97 and Free Fallin' | Fintech Inside #109

Three structural forces. Four acute shocks. One permanent new floor. The complete rupee breakdown for fintech founders.

Hi Insiders, I’m Osborne, an investor in early stage startups.

Welcome to the 109th edition of Fintech Inside.

I've been an investor in Indian startups for more than a decade. In that time I've watched the rupee grind from 64/$ to 83/$ - slow, predictable, almost boring. Every year, 3-4% weaker. Economists called it gradual depreciation.

The rupee hit 97 against the dollar this month. To put that in perspective: it took the rupee nine years to move from 64/$ to 83/. It took twelve months to move from 83 to 97/$.

It’s easy to worry, when the headlines call the rupee at 97/$ a crisis. The data tells a more nuanced story i.e. one where the rupee went from its most overvalued level in years to genuinely undervalued in just seventeen months. Both framings are partially true, and the distinction matters enormously if you're trying to build a business through it.

This edition is my attempt to cut through the noise. I'll walk through why the rupee fell, what the RBI has done and can and cannot do about it, and what the second and third order effects look like for startup founders. It's a long read but I think it's worth it.

Thank you for supporting me and sticking around. Enjoy another satisfying week in fintech!

Considering angel investing? I get a bunch of fintech founders reaching out to me for investors. I’d be happy to put you in touch. Send me a DM here.

🤔 One Big Thought

97 and Free Fallin’: Why the Rupee is falling and what it means for startups

A disclaimer worth making: I'm an early stage investor, not an economist or currency analyst. Everything here is my own analysis and interpretation, not financial advice, not investment advice, just one practitioner trying to make sense of a complicated picture.

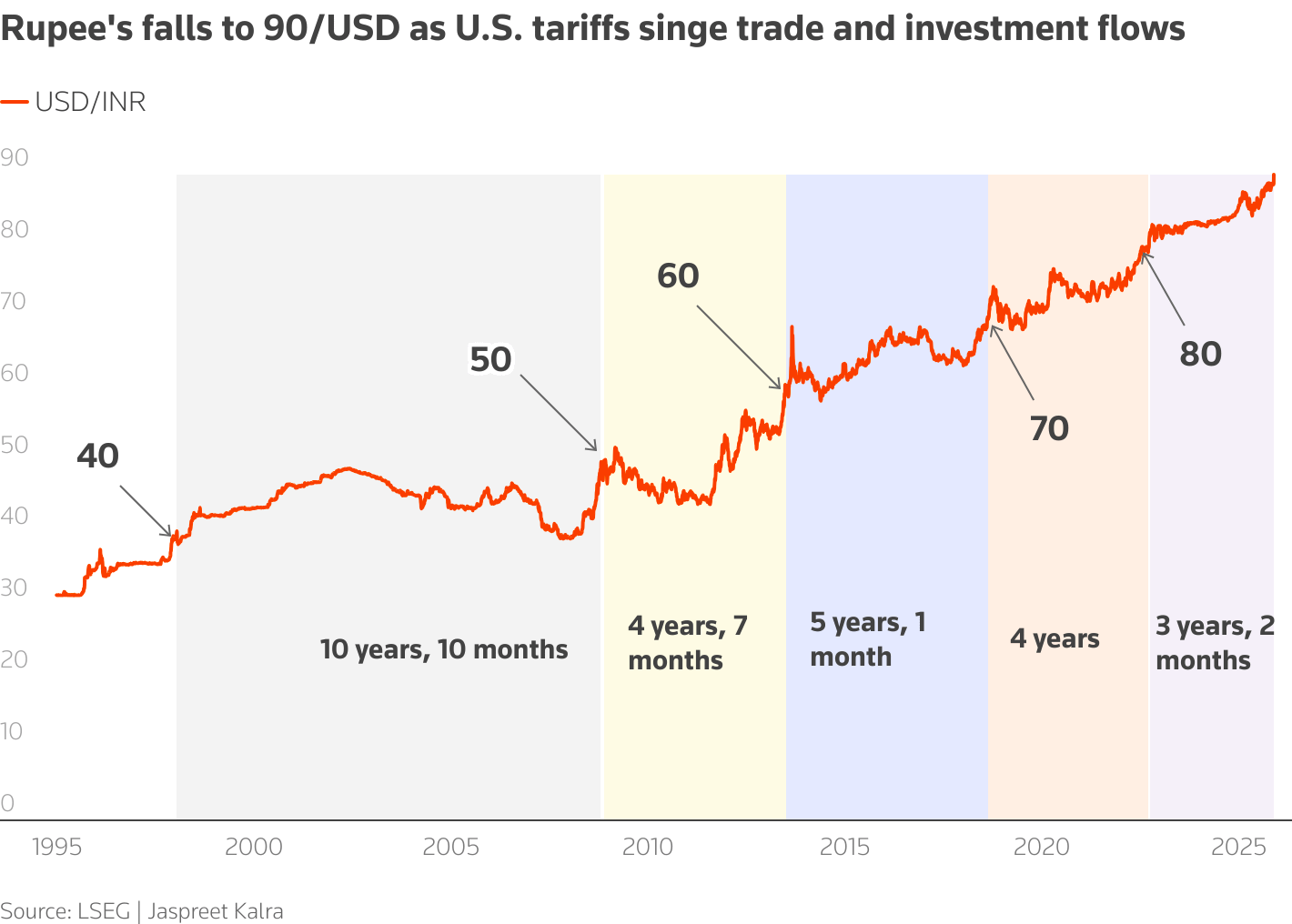

The rupee touched 96.9 against the dollar this month. That’s a record low.

