Flight simulator for financial services | Fintech Inside - 108

World models and synthetic user bases could be the next frontier in financial services for risk, regulation and infrastructure.

Hi Insiders, I’m Osborne, an investor in early stage startups.

Welcome to the 108th edition of Fintech Inside.

Every pilot who has ever carried passengers has already crashed a plane.

Not on a real runway but in a simulator. Over and over, across hundreds of hours, in conditions designed to break them. Engine failure at take-off. Wind shear on approach. Total hydraulic loss at 30,000 feet. The aviation industry decided long ago that the only acceptable place to make fatal mistakes is in a room where nothing is real.

So far, the only way for the financial services industry to simulate risk management was in a spreadsheet. But the product was test in the wild.

A bank launching a new credit product runs a pilot, a few thousand real customers, real money, real consequences, and calls it testing. A fraud team discovers a new mule network pattern when the mules have already moved the money. An insurer calibrates its AI claims engine on live claims, paying the price of every wrong threshold in real time.

We carry passengers on the first flight. The question this edition explores: what changes when financial services industry can simulate risk management on synthetic users?

LLMs make that possible. But is there an opportunity for fintech startups to build?

Thank you for supporting me and sticking around. Enjoy another satisfying week in fintech!

Considering angel investing? I get a bunch of fintech founders reaching out to me for investors. I’d be happy to put you in touch. Send me a DM here.

🤔 One Big Thought

Flight simulator for financial services

What world models mean for risk management in financial services and why simulation-first strategy could be a competitive advantage

When I was in college, I wanted to build a humanoid robot.

Not fix one. Build one. The whole thing. A machine that could walk, think, adapt, and exist in the world the way humans do. I was obsessed with having a never-tiring companion to do things for me, maybe I was just lazy. The problem was I was never particularly gifted at physics or mathematics, which, it turns out, are fairly important if you want to build a humanoid robot.

So here I am, a venture capital investor. But the fascination never really left.

What I did not know back in college was the hardest part of building a robot was not only the hardware. It was the training too. How do you teach a machine to navigate a world it has never seen? To react to a chair placed where no chair was before? To recover from a fall it has never taken?

The old answer was deterministic programming i.e. code every move, script every response. As processing power improved, thanks to Moore's law, and neural network approaches became commonplace, training improved, but it was still slow, brittle and tough to scale.

With the discovery of the transformer architecture, large language models can be trained on massive amounts of data, making it possible to train AI agents that can generalise to new situations.

Over the past two years, two events brought back my fascination for robots with full force:

The first was watching Google DeepMind’s work on world models, training robotic systems entirely inside synthetic environments, exposing them to millions of simulated scenarios, edge cases, and adversarial conditions, before real-world deployment.

Source: Google DeepMind The second was NVIDIA’s Omniverse and Cosmos platforms - a physics-accurate simulation infrastructure purpose-built for training autonomous systems in synthetic reality at scale.

Enter world models.

Today, Google DeepMind’s Genie 3 generates entire photorealistic, interactive environments from a text description. A robot trains inside that synthetic world - bumping into walls, grasping objects, navigating edge cases, for thousands of hours. It fails safely, learns continuously, and emerges into the real world already prepared for scenarios it has never physically encountered.

Waymo took this further. In February 2026, Waymo adopted Genie 3 to build its “Waymo World Model.” The Waymo Driver had logged 200M real autonomous miles, but billions more in simulation. The result: a self-driving car that crashed a million times in a simulator so it crashes near-zero times on real roads.

I find this approach of running simulations super relevant to financial services. Not as a metaphor but as a blueprint.

My thesis is that better risk management in financial services will come from firms that simulate before they ship. Running thousands or millions of synthetic users, transactions, and fraud scenarios through a digital twin of their financial product before it touches real customers.

The same way a robot trains in a synthetic world, a financial product can train in a synthetic economy.

What exactly is a world model?

Put simply: a world model is a digital sandbox that simulates how actual people, customers, fraudsters, borrowers, regulators, each with varying parameters of income level, locations, spending behaviour, devices, and other characteristics, will behave in specific scenarios. Simulation is running thousands of those scenarios through the sandbox to see what happens before you commit real capital.

