Decoding Block | Fintech Inside - Edition #67 - 19th Sept, 2022

Are you excited for Fintech Happy Hour in Mumbai? I am! See you there. Also, there's a breakdown of Block's financial ecosystem, written by Dinesh Vernekar.

Hi Insiders, I'm Osborne, Principal at Emphasis Ventures (EMVC).

Welcome to the 67th edition of Fintech Inside. Fintech Inside is the front page of Fintech in emerging markets.

Fintech Happy Hour presented by IDFC First Bank is happening this week! I’m super excited to see the Mumbai fintech community come together! Going by the sold out registration, I’m sure this will be one to remember! See you there!

This week’s Fintech Inside is a cross post of a blog by Dinesh Vernekar. Dinesh decodes Block - the financial behemoth that’s built a uniquely 21st century financial platform serving merchants and consumers.

If you’re an early-stage fintech startup founder raising equity or debt, I may be able to help - reach out to connect@osborne.vc

Enjoy another week in fintech!

✨ Fintech Happy Hour

It’s Fintech Happy Hour week! I’m excited to meet everyone that registered to join us on Thursday, 22nd Sept for the Mumbai Fintech Happy Hour presented by IDFC First Bank.

The passes are completely sold out and I cannot accept any further registrations (venue capacity limits). If you registered earlier, you will receive calendar invites to block your time along with the venue details.

Huge thanks to all the sponsors of Mumbai Fintech Happy Hour - IDFC First Bank, Tartan, Tether by M2P and Pazcare.

Haven’t registered? I’ll be attending the Global Fintech Fest on Tuesday, Wednesday and Thursday - would love to meet. Send me a note at connect@osborne.vc and we’ll set up some time.

🤔 One Big Thought

Decoding Block – Cash App & Square

Note: Today's edition is a cross-post of a blog written by Dinesh Vernekar. He's the Head of Product at OneCard and writes a lot of deep dives from a product perspective. Follow him and his insights. This post has been lightly edited for brevity and space constraints.

Block is one of the most interesting fintech businesses in the US and the world. It is also one of the few companies with a successful consumer (Cash App) & B2B Play (Square).

In this post I’ll be focusing on the following aspects:

Beginning and going upmarket

Terrific growth

Network effects & moats

Big consumer & B2B plays

Effective monetisation

This might be a good read for product, marketing and business managers trying to monetise their products, build virality and lower CAC, create lock-in and overall build more sustainable businesses.

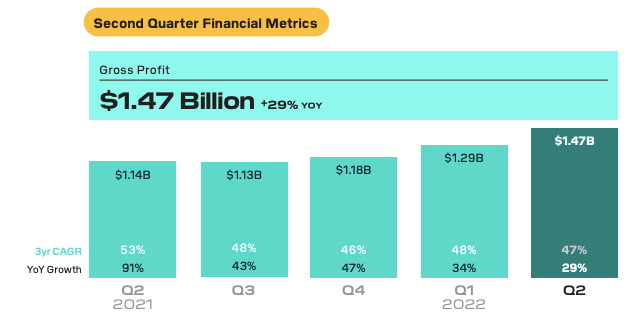

Let’s start with Square's financial performance.

In the quarter reported for Q2 2022, Block had a gross profit of $1.47B with a 29% growth in profit year on year.

Block comprises of 2 main companies –

Cash App – A P2P payments and services app.

Square – POS and other services for merchants.

Reiterating my point on the strength of its consumer and business verticals, they generated an almost equal amount of gross profit from both businesses with both showing about 30% growth YoY.

Let’s get started and understand the evolution of Square.

1. Beginnings & going upmarket

Square started in 2009 to enable anyone with a mobile device to accept card payments. And unlike a lot of tech companies, it went public 6 years later in 2015. In 2015, they processed a $35.6Bn in payments value (GPV) with 712mm payments from 190mm unique cards. Just 7 years later, GPV has grown to $152.8Bn with over 3Bn payments from 526mm cards. The GPV alone has grown at 23% CAGR. But how did Square enter an existing market? Let’s understand.

As a new company in the POS space, Square had the following approaches available to enter into the POS market –

Hardware

Hardware + Software

Software only

As I mentioned in my post on QR codes, POS infrastructure is typically expensive and thus a big hurdle for adoption by merchants. A typical device in India costs about Rs. 10,500 ($131). The best approach is to use software only and use the mobile phone as a complete mobile acceptance device. A mobile app can be used to recognise the card using NFC and then authorise the transaction using a pin. However most mobile devices don’t have NFC technology and this leads to an incomplete solution – a strict no-no in payments technology.