Here’s what’s strange though, the rupee has been grinding lower for years. The 10-year data tells a clear story: 64/$ in 2015, 67 in 2016, 70 in 2019, 74 in 2020, 83 in 2023, 85 by end-2024. A slow, predictable decline averaging 3-4% a year. Economists call it gradual depreciation.

But 2025-2026 is different.

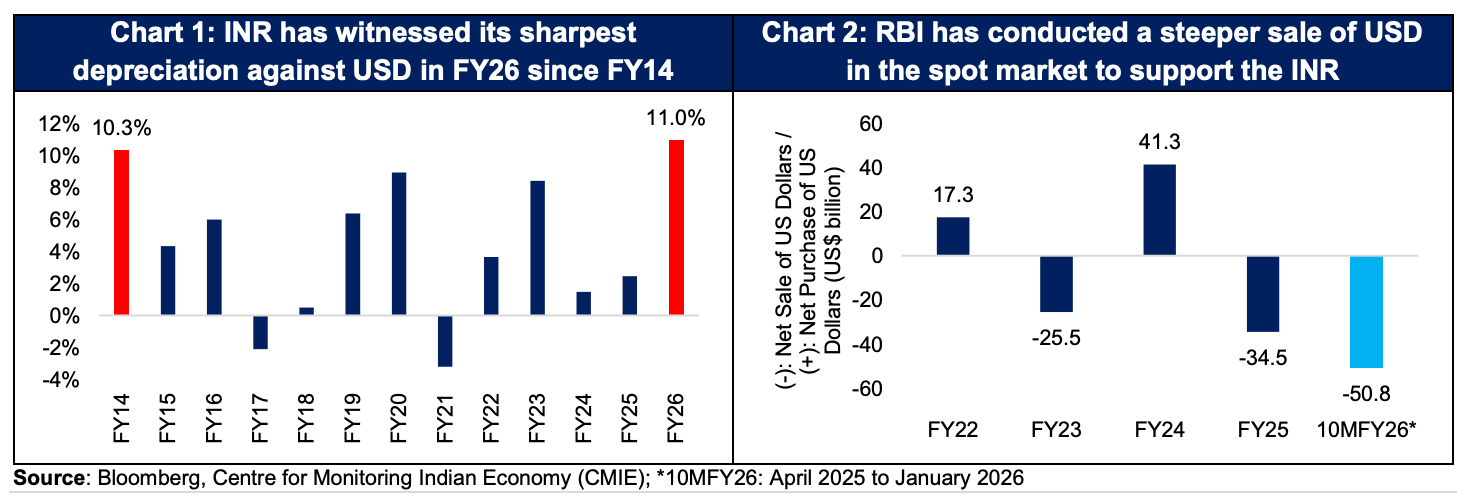

In the last twelve months, the rupee dropped from ~83/$ to ~97/$. That’s ~17%. More depreciation than the previous three years combined.