Think of it like this: if you open a new store on a busy Mumbai street, you do not immediately stock inventory and hire staff. First, you study foot traffic. You observe competitor pricing. You understand peak hours. Then you experiment with different displays, promotions, and product placements. You simulate the economics of that store in your head, or better yet, with real data. A world model digitises that process at scale and speed. It can simulate 10,000 “stores” across 10,000 “streets” in minutes. The only difference is the sandbox runs in silicon instead of in your head.

A pattern across industries: simulate the human, not just the system

The usefulness of simulation extends far beyond finance. Consider three examples.

War games: RAND Corporation and military strategists have used simulated conflicts for decades, not to predict outcomes, but to surface second-order effects. A troop movement triggers a supply chain response that triggers a diplomatic reaction. A spreadsheet cannot capture that cascade. Only a simulation of human decision-making under stress reveals it.

Pandemic modelling: In October 2019, Johns Hopkins’ Event 201 simulated a novel coronavirus pandemic. It predicted supply chain breaks and hospital crises. When COVID-19 arrived months later, the simulation proved failure modes were knowable in advance.

Flight simulators: Every pilot trains for emergencies they have never faced. When engine failure happens at 30,000 feet, the pilot does not reason from first principles. They react from muscle memory built in a simulator.

Google’s own DeepMind pushed the frontier by famously training AlphaFold to predict protein structures and then beating the world champion at the game of Go by building AlphaGo. DeepMind achieved all this by approaching the problem as a game.

Common thread: all three simulate human behaviour under stress, not just physics or probabilities. That is what makes the LLM-powered approach different. It models people i.e. what they do, how they lie, who they blame, not just math.

Why should a financial product train in a simulator?

In aviation, no pilot carries passengers without hundreds of hours in a flight simulator. They practice engine failure, wind shear, bird strikes, emergencies most will probably never face in real life. When they do face them, they have already lived the scenario. The simulator collapses years of rare-event exposure into hours.

Today financial services operates in reverse.

A fintech launching a new BNPL product tests it on real customers with real money. A bank rolling out a new fraud detection system learns what it missed after the fraud happens. An insurer deploying an AI claims engine calibrates thresholds through live claims, paying the cost of every false positive and false negative in real time. Sure, it’ll be in “closed beta” or pilot mode to track vintage performance, but parameters change quickly when the rubber hits the road.

We test products on the equivalent of live passengers.

Simulation is not new to finance. It just simulated the wrong thing.

Banks have run simulations for decades. Monte Carlo models for portfolio risk. Value-at-Risk calculations for market exposure. Stress tests for capital adequacy. These simulate numbers, interest rate movements, default correlations, market volatility.

But, as they say, the best fiction is written in Excel.

They do not simulate people, scenarios, or behavioural patterns.

That is the limitation LLMs now address. A growing body of research uses large language models as “synthetic participants” i.e. generating behavioural responses that approximate real user decisions. A 2026 study validates LLM simulations as behavioural evidence, showing they can reproduce known economic patterns. JPMorgan Chase’s 2026 Emerging Tech Trends report explicitly calls out “AI-powered simulation” with synthetic users as a key trend i.e. synthetic personas and continuous attack simulations replacing real-world testing (Page 55 onward).

The shift is from simulating macro trends/markets to simulating users.

