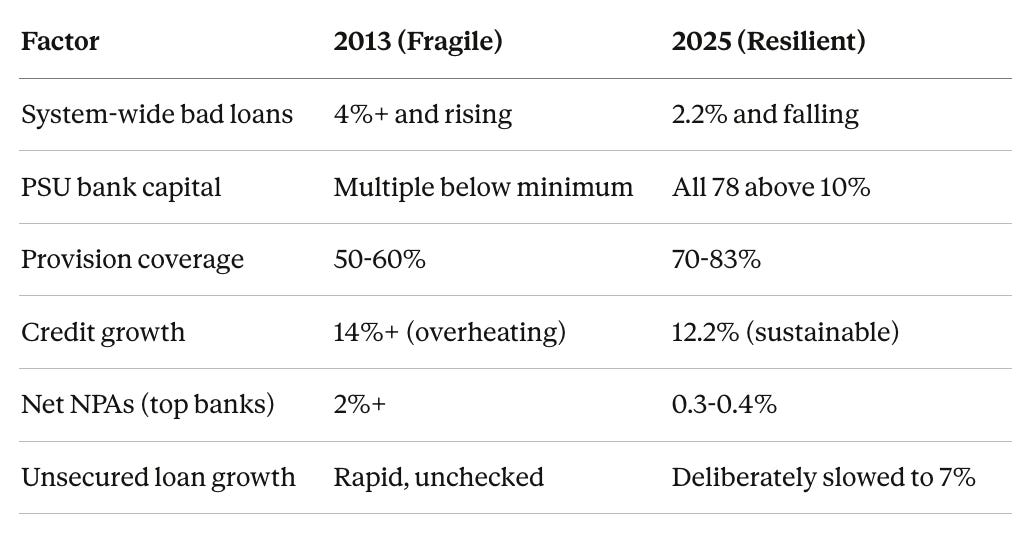

The last time India faced a comparable external shock was the 2013 “taper tantrum” combined with oil volatility. The banking system was structurally fragile:

Even in a severe scenario where bad loans double from 2.2% to 4.4%, that’s still below 2018 peak levels. Credit costs could rise 100-200 basis points and the system would remain solvent, well-capitalised, and capable of lending.

Those “excessive” provisions? They’re the buffer that absorbs the first wave of defaults without triggering a capital crisis. That “too-conservative” lending mix? It means the loan book is skewed toward secured assets - gold, property, vehicles, that hold value in a downturn. The collapsed unsecured growth? It means less exposure to the borrower segment that defaults first when inflation spikes.

The system I was ready to criticise for not taking enough risk turns out to be well-positioned for an external shock nobody saw coming.

Is that luck? Is it the RBI playing a longer game than any of us realised? Or is it the happy accident of institutional trauma - the hangover from 2018 producing caution that accidentally prepared the system for 2026?

Probably a bit of all three.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

One question I’m wrestling with, and I don’t have a clean answer.

In normal times, the Indian banking system is probably too cautious. But these are not normal times. And the question of “how much risk should banks take?” looks very different when there’s a conflict in West Asia and supply chain disruptions are shutting down factories.

The tension between these two truths is the defining question for Indian banking right now. Too little risk starves the economy of growth capital. Too much risk leaves it vulnerable to shocks. The system is currently planted firmly on the cautious end. The conflict validates that positioning in the short term.

But when the conflict ends we’ll need to have a serious conversation about whether this level of caution is sustainable for a country that needs 7-8% GDP growth.

How should founders plan for this period?

Credit is flowing but narrowing. Credit growth is projected at 13-14.5% for FY27. That sounds healthy. But secured lending is booming while unsecured is being rationed. If you have hard assets to pledge, you’re in a borrower’s market. If you don’t, options are shrinking.

Build working capital buffers. If you’re in anything MSME-adjacent, logistics, transport, manufacturing, anything tied to input costs, assume your working capital cycle lengthens by 30-60 days. The founders who survive geopolitical shocks are the ones with the most cash, not the best product.