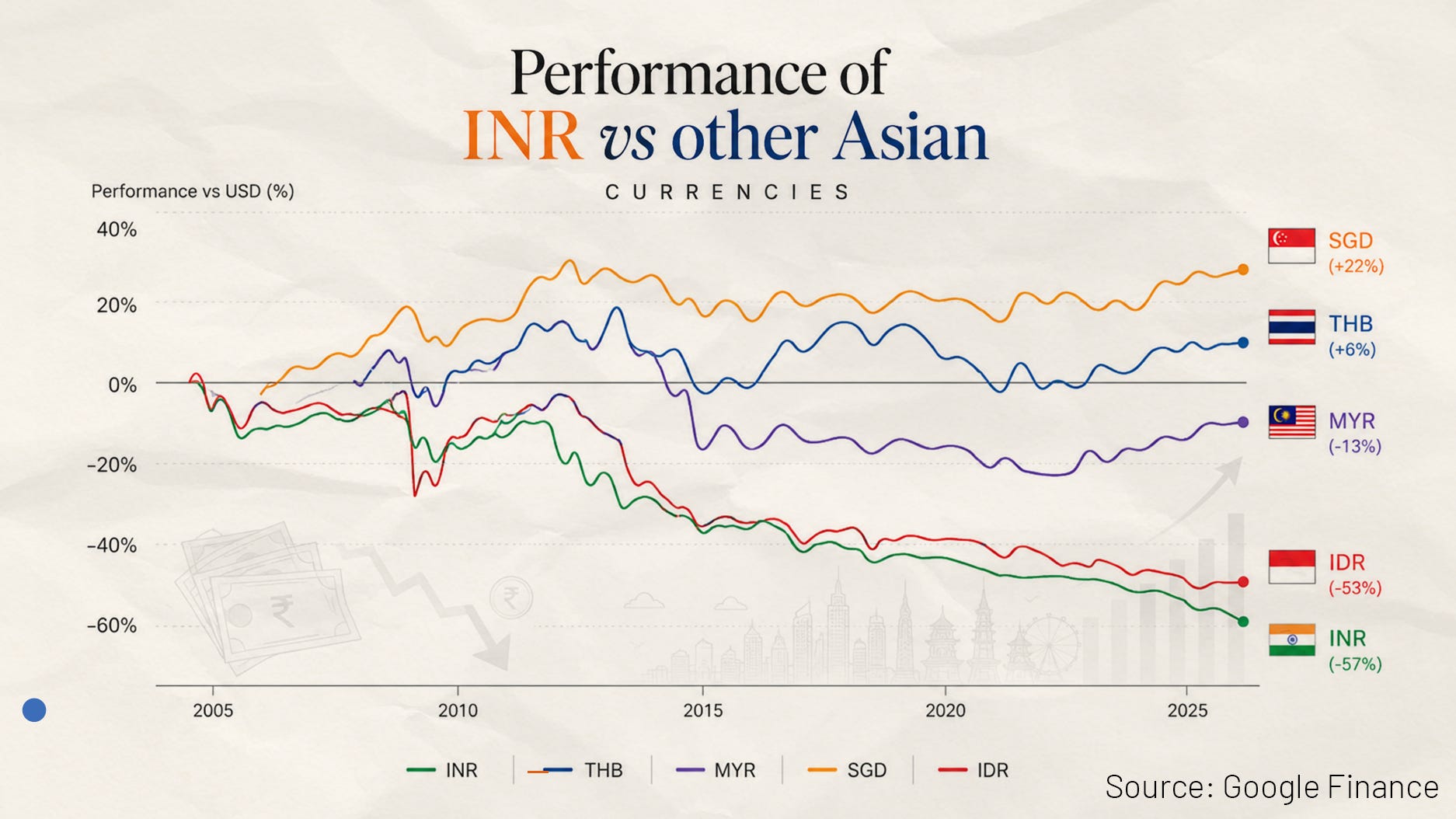

And that’s not all. The rupee weakened against most major currencies, not just the dollar. Against the Australian dollar, it fell 25%+. Against the Chinese yuan, ~20%. Against the Singapore dollar, ~15%. The only exception was the Japanese yen (3.5%) because the yen weakened alongside the rupee.

The rupee is Asia’s worst-performing currency in FY26 at 9.9%. It’s not a dollar story. It’s a rupee story.

Compare this to other emerging markets. Turkey’s lira lost 30% in 2023-24. Egypt’s pound fell 40% in 2024 alone. Nigeria’s Naira halved in 2024. These were crisis-level collapses driven by policy failures i.e. unorthodox monetary policy, capital controls, debt defaults. India’s 17% decline looks modest by comparison.

The difference is structural: India has $681bn in reserves, a Current Account Deficit (CAD) at 1.3% of GDP, and a coherent monetary authority. The rupee is weakening from a position of relative strength, not weakness. That makes this a correction, not a crisis. Either way, correction or crisis, it has implications for all of us.

My view is straightforward: It’s an acceleration and a convergence of forces that were building for years and hit all at once. The inflation differential. The trade deficit. US tariffs. The Iran conflict. An RBI that spent $53bn defending the currency and still couldn’t stop the slide.

For fintech founders and operators in India, this has direct impact on your P&L. Not in the distant future. Right now.

