The Userbase Conundrum | Edition #46 - 28th Nov, 2021

How many users should fintech startups have? I dive deep into user bases and identify how much is good enough. Details on digital banking regulations, Indonesian banking acquisitions and UPI charges.

Hi Insiders, Osborne here.

Welcome to the 46th edition of Fintech Inside. Fintech Inside is the front page of Fintech in emerging markets.

For weeks I've been thinking about today's post - how many users is good enough for Indian fintech startups? I was amazed at the numbers when I compared various public Indian financial companies. Today's post details out that finding and hope to lower expectations of most people from fintech startups.

There was also the Niti Aayog discussion paper on digital banking regulation. Unknown to most of us in India, Ajaib (Zerodha of Indonesia) acquired a 24% stake in a local bank, but Ajaib isn't the one to acquire a stake in a bank. There's details on that. Lastly, we all know that UPI is free, right? SBI Bank didn't think so. It's yet to refund $22mm for wrongly charging customers for UPI.

There's a lot in today's edition. Hope you find value in it. Don't forget to share on social or with a fellow fintech friend!

Enjoy another week in Fintech...

If you’re an early-stage fintech startup founder raising equity, I may be able to help - reach out to connect@osborne.vc

🤔 One Big Thought

The conundrum that is fintech startup user bases

India, as we know, is home to ~1.3bn people. As of 2020, 650-700mm Indians had access to the internet, 500-550 Indians had a smartphone and 200-250 Indians transact online. By 2025, India is expected to have 1bn internet users and 700-750mm online transactors.

These are large numbers by any stretch of imagination - especially for a single country. Of course when we see these numbers at a country level, we think to be a large business means having hundreds of millions of users. Maybe this is true for some businesses for example telecom, commerce etc. but its not for most businesses. It's not even remotely true financial services businesses.

Let's play a game.