Applications in financial services

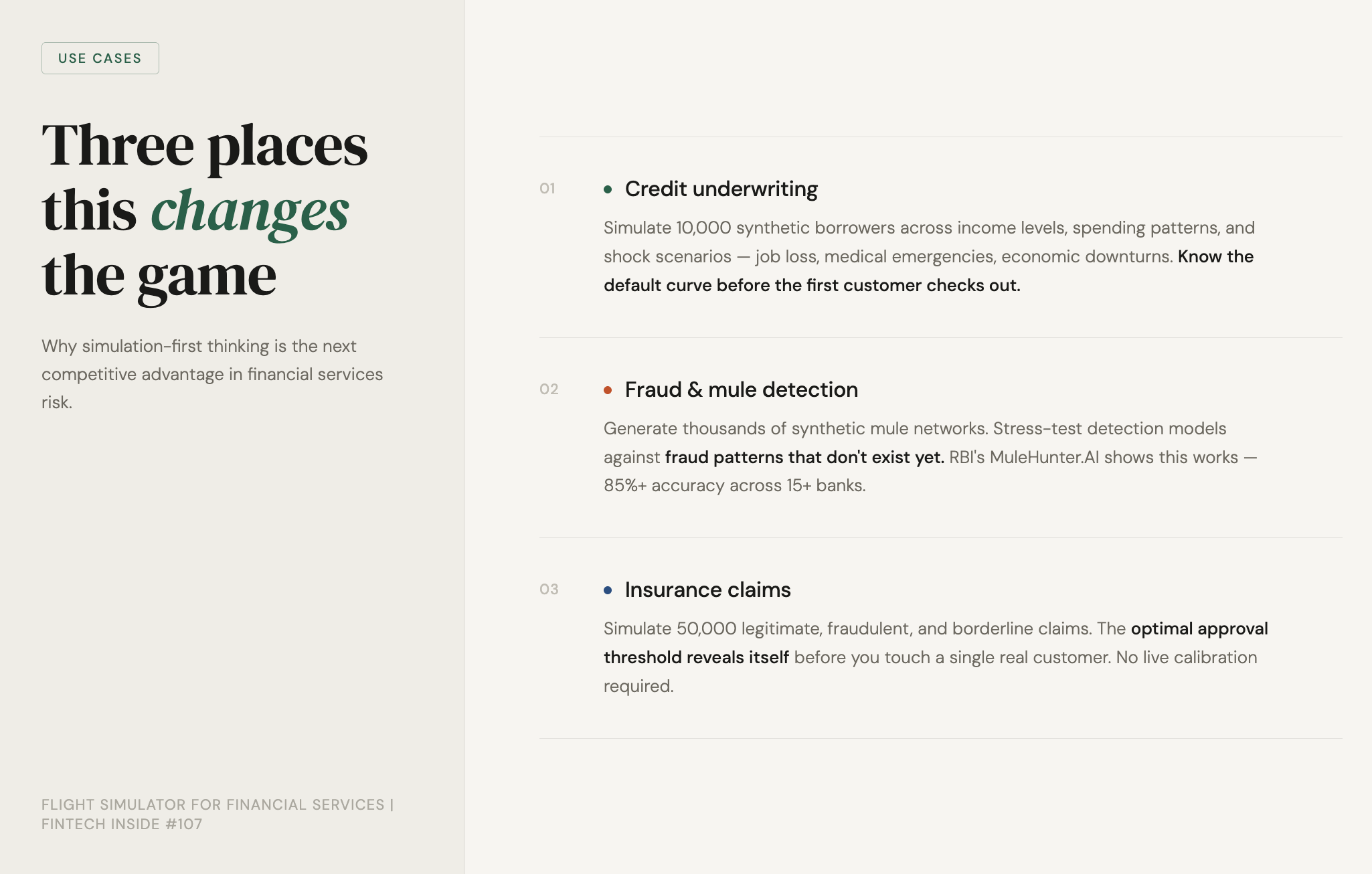

Credit underwriting

A fintech building a BNPL product faces an impossible choice: underwrite conservatively (losing customers) or loosely (accepting defaults), no middle path without data.

With a world model, a company could simulate 10,000 synthetic borrowers. Varying income levels, spending patterns, repayment behaviours, shock scenarios, job loss, medical emergency, economic downturn. Even the synthetic profiles could be auto generated by LLMs or from past data.

The simulation could reveal the default curve before the first customer checks out. The team knows exactly where risk thresholds should sit because they’ve watched 10,000 versions of their borrower behave across every stress scenario.

Fraud detection and mule accounts

The Indian government and RBI have flagged mule accounts as a systemic risk. The RBI Innovation Hub built MuleHunter.AI, an AI tool detecting mule accounts with 85%+ accuracy, now rolling out across 15+ banks.

But today’s fraud patterns shift tomorrow. Mule networks evolve. Social engineering tactics adapt. A static detection model chases yesterday’s crime.