What Actually Happened

The structural baseline

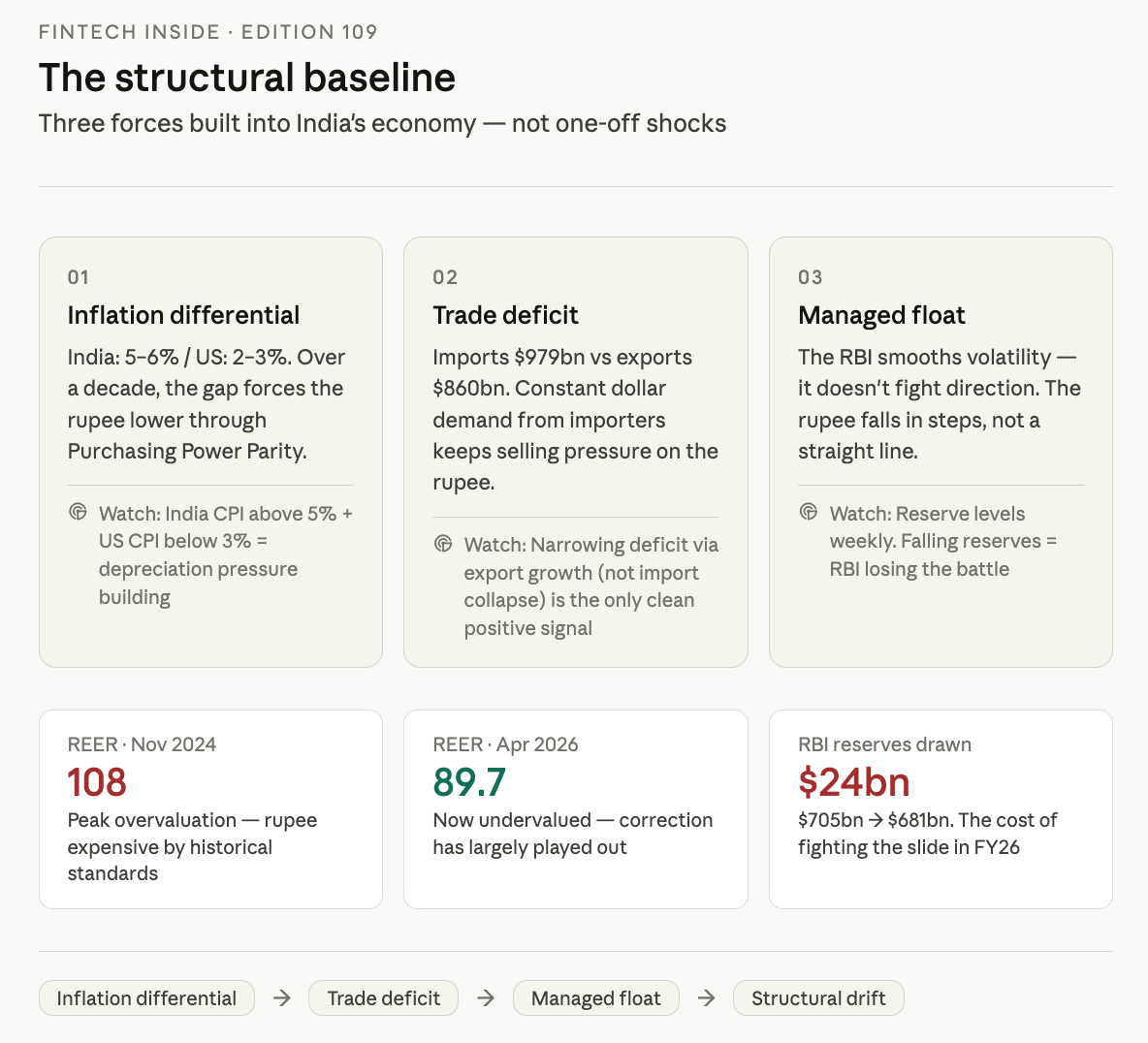

The rupee doesn’t fall by accident. It falls because of three structural features built into India’s economy.

First, the inflation differential. Inflation measures how fast the purchasing power of a currency erodes domestically. India runs inflation at 5–6% annually. The US runs at 2–3%. That gap sounds small. Over a decade, it isn’t.

If a basket of goods costs ₹100 in India today and $1 in the US, and India inflates at 6% while the US inflates at 2%, then in ten years that basket costs ₹179 in India and $1.22 in the US. For the exchange rate to reflect the same real purchasing power, the rupee has to fall to compensate. Economists call this Purchasing Power Parity. The rupee adjusts whether policymakers want it to or not.

Signal to watch: When India’s Consumer Price Index (CPI) prints above 5% and US CPI prints below 3%, expect structural depreciation pressure. When the gap narrows i.e. India’s inflation falls, US inflation rises, the structural drift slows. The RBI’s 4% inflation target exists partly to manage this. Every time it misses upward, the rupee pays.

Second, the trade deficit. The trade deficit measures the gap between what a country imports and what it exports. India’s total imports was $979bn in FY26 and total exports was $860bn. That $119bn gap creates a dollar demand. Importers need dollars; they sell rupees. More supply of rupees, less demand and the price falls.

Every Indian importer - an oil company buying crude, a manufacturer sourcing machines, a retailer importing electronics, needs to convert rupees into dollars to pay their foreign supplier. That conversion creates selling pressure on the rupee. When imports consistently exceed exports, the selling pressure is constant. More rupees chasing fewer dollars means the rupee weakens.

Signal to watch: A narrowing deficit, driven by export growth, not import collapse, is positive for the rupee. India’s electronics export surge ($48bn) is the most important positive signal in the current data. If that trajectory continues, it could reduce the deficit over 3–5 years.

The current account deficit (CAD) is the broader version of this, it includes services and remittances alongside goods trade. India’s CAD is at 1.3% of GDP, up from 1.1% YoY, which is manageable. In 2013, when the rupee last faced a comparable crisis, CAD hit 5% of GDP. That context matters: India is running the same depreciation pressure from a structurally stronger position.

Third, the managed float. Most people assume exchange rates are either fixed (the government sets the rate) or free-floating (the market sets it). China had earlier pegged its currency to the US Dollar until 2005. But the rupee is neither. It operates under a managed float i.e. the RBI intervenes to smooth volatility without committing to a specific level.

When the rupee falls sharply, the RBI sells dollars from its reserves to buy rupees, creating artificial demand that slows the decline. When the rupee strengthens too quickly, which can hurt exporters, it buys dollars to slow the appreciation. The RBI is not fighting the market’s direction. It is managing the speed of travel.