Square was able to circumvent this limitation by focusing on its reader device. Instead of being a standalone app, it created a device to connect to your iPhone or iPad and start accepting payments.

Thanks to Square reader’s ease of getting started, distinctive design and no fees for the reader, Square was able to quickly onboard smaller merchants.

If we check their seller network in 2015, we can see the smaller merchants with a GPV of less than $125k accounted for a majority (61%) of its customers. This is excluding Starbucks as the biggest merchant on their network.

Over a period of time, this GPV mix changed considerably with the range of products also offered changing from just the magstripe reader to a host of POS solutions for merchants of all sizes and shapes. By 2021, Square has been able to change the GPV mix with 37% GPV coming from large merchants in Q4 2021. Not bad for starting out focusing with a simple reader.

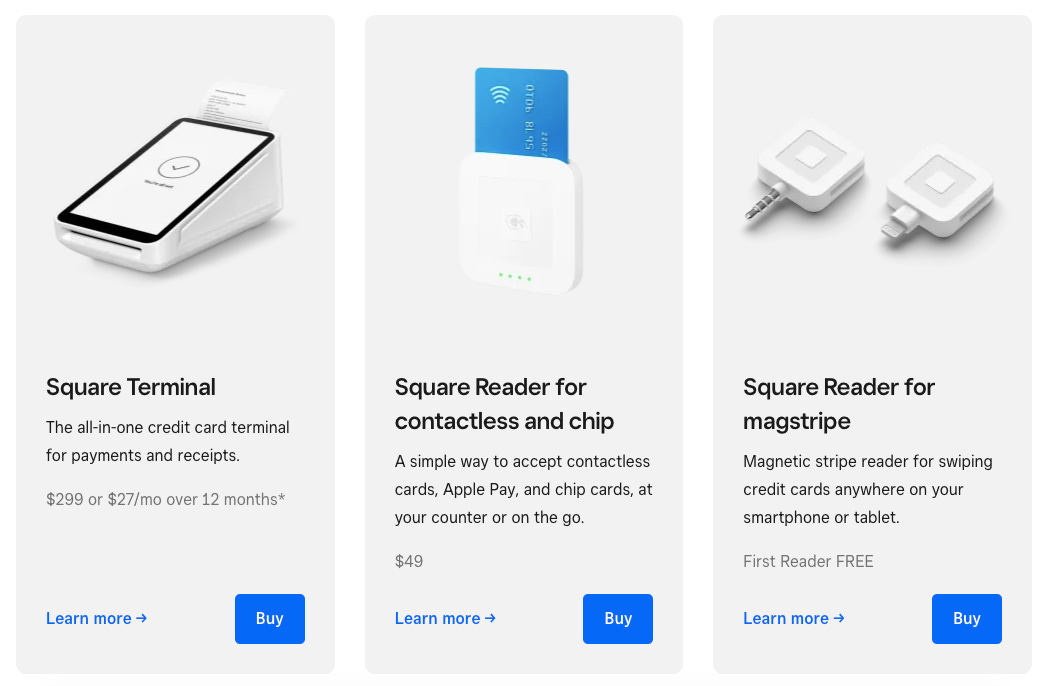

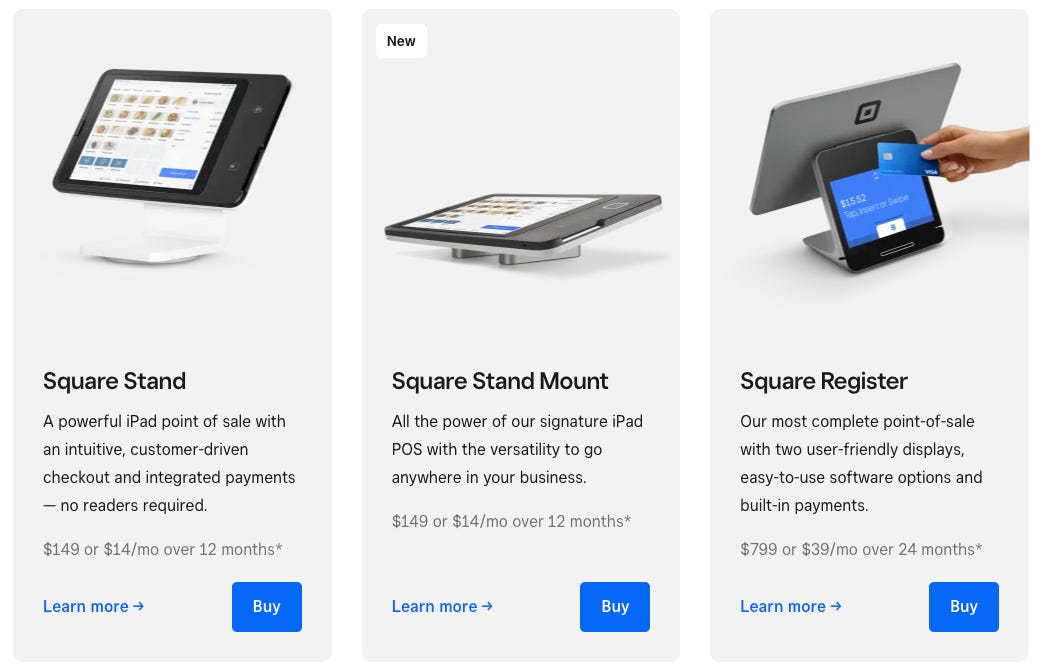

Square has now expanded from offering just payment accepting devices to offering an entire set of services to manage payments, customers and invoicing.

Current set of POS devices offered by Square at different price points:

If we look at the above set of devices, the common thread is using the power of the iPad or iPhone to power payments. Also from a price point perspective, from free to $799/month, Square is able to cover different needs for merchants of all sizes. In another post, I’ll cover the following dimensions to expand their merchant base. Square is currently using a mix of them.

Vertical approach – one category

Horizontal approach – one set of business

Small & Medium Business (payment volume less than X & order value Y)

Big merchants

2. It’s terrific growth

The second most remarkable thing about Block, is Cash App's terrific growth trajectory. At last count, Cash App had 80 million (26% of US population, last updated on 22nd May 2022) users monthly transacting on their app for a variety of services from P2P payments, P2M payments, neo-banking, stock broking, crypto investments and more.

This is even more remarkable if taken into consideration that it entered the market when Venmo, Paypal and other giants had captured sizeable market share. Payments was thought of as a largely solved problem. Cash App started with a simple promise to send and receive money. This once again proves that the largest opportunities lie in the core business and if one can find a GTM to attack the market, the returns can be huge.

If one checks out the initial reports and investor presentations, its quite clear Square Cash was one of several bets. However its growth has been nothing short of remarkable.