A simulation environment changes this. It generates thousands of synthetic mule networks, testing detection systems against novel patterns before fraudsters deploy them. Banks stress-test their fraud models against threats that do not yet exist. The RBI Innovation Hub could open this as a shared simulation layer for all banks, a collective immune system trained on synthetic attacks.

Insurance claims

An insurer deploying an AI-driven claims approval engine faces a calibration problem. Approve too aggressively and fraud leaks through. Reject too aggressively and legitimate customers get denied, damaging trust.

Simulate 50,000 claim scenarios, legitimate, fraudulent, borderline and more, and the optimal threshold reveals itself. The insurer enters the market with a calibrated system, not a guessing game.

Three more places simulation bites

Credit, fraud, and insurance are the obvious ones. These three are less obvious.

KYC and identity verification: Synthetic identity fraud, where fraudsters blend real and fake data into convincing new identities, costs financial services millions annually. A simulation environment can generate synthetic identity profiles that push the boundaries of current KPIs. Banks can test their verification pipelines against emerging fraud strategies before real criminals deploy them.

Payment routing and transaction risk: Every payment network decides in milliseconds whether to approve or block a transaction. A simulation can generate millions of synthetic transaction patterns, including evolving fraud tactics, to find the optimal balance between friction and loss. Lower false declines. Faster settlements. Higher conversion. All before going live.

Insurance product design: Insurers set premiums based on historical loss data. But the world is not static. Climate change. New vehicle technologies. Shifting demographics. All of these change the risk equation. A simulation can model how a new product or pricing change performs under dozens of future scenarios, not just past conditions.

The best part is, an LLM/world model can literally generate scenarios and edge cases that we could not possibly imagine. Talk about dealing with the unknown unknowns!

Simulation is an illusion of accuracy which captures historical patterns without understanding the underlying causal economic drivers

The strongest opposing view deserves a fair hearing.

“Simulations are only as good as their assumptions. A synthetic user is not a real user. LLMs hallucinate. Behavioural simulations encode the biases of their training data. You might simulate 10,000 scenarios and still miss the one that breaks your product. The 2008 mortgage crisis happened because sophisticated risk models failed to capture correlated defaults. A simulation would have failed similarly.”

This is worth sitting with, especially the 2008 point, because it sounds like the kill shot. It isn’t.

The models that failed in 2008 were simulating correlated macro risks: interest rate movements, default probabilities, market volatility. They were, in effect, very sophisticated Excel sheets. What it did not simulate was human behaviour, the mortgage broker who misrepresented income, the borrower who defaulted the moment equity turned negative, the rating agency analyst who stopped asking questions. The cascade was behavioural.

That is the gap world models simulation addresses. The shift isn’t from bad models to better models. It’s from simulating markets to simulating people. 2008 doesn’t argue against this approach, it argues for it.

No simulation replaces reality entirely. A flight simulator doesn’t produce a perfect pilot. But a pilot who trained in one handles their first real emergency better than one who didn’t. A BNPL product tested against 10,000 synthetic borrowers could have a better risk profile than one tested against 100 real users in a regulatory sandbox.

The bar is “better than current practice.” But unlike the 2008 models, this approach is actually designed for the problem that broke them.

What this means for founders and regulators

India has a head start. The RBI already operates a regulatory sandbox where fintechs test products with real data. The Inter-operable Regulatory Sandbox (IoRS) spans RBI, SEBI, IRDAI, PFRDA, and IFSCA, allowing products that cross regulatory boundaries to be tested under one roof.

This is a strong foundation. But it requires a partnership between a licensed firm and uses real data at limited scale with a narrow scope.

A synthetic world model could complement it: let firms stress-test products against millions of synthetic users and scenarios before they enter the sandbox. The sandbox becomes the final exam, not the first test.

The implications flow in three directions.

