Fintech Inside #24 - 13th Mar, 2021 | Crypto's Problem

The blockchain community has a problem. I address that problem in today's edition. Also - India's financial industry was disrupted, India is exploring SPAC's and GooglePay's plan to monetise

Hi Insiders, Osborne here.

Welcome to the 24th edition of Fintech Inside. Fintech Inside is the front page of Fintech in emerging markets.

Blockchain and its applications cannot be ignored. But the blockchain community has a big problem. I discuss that problem in today's edition.

There's also news of India's financial industry being disrupted, an expert committee is formed to explore SPAC's in India and GooglePay is finally monetising its users.

In other news: Did you know, Chase was acquired by Chemical Bank in US? Here's an in-depth report of Women in Global Fintech by FT Partners. The Eastern Caribbean Central Bank (ECCB) is expected to launch its CBDC - DCash, in H2-2021.

🤔 One Big Thought

Blockchain community's biggest problem

Blockchain. Cryptocurrency. Hashing. Hashrate. Mining. Fork. Soft fork. Hard fork. Stablecoin. Bitcoin. Bitcoin Cash. Dogecoin. Ripple. Ethereum. Gas. Smart Contracts. Cold Storage. Hard Storage. DeFi. Dapps. Digital Asset. NFT. Token. CBDC.

Ever heard these terms and found yourself scratching your head? Happens to me all the time. These terms are thrown around a lot these days as blockchain, cryptocurrencies and bitcoin gains prominence in the world of Finance. If you're wondering what those terms refer to, they are all terms related to blockchain and its applications. You can get yourself up to speed on what those terms mean through this link.

I didn't just throw around those terms to brag about how much I know about blockchain, because I know less than 40% of those terms. I know I'm not alone here, though. The lack of understanding of those terms illustrates the problem that the blockchain community is facing - accessibility.

Accessibility, not in terms of access to a blockchain, a crypto-currency or even an NFT. Accessibility in terms of understanding, trust, real world applications and absence of fear. If and when the blockchain community solves for these 4 things, I believe it will be adopted by the mass market. If not, it will remain a niche.

Blockchain and Cryptocurrency are slowly becoming mainstream with real world applications and implications. Today, we see financial institutions holding cryptocurrency in their treasury’s. It is still to find love among regulators globally. Other than launching central bank cryptocurrencies, regulators are wary of any other applications. The community has to make blockchain accessible for it to cross the high barrier of regulation to find mass adoption. Regulators need to be educated but more importantly in the language they understand.

The blockchain community comes across as that child who grew up in the digital age and gets frustrated when trying to explain to their parents (regulators) how a new app on their smartphone works. Large tech companies spend billions trying to make their products understandable and accessible. It is an iterative process, it will take time, no doubt. But to me, it seems that very few people in the community are making that effort to make it accessible. This is changing though - more folks are getting involved to make blockchain accessible. This is the problem that needs attention.

If you would like to learn more about blockchain, cryptocurrencies and recent craze around NFT's, read these: What is an NFT. Largest NFT sale to date - USD 69 mn. How to create and sell an NFT. Everything you need to know about blockchain. Write simply by Paul Graham.

Highly recommended listening: Tim Ferriss' interview of Katie Haun where she talks about her stint at the FBI in nabbing Dread Pirate Roberts of PirateBay and subsequently getting involved in blockchain, cryptocurrencies and much more. It's definitely worth your time.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

3️⃣ Fintech Top Three

1️⃣ Financial Services and Payments were disrupted due to a new SMS Scrubbing System

A new blockchain-based, SMS scrubbing system, that went live on Sunday midnight, disrupted delivery of banking and payments SMS'. These SMS' were primarily for OTP's and notifications. Some said that 40% of all SMS deliveries didn't go through. After this disruption, the Telecom regulator deferred the launch of this system by 7 days to iron out these issues.

Takeaway: For the uninitiated (me), this new SMS scrubbing system is a way to weed out unregistered commercial SMS'. Because some legit business were unable to get their content and ID's registered on the blockchain, their commercial SMS' were not being delivered.

This system is probably a great way to deal with spam/fraud over SMS but there should have been proper trials or a phased roll out. Over one billion commercial SMS' get delivered in India each day, a large portion of which is banking and commerce OTP & notifications. For some startups, this was the worst single-day drop in their NPS.

2️⃣ SEBI formed an expert group to evaluate the feasibility of SPAC's

India's securities regulator - SEBI, formed an expert committee to evaluate if SPAC-like structures can be introduced in the Indian markets. This committee has been asked to submit its report at the earliest.

Takeaway: It is amazing to see the Indian securities regulator be pro-active in thinking about SPAC's. They have been making claims of wanting to make going public in India easier. It is left to be seen if SEBI is actually serious about SPAC's or just some optics management.