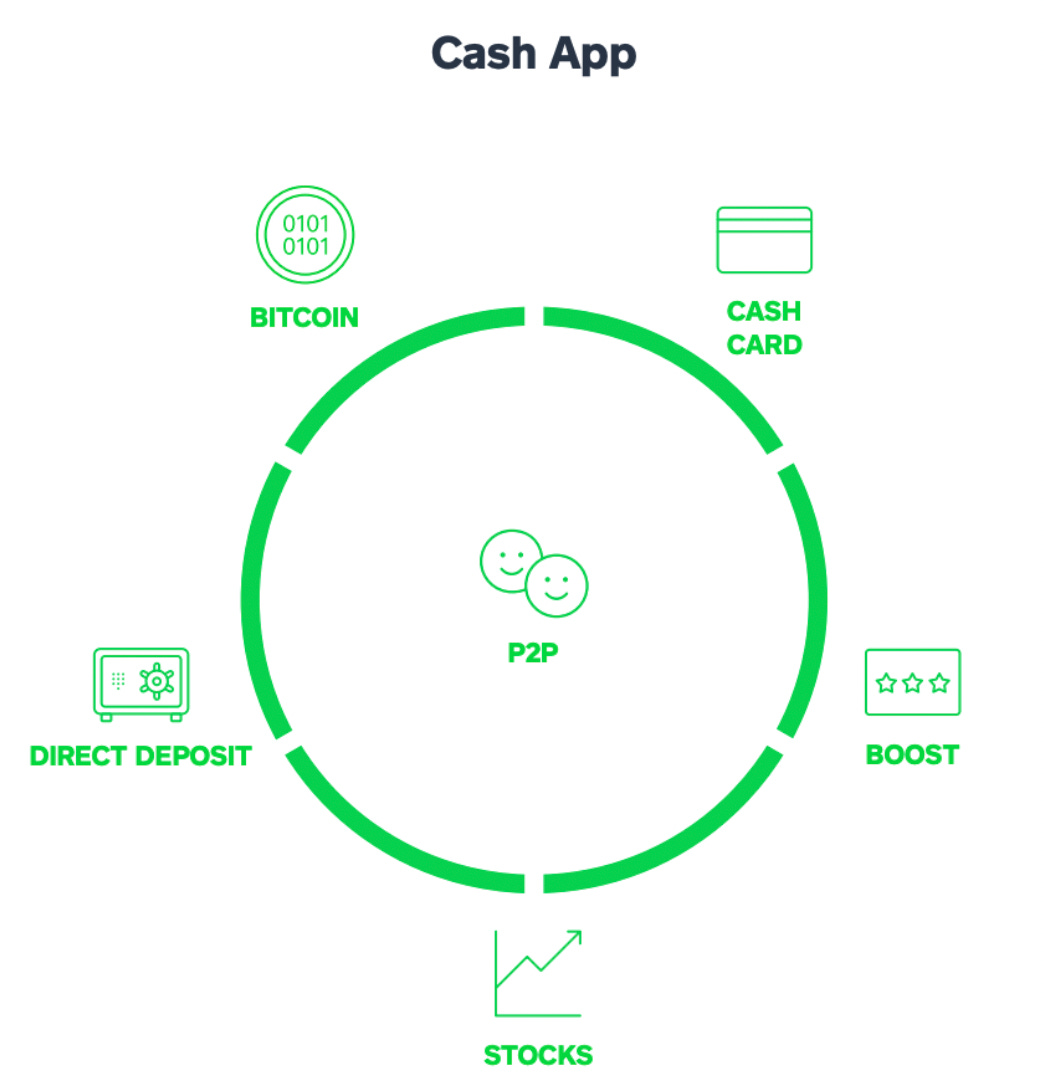

Let’s understand the product offerings of Cash App.

The core value proposition is P2P transfer and Cash App was launched with this proposition in Oct, 2013.

This is very similar to the experience we currently experience with Gpay/PhonePe in India, but one has to consider in the US P2P transfer isn’t exactly solved. Thus if you’re looking to pay/get paid for odd jobs, Cash app is perfect.