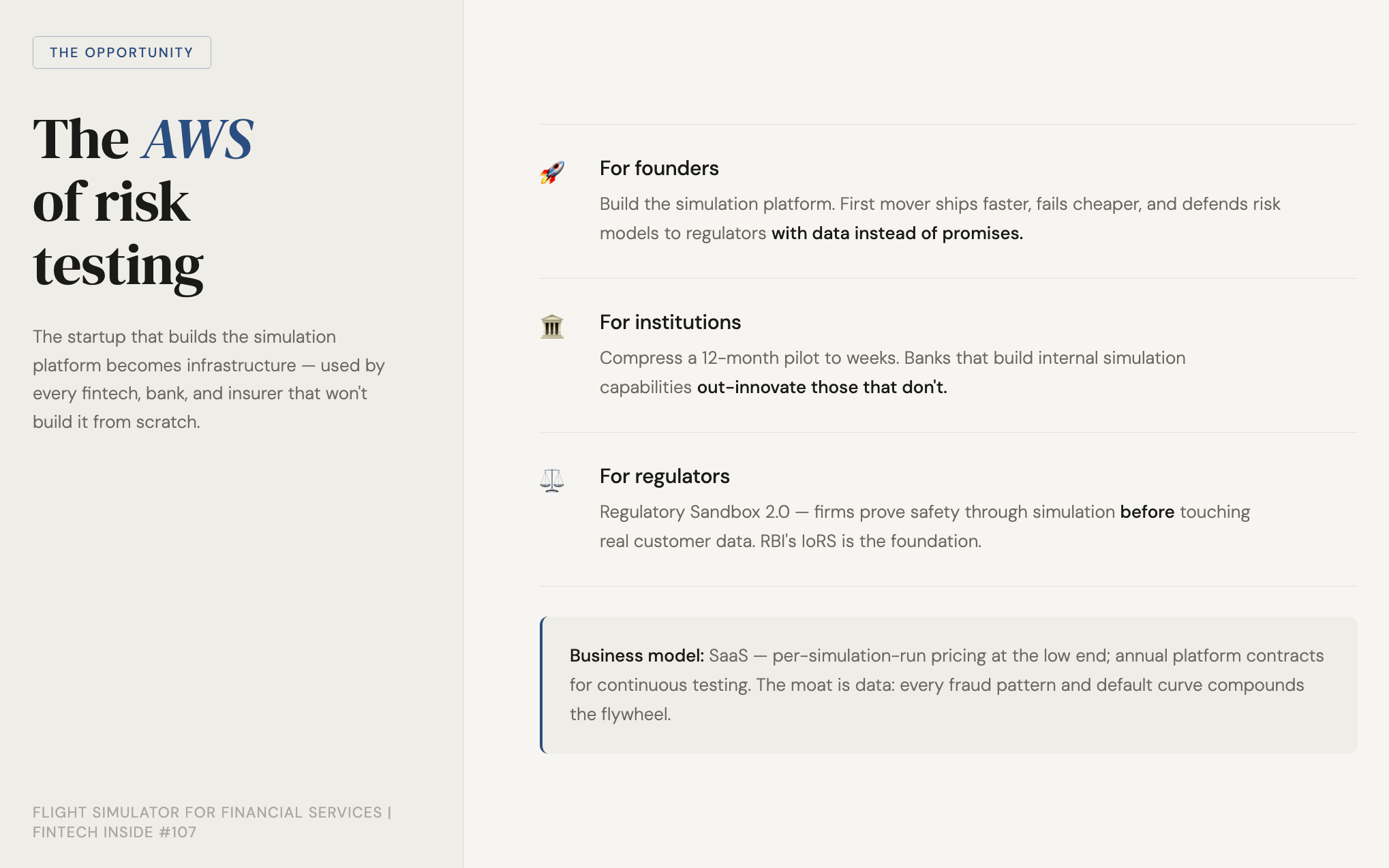

For founders: A build opportunity. The startup that creates the “financial world model” i.e. a simulation platform where financial firms test products against synthetic users, becomes the AWS of risk testing. The first fintech to embed simulation into product development ships faster, fails cheaper, defends risk models to regulators with data instead of promises.

For institutions: Simulation transforms the cost of innovation. Launching a new credit product today requires more than a year of pilot testing, internal roll outs, regulatory review, and a cautious rollout. A simulation environment compresses this to weeks. Banks and NBFCs that build internal simulation capabilities out-innovate those that do not.

For regulators: The regulatory sandbox 2.0 includes a shared simulation layer. The IoRS framework could offer synthetic testing environments as a public good, letting firms prove product safety through simulation before touching real customer data. The RBI’s MuleHunter.AI shows the blueprint: build a shared tool, offer it free to all banks, improve it together.