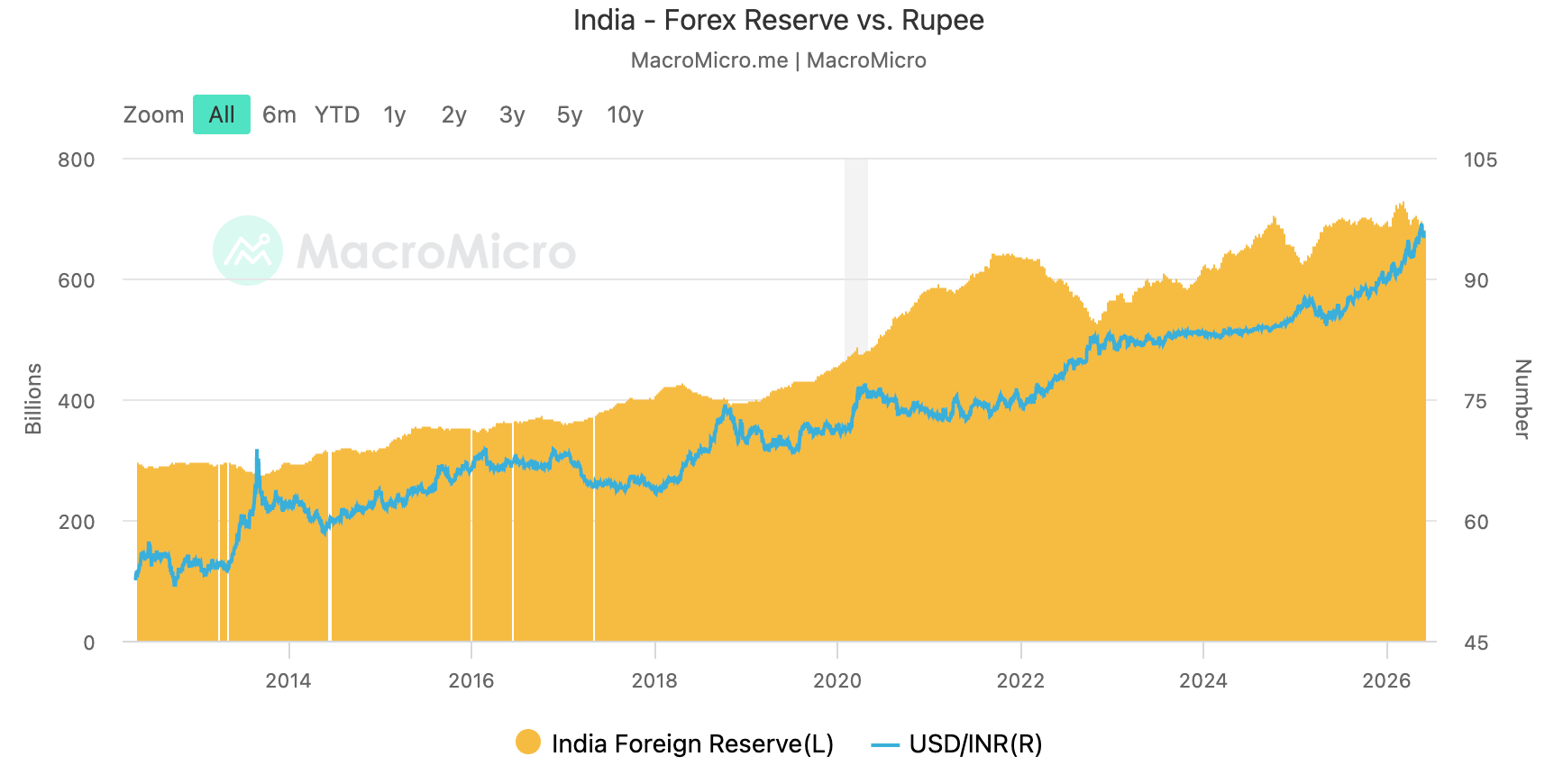

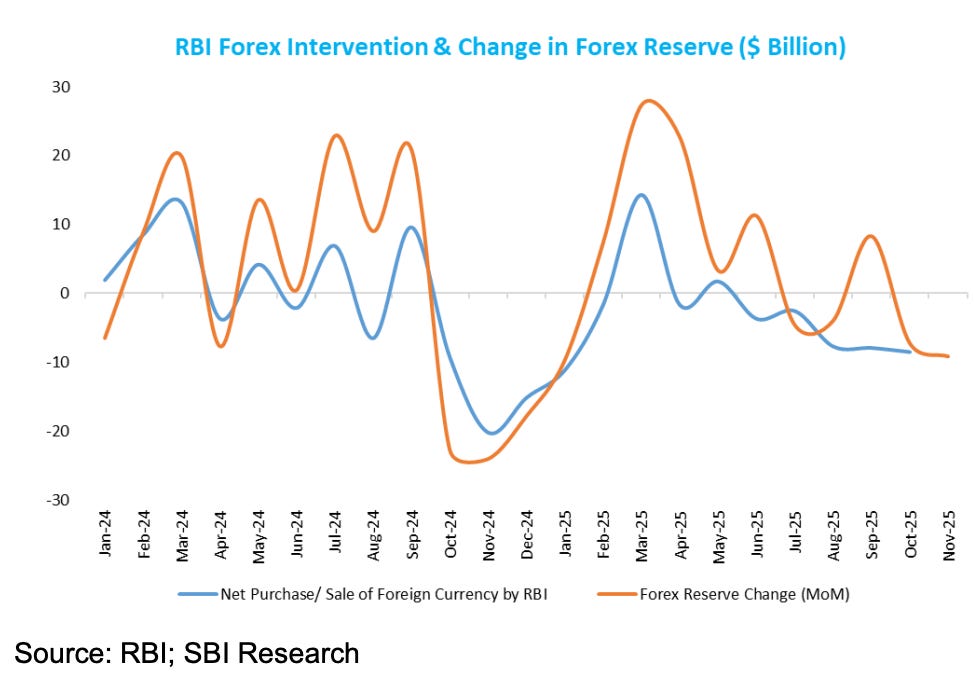

Signal to watch: RBI reserve levels are published weekly. When reserves fall sharply, the RBI is intervening i.e. burning dollars to defend the rupee. That is unsustainable beyond a certain point. India’s reserves dropped from $705bn in September 2024 to $681bn as of 22nd May 2026. That $24bn drawdown tells you how hard the RBI fought. When reserves stabilize or rebuild, intervention pressure has eased. When they fall consistently month-on-month, the RBI is in a losing battle.

The 40-year chart tells the story. Each crisis resets the floor lower. 1991, 2008, 2013, 2018. The pattern is consistent. The direction is one way. The managed float explains why the rupee falls in steps rather than in a smooth line - the RBI absorbs shocks and releases them gradually.