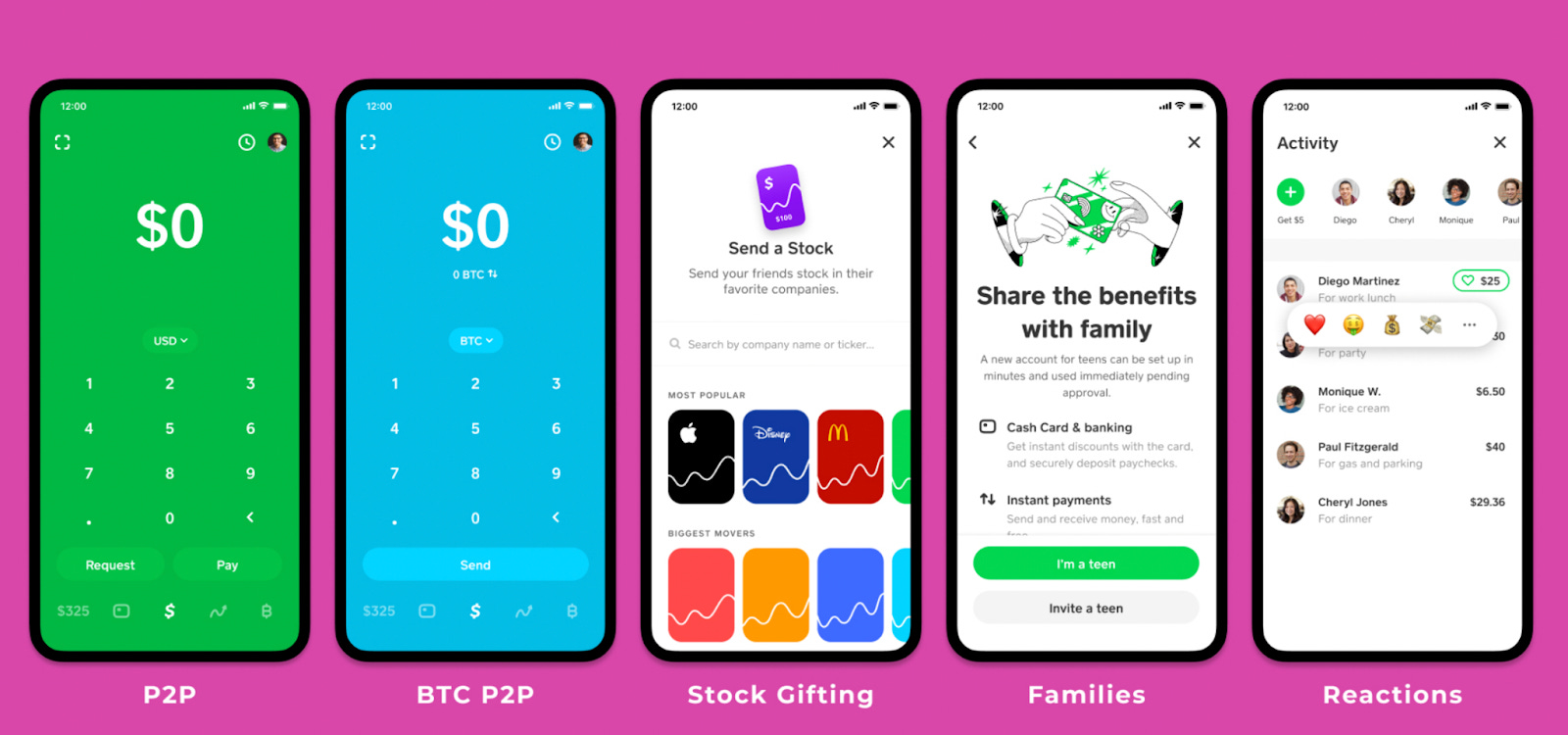

Over time this proposition has grown to add a rewards program (Boost), bitcoin trading, stock trading, debit card (cash card) and direct deposit.

A big part of this growth has been its ‘network effort’. Cash App is probably one of the big examples of successful referral marketing. But they’ve taken it to a new level. In India Gpay too paid paid out a cash reward for sending money to a new customer. Unlike other reward programs where the focus is just on downloading the app, here GPay was able to uniquely link their Google account with their bank account & UPI handle creating an immensely powerful network..

But there’s a second part to this trick. Cash app also uses influencers to give out cash to users using their $CashTag. The lure of quick cash enables a lot of users to create their accounts.

While the contribution of these campaigns to their marketing is unknown, it does have an enviable CAC in the industry with $10 compared to insanely high acquisition costs for its competitors.

Further expansion with a range of products:

Cash app pressed on the advantage in all 3 areas – a. Acquisition (by building products with inherent network effects) b. Engagement – high engagement products like Cash Card c. Monetization (as we’ll explore in the blog later)

3. Moat & network effects

Over the last 2 years, I’ve spent a larger amount of time thinking about the ‘MOAT’ of a business. In internet businesses, it’s no longer sufficient to find scale as retaining that business is ever more difficult.

Some examples of Moats:

Brand

Network effect

Lock-in

In my opinion, Block has been able to create a moat by focusing on 2 aspects a. Network effect and b. Lock-in.