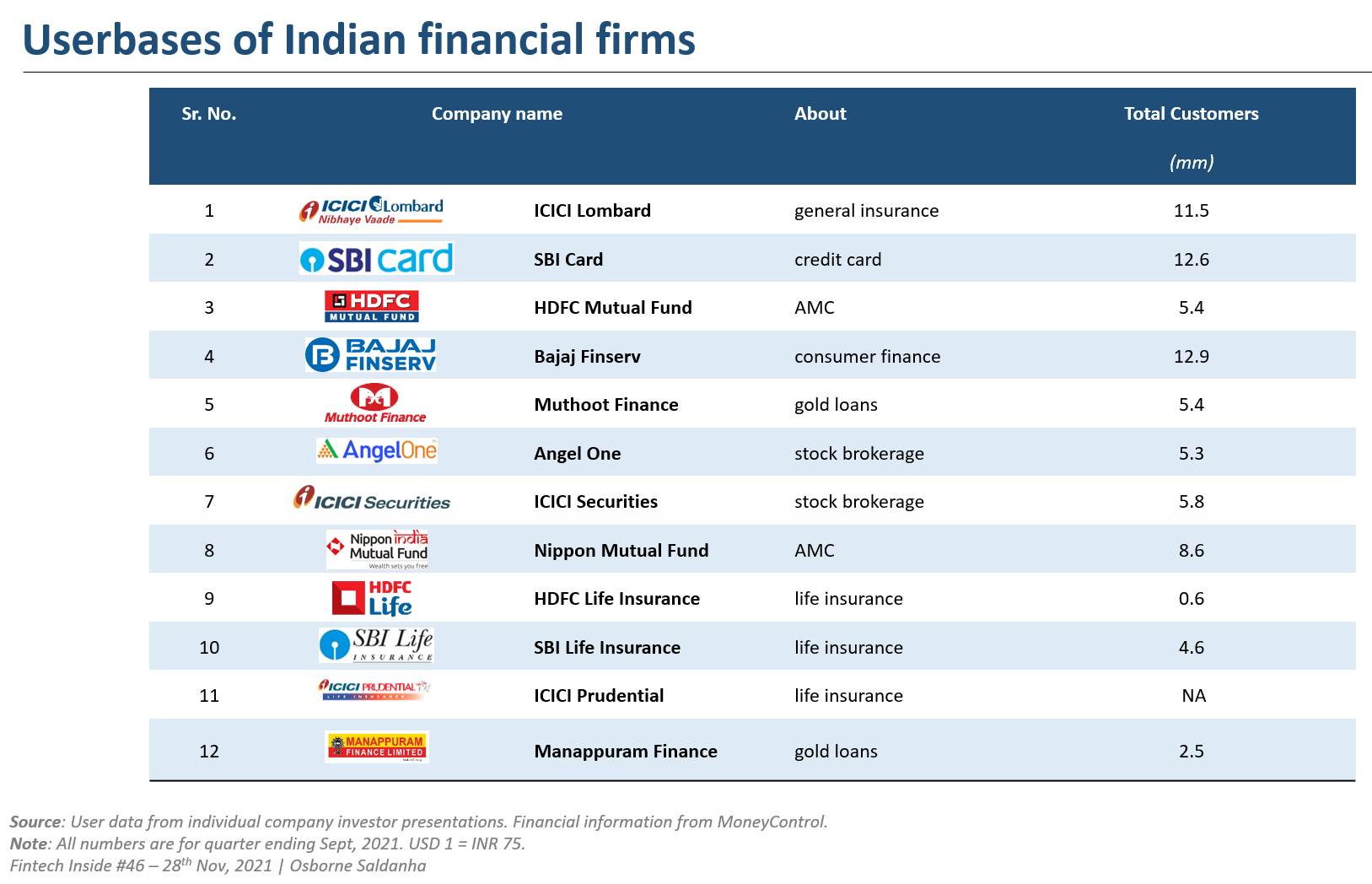

How many customers do you think these companies have? ICICI Lombard (general insurance), SBI Card (credit card), HDFC Mutual Fund (AMC), Bajaj Finance (consumer credit), Muthoot Finance (gold loans), Angel One (stock broker), ICICI Securities (stock broker and wealth mgmt.), Nippon Mutual Fund (AMC), HDFC Life (life insurance), SBI Life (life insurance), ICICI Prudential (life insurance), Manappuram (gold loans).

Once you've done your number crunching, guess what's the valuation of these companies.

As a subscriber of this newsletter, I can't let you do the work yourself. That's why you come to Fintech Inside, right? Have a look at the customers base of each of those companies.

You'll notice that all of them have less than 15mm registered customers. Heck, only 3 companies have a user base more than 10mm! Majority of the companies have roughly 5mm users. Also note, these are all registered users, not all are active users bases. Now look at the valuation of those companies.