The investment play: This is infrastructure that will be used on an ongoing basis. I don’t think simulation will be a build and sell once model. It’ll require continuous refinement.

Startups that build simulation platforms for financial services sit at the intersection of three mega trends: AI, risk management, and the digitisation of finance.

Think of it as the “AWS of risk testing”, a platform layer that every fintech, bank, and insurer will need but won’t want to build from scratch.

The business model is SaaS - priced by scenario volume, with a consumption layer for compute-heavy stress tests. Think per-simulation-run pricing at the low end, annual platform contracts for institutions running continuous testing cycles.

The moat is data: Every fraud pattern, default curve, and behavioral anomaly that passes through the simulation becomes training signal. That data feedback loop compounds in the flywheel of better simulation → more customers → more data → better simulation.

That compounds in a way that a one-time software sale doesn’t. The firms that get in early lock in a data advantage that’s genuinely hard to replicate. The cost structure is real. Inference at scale isn’t cheap, but margin expands as the models improve and the dataset deepens.

This is a business that gets cheaper to run as it gets better. That’s the kind of unit economics worth building toward.

I think AI-native startups i.e. startups that begin with the synthetic user layer and expand outward into risk management, is where I think the outsized returns live. A startup that builds a clean simulation layer, independent of any single financial product, can become the default testing environment for the industry.

What the future of risk management holds for the industry?

DeepMind proved world models work. Waymo proved they scale. JPMorgan Chase proved the largest financial institution on earth is thinking this way. The pieces are all there.

The company I’m watching for looks like this: it starts narrow, building for one vertical, one problem, probably fraud or credit underwriting, and builds the simulation layer so well that it becomes the default testing environment for that problem across the industry. It doesn’t try to be a bank or a risk engine. It sells picks and shovels: run your product through our synthetic world before you ship it to real customers.

The wedge is regulatory. The first firm that walks into a SEBI or RBI sandbox conversation with a simulation report - “here are 50,000 synthetic scenarios we stress-tested before touching a single customer”, could potentially change the conversation with regulators permanently. That becomes the new standard of care. Every firm that follows has to meet it.

Within five years, launching a financial product without simulating it against synthetic users will seem as reckless as flying a plane without a simulator.

The question is which founders build the infrastructure, and which institutions adopt it first.

If you could simulate 10,000 versions of your customer before your next launch and know exactly where the defaults, fraud, and failures would come from, would you still launch the same way you do today?

I want to hear why I’m wrong. Simulation has limits. But so does testing with real money and real customers. Which ones are you willing to live with?

Would love to hear your views.

If you’re a founder working on any of the use cases above, credit underwriting, fraud detection, KYC infrastructure, or regulatory tech, I’m actively looking at this space. Let’s talk.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🎵 Song on loop

Fintech updates can get boring, so here’s an earworm: Never thought I’d get hooked onto AI music, but this youtube channel (Shanti Instrumentals) is on loop for me playing in the background all day as I work. It’s calming, it helps me focus and I just can’t believe it’s made with AI. Blows my mind.

Call outs

[VIDEO] What does the $ actually stand for? (I never really thought to question where the dollar sign comes from, this video explains the fascinating history).

[VIDEO] The World’s First Smart Home (built in the 19th century by William Armstrong in Cragside, UK).

[ARTICLE] The Trap India Faces Isn’t Just Geopolitical Anymore (related to the INR/USD rate, but goes deeper).

[ARTICLE] The Mathematical Reason Most People Never “Make It”

👋🏾 That’s all Folks

If you’ve made it this far - thanks! As always, you can always reach me via DM at osborne.vc/dm. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.

Really interesting framework for thinking about risk management beyond traditional rule-based models. The idea of “simulation-first” finance feels especially relevant for areas like credit underwriting, fraud detection, and receivables workflows, where testing against synthetic scenarios could improve both operational resilience and financial decision-making over time.

Hey Osborne! This is interesting . Do you have thoughts on how to get started with running these simulations ?

We’re building the first instant payout product for flight delays (YC-backed); and ramping up distribution with a few airlines and OTAs.

I’d like to know more to model this out and test the approach. let’s connect ?