Cash app focuses on the network effect. Each customer added to the network strengthens the value proposition for everyone as P2P transfer becomes more seamless. And Square has a moat on the merchant side, the more merchants accept Square, the more brand and customer recognition it creates for customers and merchants.

Over time, Cash app is transforming from a P2P app to an end to end finance app that meets both your needs – credit and debit. This is different from the ‘Super app’ thought process where one tries to fulfill all needs.

Square has focused on lock-in. By going deeper into the life of a merchant, it has made its service indispensable.

As you can see Square covers the entire gamut of services for businesses –

Point of sale (Payments)

General

Restaurants

Payroll

Invoices

Appointments

And much more. Leading to more and more lock-in both for the consumer and merchant business.

4. It’s effective monetisation

Block is truly remarkable in the way it’s been able to monetise.

Square and Cash app are polar opposites in a sense. Square is a more traditional business with transaction revenue comprising a big part of its overall revenue and it’s trying to expand to add additional lines of revenue. Cash app on the other hand doesn’t have a very traditional business model and is creating a new category of financial super app with revenue from several sources including subscriptions and services.

In 2022, Block earned $17Bn in revenue.

Revenue for Block is broken down into 4 broad categories:

Transaction revenue: transaction fee applied on the transaction amount. Typically 2.6% + 10c of the transaction amount charged to the seller. P2P in business accounts and payments made via CC (similar to a PG business).

Subscription and service based: Cash app and allied services.

Hardware revenue: Sales of payment hardware to merchants.

Bitcoin revenue: Fees whenever the user trades or does a transaction. Margin between buying from a customer/broker and selling it to the customer.