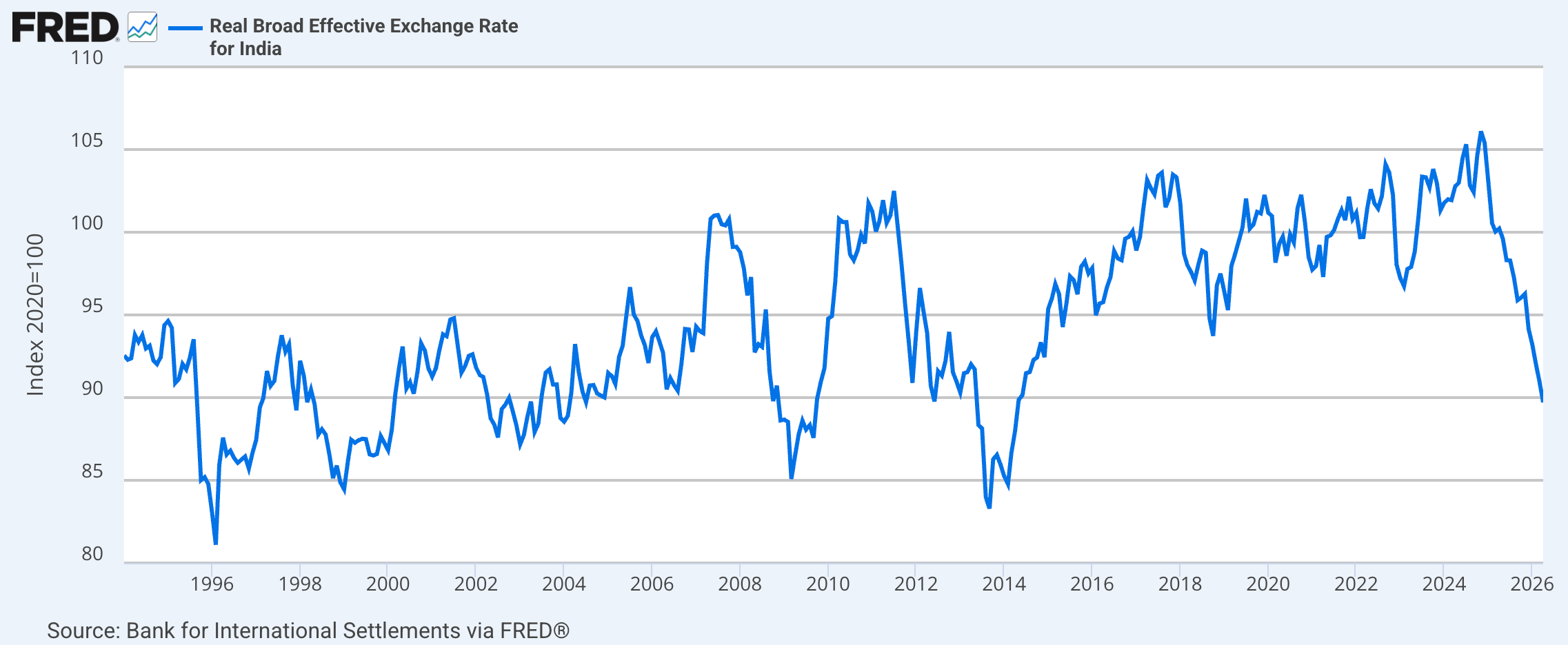

The REER context adds another layer. India’s Real Effective Exchange Rate (REER), a trade-weighted measure adjusted for inflation, stood at 108 in November 2024 (peak overvaluation). By April 2026, it had fallen to 89.7. The rupee went from most overvalued in years to undervalued in 17 months. This is what a real correction looks like, not a disaster.

The REER is an important currency metric most people should look at. It adjusts the nominal exchange rate (the 97/$ number you see on your phone) for inflation differentials across all of India’s trading partners, weighted by trade volume. It tells you whether the rupee is genuinely cheap or expensive relative to fundamentals, not just relative to the dollar.

A REER above 100 means the rupee is overvalued relative to its historical average i.e. Indian goods are expensive for foreign buyers, imports are cheap, exports are uncompetitive. A REER below 100 means the rupee is undervalued i.e. Indian goods are cheap globally, exports become more competitive, imports get expensive.

This is the number that reframes everything. The 97/$ rate feels like a crisis because it’s a record nominal low. But the REER says the rupee is now cheap by historical standards which means Indian exports are more competitive, the current account pressure should ease, and the structural case for further sharp depreciation is weaker than the headlines suggest. This is what a real correction looks like.

Signal to watch: REER data is published monthly by the RBI. When REER is above 105, the rupee is expensive and depreciation pressure is building beneath the surface. When REER is below 95, the rupee is cheap and the structural correction has largely played out. Where it sits today at 89.7, suggests the worst of the adjustment may already be behind us, even if the nominal rate drifts further.

The acute shock

What changed in 2025–26 wasn’t the structure but the shock that landed on top of it.

US tariffs. The US imposed 50% tariffs on Indian goods, the sharpest trade restriction since the 1990s. That spooked foreign investors. India is reportedly in the final leg of negotiating a better trade deal.

FPI outflows followed. Foreign portfolio investors pulled ₹1.6 lakh crore (~$18bn) out of Indian equities in 2025 alone. One of the largest annual outflows on record. Every exit meant selling rupees and buying dollars.

The Iran conflict pushed oil past $110 a barrel. India imports 88% of its crude oil. Every $10 rise in crude adds ~$15bn to India’s annual import bill, which in turn gets passed onto customers. More dollar demand. More rupee pressure.

The RBI fought back. It sold $53bn in the spot market in FY26, a record. It held $103bn in negative net forward positions. It intervened daily at an estimated $1bn. It even restricted Indian banks from trading in the offshore NDF market. None of it reversed the slide.