Partner risk is real. If your fintech relies on third-party program managers, payment aggregators, or API partners, their compliance failures become your problem. Audit your partners. The regulatory appetite for enforcement is clearly rising.

Watch your customers’ customers. If you serve small businesses, their end consumers cut spending first when inflation bites. Model your revenue with a 10-15% consumption sensitivity.

What this means for fintech startups in India

The system’s caution is your white space. Banks have retreated from unsecured lending. Growth collapsed from 21% to 7%. But demand for credit hasn’t disappeared, it’s just unserved. Fintechs that can underwrite the “unbankable” borrower more intelligently, using cash flow data, GST analytics, supply chain signals, are filling a gap that’s wider than it’s been in years. Build the underwriting intelligence and banks will partner with you.

Novel collateral types are the unlock. If the system wants collateral, give it collateral, just not the traditional kind. Warehouse receipt financing, invoice discounting, equipment-backed lending, receivables factoring. Every fintech that can create a trusted collateral layer for borrowers who don’t own gold or property is building a wedge into the biggest gap in Indian financial services.

The deposit war is a fintech opportunity. Banks are desperate for deposits. CASA ratios are falling. Anyone who can help banks acquire or retain depositors, better savings products, embedded deposit features, yield-optimised offerings, is solving a ₹240 lakh crore ($2.5tn) problem.

Risk and collections infrastructure will see a demand spike. Even a mild uptick in defaults will trigger a buying cycle for early warning systems, collections automation, and restructuring workflows. Build for the stress cycle now, sell into the demand when it arrives.

Cross-border and trade finance is the sleeper. Supply chain disruptions from West Asia will force Indian businesses to rethink sourcing, hedging, and trade finance. Currency volatility is rising. Cross-border payment efficiency matters more. This is a problem that just became urgent.

Compliance-as-product wins. The Fino and HDFC episodes share a thread: the cost of compliance failure is going up. KYC on API partners, suitability checks on complex products, GST traceability through payment chains. Fintechs that build compliance as a core feature rather than a checkbox will win bank partnerships and avoid existential regulatory risk.

Indian banks are not taking enough risk. The data is clear: historical low, near-zero net defaults, record provision coverage, collapsing unsecured lending, booming gold loans. The system has overcorrected from 2018, aided by an RBI that learned the hard way what happens when banks run wild.

In normal times, I’d argue this is a problem. MSMEs are being rationed. Fintechs are losing their partnership foundation. Innovation is being throttled. Capital is sitting in provisions instead of funding growth.

But these are not normal times. There’s a conflict in West Asia. Oil is at $100. Supply chains are breaking. And the Indian banking system, almost by accident, is the most fortified it’s been in three decades.

The fortress was built for the last conflict. It might just save us in this one.

The real question comes after. When the crisis passes, will the system find the courage to take risk again? Will the RBI loosen the regulatory grip? Will banks start funding the economy’s potential, not just its safest bets?

That’s the conversation we’ll need to have. But not today. Today, we’re grateful for the fortress.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🎵 Song on loop

Fintech updates can get boring, so here’s an earworm: I’m forever fascinated by movies about space and space travel, so had to watch Project Hail Mary this past week. The movie had the song Winds of Change by the Scorpions (Spotify / Youtube) which I hadn’t heard in a while. Good nostalgia. Which is your favourite movie about space?

✨ Call outs

[Product Release] Union Square Ventures released its venture capital agents. Meet the Agents at USV: Arthur, Ellie, Sally, and Friends.

[Report] 2026 Market Overview by Hamilton Lane

[Post] The IMF Part 2 - How the fund actually works

[Report] India’s Data Centre Capacity to Grow 4x to ~4 GW by 2030

[TV Show] Shrinking - my latest favourite show, available on Apple TV.

👋🏾 That’s all Folks

If you’ve made it this far - thanks! As always, you can always reach me via DM at osborne.vc/dm. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.

This is a FANTASTIC post. Really helps frame investment thought into India. Thank you Osborne.

The Scorpions’ Winds of Change was a CIA operation…maybe

https://www.rollingstone.com/culture/culture-news/wind-of-change-podcast-990393/