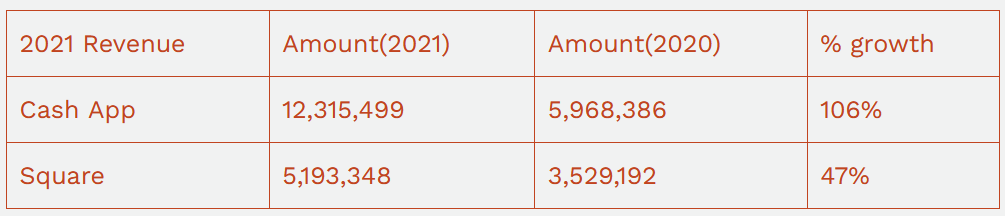

If we compare the financial performance of the last 2 years:

Square had its revenue increase by almost $8Bn in a single year. $5.4Bn of the contribution of increase was due to revenue from Bitcoin transactions.

One of the key insights here is that the hardware is primarily an acquisition tool for the merchant business for Square.

Revenue mix excluding the revenue from Bitcoin:

As we can see from the above diagram, Bitcoin services revenue comprised a significant part(56.7%) of the revenue in 2021. However it is more prudent to understand the revenue mix excluding Bitcoin as Bitcoin had a stellar ride in 2021 and activity has reduced to a great extent in 2022.

Let’s understand the mix of revenue across their 2 products – Square and Cash app.

We can see that Cash app generates substantially more revenue than Square.

Cash app has currently revenue generated from 4 different sources:

Bitcoin trading

Cash App Instant Deposit

Cash Card

Cash for Business

We’ve explained the revenue from Bitcoin trading above. However the gross profit for Block is only 4.9% of the total gross profit. Thus the healthy growth is attributed to growth in Cash app active customers, increase in Business accounts and broader economic recovery.

The success of Cash app’s monetisation is in my opinion due to 2 reasons –

Increasing lock-in

Ecosystem strategy

Let’s understand the first point.

Increasing Lock-in: One of my biggest theories is that for app products to become sustainable businesses, they have to find a way to lock-in the customer. Without a central reason to lock-in the customer, churn is a recurring problem and up-hill battle for both growth and monetisation.

This theory is validated in some way by the change in the revenue post introducing Cash Card. An offline product that complements your online experience leads to an overall increase in retention, engagement and hence monetisation.

And we can see that in the current year, out of the 47m monthly transacting users, Cash Card comprises an enviable 15m users.

The other important thing is ecosystem play - to build habits across items to increase revenue from them all.

However we can see from the latest presentation that they’ve been able to further increase it to $45 by the introduction of borrow.

Square has currently revenue generated from 4 different sources:

Transaction revenue

Hardware revenue

Other(?)

A big driver to revenue in Square is the transaction revenue. While there’s a lot more to explore in this piece too, I’ll keep it for a separate post.

We can thus see that even though the revenue is greatly different for the two products, the net contribution to gross profit is pretty close.

And that’s it for now. In upcoming posts, I’ll cover a few other topics like payback period, effect of retention on Square and Cash app, commentary of the Flywheel deployed by Cash app and more.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🌏 International

Revolut plans to launch one-click payment feature Revolut Pay, and has signed up Shopify, Prestashop, WH Smith, and Funky Pigeon. Goldman Sachs’ loss rate on credit card loans is the worst among big U.S. card issuers and “well above subprime lenders” at 2.93%. Jordanian FinTech liwwa raised an $18.5mm pre-Series B round of equity and debt funding. MODO, a virtual wallet popular in Argentina, launched an instant payments feature and is exploring a buy now, pay later. SWIFT is testing a blockchain project with crypto startup Symbiont to drive “efficiencies in communicating significant corporate events”, like dividends and merger. PayU acquired Ding, a Colombian payments company. One, the Walmart fintech company in the US, is pilot testing its banking services to Walmarts sellers, employees and select users. The US Consumer Financial Protection Bureau plans to start regulating BNPL companies, such as Klarna and Affirm, and issue guidance or a rule to align standards. Apple Pay processes $6 trillion annually, edges out Mastercard according to a report.

Looking for the news digest? Read all the week’s fintech news and updates in India and SEA over at This Week in Fintech - India and SEA Edition.

🏷️ Other Notable Nuggets

👋🏾 That's all Folks

If you’ve made it this far - thanks! As always, you can always reach me at connect@osborne.vc. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.