Rate cuts removed support. The RBI cut the repo rate four times in 2025 after retail inflation dropped to 0.25%. Lower yields meant lower carry trade appeal. Foreign investors looking for yield found less reason to stay.

The result: the rupee fell from ~83/$ to ~97/$ in twelve months. A 17% depreciation against a historical baseline of 3–4%.

What the RBI does next and what it means for us

The question I hear in every conversation: “Can the RBI stop this somehow?”

Short answer: it can slow the fall. It cannot reverse the forces that drive it.

Rate hikes are the big signal to watch. The next RBI Monetary Policy Committee decision is June 5. The RBI cut rates four times in 2025. It may now pause or reverse. A 25-50bps hike would restore some carry-trade appeal and slow the rupee’s slide. But it also raises your cost of capital. If you run a lending fintech, this directly compresses your net interest margins. If you are a cross-border platform, higher rates tell you the RBI is prioritising the currency, which is good for your business.

NRI deposit schemes could bring short-term relief. The 2013 playbook: the RBI raised $34bn through FCNR deposits by offering NRIs premium dollar-denominated rates. It could do the same now. Current FCNR rates offer up to 5.2% tax-free on USD savings. A new scheme could inject $10-20bn of dollar supply into the system quickly, stabilising the rupee without rate hikes. For fintechs serving NRI remittances, that means more volume flowing through formal channels.

Reserve depletion is a wasting asset. The $53bn spent in FY26 bought time. At $110 oil, the monthly burn is $20-30bn. Reserves are $681bn and dropping. The RBI can sustain this for another quarter, maybe two. But not indefinitely. As reserves drain, the psychological buffer shrinks. Markets notice.

What the RBI might not do. It might not defend a specific INR level. It will not raise rates aggressively just for the currency. The MPC has consistently prioritised growth over rupee stability. The rupee can drift to 100/$, slowly, not suddenly. That is the managed float working as designed.

Bottom line for founders: The policy toolkit can slow the rupee’s fall and prevent a disorderly crash. It cannot change the structural drift. Assume the rupee stays in the 95-100/$ range for the next 12-18 months. Anything better is a tailwind. Plan for worse.

The other side

A reasonable person could disagree with this framing. Let me state the strongest version of that argument.

“The rupee’s fall is temporary. It stabilises when the Iran conflict de-escalates and oil prices normalise. The RBI has $681bn in reserves, plenty of firepower. India’s macro fundamentals i.e. GDP growth at ~6.5%, CAD at 1.3% of GDP, record exports and so on, are nothing like the 2013 taper tantrum when CAD hit 5%. The rupee returns to 85/$ within two years.”

I think this argument is wrong, but not unreasonable. Here is why the structural argument holds more weight.

The structural drivers predate the Iran conflict and will outlast it. The inflation differential. The trade deficit. The 86% of India’s trade still invoiced in dollars. These don’t go away when oil prices drop.

What the oil shock and tariffs did was accelerate a trajectory already in motion. The question isn’t whether the rupee stabilises. It’s where the new floor settles. ING’s May 2026 forecasts show the rupee recovering slightly to 94/$ over 12 months, a 4% improvement from current levels but still well above 85/$. BMI expects 95/$ by end-2026. MUFG and Aberdeen warn 100/$ is possible if Strait of Hormuz tensions escalate.

What would change my mind? Two things. First, if India’s export diversification continues i.e. electronics exports at $48bn, smartphones at $30bn, and reduces the structural dollar demand for imports. Second, if rupee invoicing of trade expands beyond the current 2–3% share. Both are positive trends. Both are early.

What this means

Layer 1: Consumers: A cheaper rupee hits consumers through three channels and they all compound.

Inflation channel: India imports 88% of its crude oil and 60% of its edible oil. Every 10% rupee depreciation adds roughly 1-1.5% to headline inflation. That flows through fuel, transport, food, and manufactured goods. The consumer feels this at the petrol pump, the grocery store, and the monthly electricity bill. Discretionary spending gets squeezed first.

Imported goods channel: Electronics, smartphones, gold, and machinery all get costlier. A MacBook that cost ₹1.2 lakh at 83/$ now costs ₹1.4 lakh at 97/$. Gold, a traditional savings vehicle in Indian households, becomes more expensive to buy. This shifts consumption patterns toward essentials and away from aspirational purchases.

Savings channel: Rupee savings held in cash or fixed deposits lose purchasing power relative to global goods. This pushes savers toward inflation hedges i.e. gold, real estate, or dollar-linked instruments. We are already seeing this. Gold demand in India rose 15% in FY26 despite record prices - as discussed in Edition #102.

Layer 2: Consumption: The chain is predictable. Higher inflation reduces real disposable income. India’s per capita income grew at roughly 9.5% nominally over the last decade, but strip out 5% average inflation and real income growth is closer to 4.5%. That 4.5% was already thin. A rupee that adds 1-1.5% to headline inflation doesn’t just slow real income growth, it cuts it nearly in half. The sectors that feel it first are travel, dining, entertainment, automobiles, and consumer durables. Discretionary spending is the first casualty of a currency correction.

This matters for fintech because consumption drives transaction volume. UPI payments, credit card spends, BNPL usage, all correlate with consumption. If consumption slows, payment volumes dip. The fee income that fintechs earn per transaction shrinks at a time when they need it most.

For lending fintechs, the picture is worse. Consumption slowdown means lower credit demand. At the same time, the RBI may raise rates to contain inflation. Higher rates mean higher EMIs, which further suppress demand. It’s a contractionary spiral.