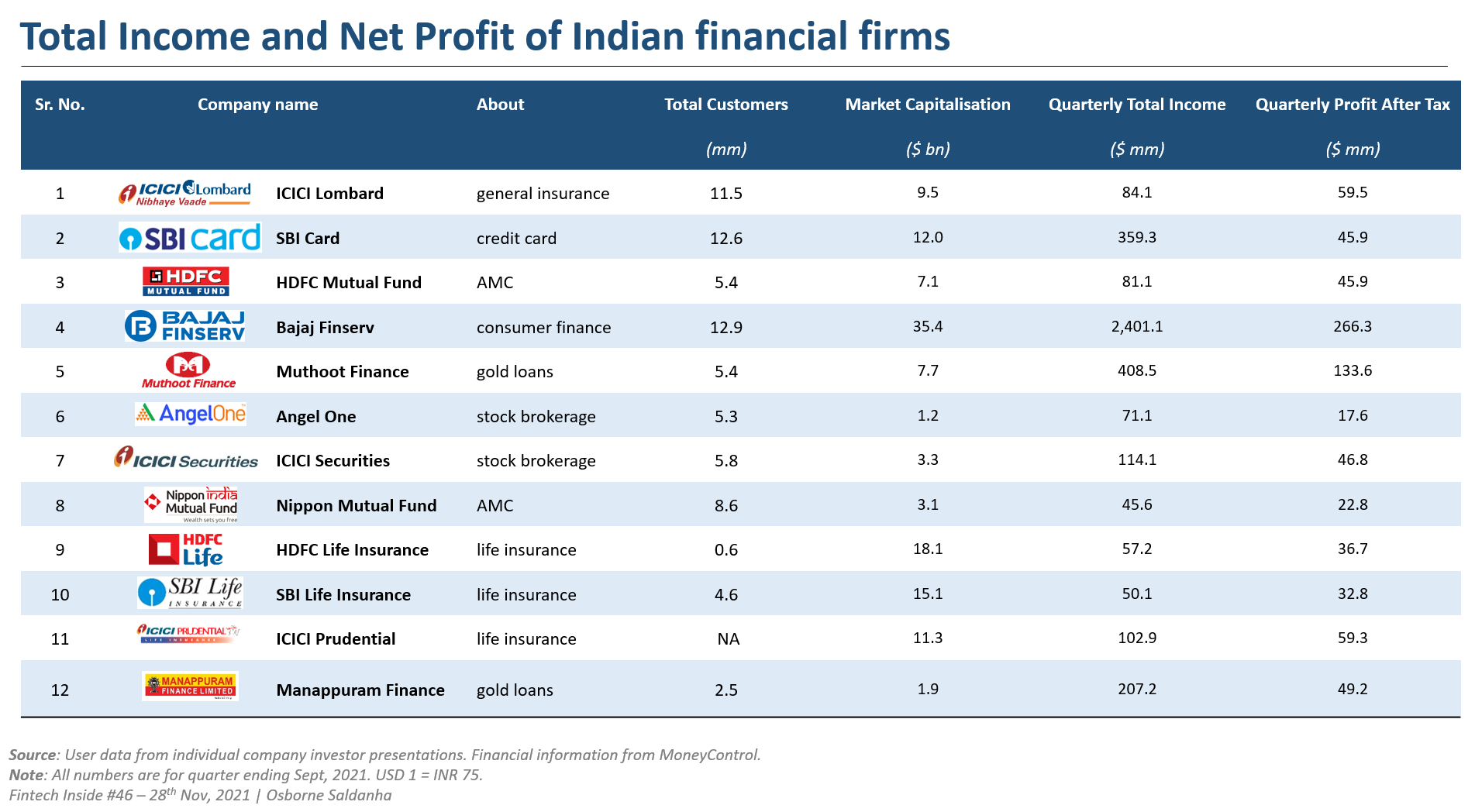

These are public market valuations, so I'm assuming market forces are at play here (not private VC valuations). This very crude analysis, values these companies, on average, at $~1.25bn (median = $0.95bn) per 1mm customers (excl. HDFC Life Insurance which seems an anomaly). Incredible, right?

Note: for this exercise, I've stuck to public financial companies and companies that have a some concentration to one business vertical. Banks are a tough beast to include in this analysis because 1) they don't give very clear numbers, 2) they have many other businesses that doesn't compare well here.

Just in case you're wondering though, as of the quarter ended Sept, 2021, HDFC Bank had 56mm registered accounts. HDFC Securities had 2.4mm customers. HDFC Credit Card had 15mm outstanding cards. SBI YONO had 43mm cumulative registered users. SBI Bank had 21mm mobile banking users. Bajaj's customer app has 13mm active users and 3mm wallet customers.

Of course, you might be thinking, "These are established financial firms, they have revenue and profit, unlike fintech startups". And you're absolutely right to think that. See the total income and profit of these companies.

A couple counter arguments to those thoughts:

Most of these financial companies are vertical entities of larger financial conglomerates. They have the distribution capability of their umbrella entity built in. In fact, you'll find very few financial companies (even outside these 12 companies) that make it large without the brand of a big bank. Fintech startups don't have this distribution luxury and are often shut out of partnerships with these financial firms.

These financial companies are operating traditional financial products with limited innovation. Fintech startups are innovating product, distribution, underwriting capabilities, pricing strategies and many more. There's no way to draw direct, apples-to-apples, comparisons with fintech startups and traditional businesses.

All this brings me to my "One Big Thought": Fintech startups don't need tens of millions of customers. Fintech startups could build very successful, profitable businesses with a couple million customers at max. It's a huge disservice to think/expect fintech startups to have hundreds or even tens of millions of customers just because they're building in/for India. These startups probably just need to go deep (not wide) and continue to offer value to these customers.

What do you think about this analysis - have a different point of view? I want to hear from you. Please write to me at email, Twitter or LinkedIn.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

💼 Work at a Fintech

workatafintech.com: Search from ~180 open positions at 50+ fintech startups in India and South East Asia.

Card91*, a card infrastructure startup, is hiring several senior positions including in sales, engineering, product and more. Apply here.

FlexiLoans, a SMB finance startup, is hiring an AVP of Supply Chain Finance. Apply here.

Tavaga, a robo-advisory startup, is hiring interns. Apply here.

Not on Work at a Fintech (yet), Bureau*, an identity, risk and fraud management startup, is hiring several positions across design, engineering, marketing, operations, product management and sales. Apply here.

Work at a Fintech is a community effort by EMVC. If you’re a Fintech who’s hiring I’d like to help. Write to me and I’ll put your requirement here. 2.5K+ people view these open positions.

3️⃣ Fintech Top Three

1️⃣ Will India soon have a digital banking regulation?

Niti Aayog, a government of India think tank, released a discussion paper on licensing and regulating digital banks in India. "This Discussion paper makes a case, and offers a template and roadmap for a digital bank licensing and regulatory framework in India". The paper talks about under-penetration of financial services in the country and how digital banking can address some of those issues.

It also suggests that digital banks cannot be offered a regulatory arbitrage and should be regulated, from a prudential norms and liquidity perspective, as universal banks but without the requirement for physical branches.