Layer 3: Credit: A weaker rupee impacts credit markets in four ways.

Higher rates: If rupee depreciation pushes inflation above the RBI’s 4% target, the central bank pauses its rate-cutting cycle or reverses it. This raises the cost of funds for every NBFC and bank. As of April, 2026, Indian banks already raised lending rates by 10 basis points to 8.50%. Credit growth will slow.

Higher NPAs: Businesses that import raw materials or carry dollar-denominated debt, face higher costs and compressed margins. Some will default. Retail borrowers face higher EMIs and higher living costs. Delinquencies rise.

Tighter underwriting: In response, lenders tighten credit standards. Fewer loans get approved. The credit-to-GDP ratio, already below its trend, slips further. This hit to financial inclusion is real especially for the thin-file borrowers fintechs have been targeting.

Secured loan boom. One side effect: as gold prices rise (driven by both global demand and rupee weakness), gold loan providers like Muthoot and Manappuram benefit. Loan-to-value ratios improve. More households monetise their gold holdings to manage cash flow. Couple that with mutual fund SIPs growing to record levels of $3bn monthly, investors will start leveraging their MFs to take secured asset-backed loans as ell. This is one of the few credit segments that will get stronger.

Layer 4: startup ecosystem: Beyond fintech, a weaker rupee reshapes the entire startup landscape.

Dollar costs rise for everyone: Indian startups run on global cloud providers, AI labs, Stripe, SaaS providers and more - majority priced in dollars. A 15% rupee depreciation means a 15% jump in cloud infrastructure costs. Burn rates could go up. Runways shrink.

Foreign talent gets more expensive: Startups hiring senior talent from the US or Europe in dollar terms face higher INR costs. Remote-first companies that pay in USD see their wage bill expand in rupee terms. Obviously this impacts Indian domiciled startups.

Fundraising math changes: Foreign funds compute returns in USD. A 4% annual rupee drift means every fund needs to earn a 4% higher nominal return in INR to deliver the same USD return. This doesn’t kill the India thesis, but it tilts the playing field toward dollar-earning business models (cross-border SaaS, digital exports) and away from domestic-consumption-dependent ones (hyperlocal delivery, domestic BNPL, D2C brands with imported inputs).

The IPO window narrows: A weaker rupee often correlates with FPI outflows. FPIs outflows from the equity market crossed ₹2.25 lakh crore ($23.7bn) as of May, 2026, surpassing the ₹1.66 lakh crore ($17.5bn) withdrawn during all of 2025. This means lower valuations in public markets. Domestic IPOs get postponed. That delays exit timelines for early-stage investors. The liquidity crunch in the startup ecosystem lasts longer.

The Second-Order Effect

If the rupee continues toward 100/$, the RBI faces a classic “trilemma”. It cannot simultaneously manage the currency, control inflation, and keep rates low. Something breaks.

The most likely outcome: the RBI prioritises inflation control over growth. Rates go up. Credit slows. Consumption weakens. The startup funding winter, which looked like it was thawing, gets another season.

The less likely but more dangerous outcome: the RBI lets the rupee find its level while keeping rates accommodative. That risks imported inflation becoming entrenched. Inflation expectations de-anchor. The cost of fixing it later, through sharper rate hikes and deeper recession, is much higher.

What this means for founders and investors?

The rupee at 97/$ is not a single event. It is the visible surface of forces that have been building for years i.e. the inflation gap, the trade deficit, the dollar dependency, and accelerated by shocks that may or may not persist.

The founders who navigate this well will not be the ones who wait for the rupee to recover. They will be the ones who build assuming it doesn’t.

That means a few concrete things. If your cost base is in dollars, model your burn at 100/$, not97/$. The psychological buffer of “it can’t get much worse” is not a treasury strategy. If your revenue is in rupees and your customers are discretionary consumers, assume transaction volumes soften over the next two quarters as real incomes get squeezed.

The rupee correction has largely played out in REER terms. The structural drift hasn’t. Those are two different statements, and conflating them is where most analysis goes wrong. The worst of the acute currency shock may be behind us.

We might have to shift our focus on the other external shocks to the market i.e. the Iran war potentially goes on for longer which could cause oil prices to spike further, spiralling into higher inflation, lower consumption, lower credit growth and higher defaults. Oh and let’s not forget the AI causing higher expenses for enterprises which might force them to cut costs by laying off employees, which will have its own ripple effects.

We can’t seem to catch a break since 2020. The slow grind is permanent. Lage raho!

I want to hear the counterargument. If you think I’ve got this wrong, if you believe the rupee strengthens from here, I’d love to hear from you. I’ll publish the best responses in a future edition.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🎵 Song on loop

Fintech updates can get boring, so here’s an earworm: Today’s title is inspired by Free Fallin’ popularised by John Mayer (Youtube / Spotify). This rendition is performed at the Nokia Theatre for his popular Where the Light Is Tour. If you haven’t watched the live performance video of that concert, I’d recommend it. Soul soothing.

Call outs

Links to non-fintech content I found super interesting:

[REPORT] India VC Exit Performance

[ARTICLE] DeepSeek’s 10 trillion USD grand strategy

[REPORT] SpaceX S-1 Breakdown

[VIDEO] The Geometry of Luck by Soleio at the Tokyo Design Forum

[VIDEO] How Jazz and Improvisation Works

👋🏾 That’s all Folks

If you’ve made it this far - thanks! As always, you can always reach me via DM at osborne.vc/dm. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.