Takeaways: This is a big step in the right direction. While Niti Aayog is just a think tank, it does a lot of the "thinking" for the government. Even though Niti Aayog is addressing digital banking in the context of financial inclusion, it's important as this is a signal the RBI and the powers that be are definitely thinking of a digital banking regime. So far it's just been rumours. We're still 2-3 years (IMO) away from actual digital banking regulations though.

The discussion paper however seems to focus a lot on the SMB sector. In fact the discussion paper is proposing this digital banking regime to address a massive credit gap to the sector. The report claims that there are 64mm unincorporated SMB's in India, of which 99% are micro businesses and they create 110mm jobs. A large fraction of this sector continues to operate outside the ambit of formal finance.

The discussion paper goes on to propose a 2-stage approach to roll out the regulation: Stage 1 - Digital Banking Sandbox, Stage 2 - Establishing the regulation and issuing Digital Universal Bank Licenses. First, applicants will operate under the sandbox regime, with metrics (CAC, credit disbursal and performance, operations and more) closely measured so that the RBI can learn and improve its regulation. Based on the RBI's learnings from the sandbox, it will establish the final Digital Universal Banking regulation. The paper, loosely recommends the same regulatory requirements as a Small Finance Bank.

As a subscriber of this newsletter, you'd know I've addressed digital banking regulations several times over the past year. In each of those, I've tried bringing learnings from SEA digital banking and how it can be implemented in India. It seems Niti Aayog was reading the newsletter as well (I joke!).

2️⃣ Indonesian startups continue to acquire minority stakes in local banks

Ajaib, an Indonesian stock investment startup, acquired 24% shareholding in Bank Bumi Arta, a local Indonesian bank, for $52mm.

Takeaways: Firstly, about Ajaib: founded in 2019, Ajaib is among the largest stock brokerages in Indonesia, accounting for 1mm of the 2.7mm stock accounts. Think of Ajaib as the Zerodha of Indonesia. <1% of the total population participates in the stock markets. It's raised a total of ~$180mm and was Indonesia's fastest unicorn at its last funding round in Oct, 2021. The most fascinating part: the founder is 26 years old and co-founder 28!

Ajaib is not the first startup to acquire stake in an Indonesian bank. GoTo, Gojek and Tokopedia merged entity, acquired Bank Jago. Kredivo acquired 24% stake in Bank Bisnis Internasional. SEA Group's ecommerce arm Shopee acquired Bank BKE. Maybe I'm missing a few more. I don't think this will be the end - there will be more startups acquiring stakes in Indonesian Banks.

In fact, you'd remember I mentioned in Edition #35, that OJK, Indonesia's central bank, seems to prefer acquisitions as opposed to new licenses. "It's [minimum capital requirements] a huge barrier to entry for any new digital banking startup. But it seems the Indonesian regulator, OJK, here doesn't want new entities to launch from the ground up. It seems to want consolidation and conversion to digital banking possibly via acquisition by tech companies, as per its statement."

3️⃣ UPI is free but not to SBI Bank

SBI Bank is yet to refund $22.2mm charged to Jan Dhan accounts as UPI processing fees. The Bank collected $~34mm in fees for UPI transactions made between April 2017 and December 2019. SBI made part payment of $12mm so far.

Takeaways: IIT Bombay released a report some years back regarding these charges levied by SBI Bank on UPI transactions made by Basic Savings Bank Deposit Account (Jan Dhan) account holders. SBI Bank charged between INR 6-19 per UPI transaction beyond four a month! It's been two years since this report came to light and SBI is yet to refund this amount. Those account holders, typically rural people, probably don't even know they are due this amount from their bank.

I usually refrain from making extreme statements, but this is basically day time robbery. UPI is free - no charges are to be levied on the user and still the largest public bank in India charged those account holders exorbitant fees. SBI Bank is, of course, not the only bank guilty of levying charges at their will. In fact, had it not been for the IIT Bombay report, this robbery wouldn't have come to light.

Of all the dark patterns that our banks employ in their processes, the one the really gets me is that banks don't notify customers when a financial fee has been charged to their account. Annual fees, account fees, notification fees, GST etc - no SMS, no whatsapp text, no notification. Even though banks charge users for SMS notifications as well. /end rant

Looking for the news digest? Read all the week’s fintech news and updates in India and SEA over at This Week in Fintech - India and SEA Edition. You can also find our US, Global and European coverage.

🏷️ Notable Nuggets

👋🏾 That's all Folks

If you’ve made it this far - thanks! As always, you can always reach me at connect@osborne.vc. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.