However, I don't think the Indian retail investor is ready for SPAC's just yet. Firstly, the structure is radically different from the traditional IPO route. Secondly, there are few brands (tech or otherwise) in India that the retail investors know of to build enough conviction to invest (without going the traditional roadshow route). Lastly, SPAC's need a sponsor/promoter with a strong brand itself - I don't see individuals attaching their names here. Indian conglomerates are fairly risk averse and will wait to see the first few dominoes fall before getting on the SPAC bandwagon. Without these known, trusted names sponsoring a SPAC, it's unlikely that retail investors will participate.

3️⃣ GooglePay released plans to monetise its users

3-odd years after launching, GooglePay decided to start monetising its user base. As part of its latest app update, going out in the coming week, GooglePay will tap into users' transaction data to monetise the same. As part of the same update, GooglePay will give users the option to not share any financial or otherwise data with GooglePay.

Takeaway: Same as CRED, Indian startup folks love to hate that GooglePay has never had a plan to monetise. GooglePay will tap into users' transaction data to offer personalised deals to users. Users will also be given an option to delete certain records from their history. GooglePay says that by default all users will be opted out of sharing this data and will have to explicitly opt in.

This is a very surprising move by GooglePay, as Google knows the power of defaults when it comes to behaviour change. Moreover, if users have opt in, assuming few do, how will it earn its revenue? It seems like users will be inundated with pop ups saying "enable personalised offers".

🚀 Featured Fintechs

Featuring 3 Fintech's weekly that have a unique business model, unique product or have recently launched.

Riskcovry - (Series A | Insurance)

Riskcovry is an Insurance API platform that enables B2C brands to offer integrated insurance products. Through their API's brands can manage end-to-end lifecycle management.

It has 50+ B2C brand partners selling insurance and expects to sell 200,000 insurance policies in this financial year.

Riskcovry raised a total of USD 6.25 mn to date. Latest round (Series A) of USD 5 mn was announced this week.

Samunnati - (Series D | Agri Finance)

Founded in 2014, Samunnati is an agri finance startup that provides trade and agri finance for inputs to small holder farmers and agri-SME's

It has cumulatively disbursed USD 810 mn (INR 6,000 crs) in loans to 54 agri-value chains in 20 Indian states

Some studies show that only 11% of the farming population has access to formal credit.

Samunnati raised USD 124 mn in equity to date along with debt from several US and EU DFI's.

Kevin. - (Lithuania, Payments)

Kevin. is a merchant payments acceptance startup.

This week, it launched a "Card Switching" product to cut card networks from the payment process.

When making debit card payments at checkout, Kevin. identifies the card network and bank name and then switches the payment type from debit card to PSD2 (similar to UPI in India).

By doing this, Kevin. cuts out the card networks and saves the merchant high transaction fees.

Founded in 2018, Kevin. has raised a total of EUR 3.4 mn.

Let's get your startup featured here. Submit your Fintech startup

🇮🇳 India

- 📰 Market Updates:

- FINTECH's: Truecaller discontinued its UPI payments service. GooglePay will give users control of financial data shared with Google. GooglePay to start monetising users data.

IAMAI, industry body, highlighted the negative effects of a crypto ban. India’s fintech sector valuation could touch USD 150-160 bn by 2025.

FamPay, a teen banking Fintech, is in talks to raise USD 25 Mn led by Elevation Capital. DotPe, a payments platform, registered 4.6 mn merchants on its Digital Showroom platform within 4 months since launch.

Samunnati, an agri-fintech startup, claimed to have disbursed USD 810 mn in loans to 4 mn farmers. Deloitte India finds that Rupeek, a gold-backed loan platform, is India's fastest growing startup at 7,295% growth over 3 years.

Paytm is likely to apply for a New Umbrella Entity license with Ola. PayMate, a payments platform, has achieved annualised run-rate of $1.3 bn in GST payments.

- TRADITIONAL BANKING: Indian government is building a National Economic Offence Record database at a cost of USD 6-7 mn. IDBI Bank was removed from RBI's Prompt Corrective Action framework after 4 years.

RBI said it had not imposed any penalty on Banks for failing to comply with KYC updating guidelines.

- 🚀 Product Launches:

Paytm launched SmartPOS App for contact-less payments on android phones. HSBC launched credit card VISA payments via GooglePay.

- 📝 Regulatory Updates:

- SEBI (securities): Issued a new framework for Mutual Fund investments in debt instruments. Formed an expert group to evaluate feasibility of SPAC's.

- IRDAI (insurance): Imposed INR 1 Cr (USD 135K) penalty on Chola MS General Insurance.

- 💰 Funding Announcements:

Kinara Capital (micro loans for small businesses). Risckovry (insurance API). Turtlemint (insurance distribution).

🌏 Asia

- 📰 Market Updates:

Lend East launched Levl - a revenue based finance startup, in Singapore. JD.com’s FinTech unit is exploring withdrawing Shanghai public listing.

Mastercard and Samsung partnered in Korea to launch a biometric card that uses a built-in fingerprint sensor to authorize in-store transactions.

Deutsche Bank launched GEM Connect - a solution for treasury automation. YAS Digital launched Hong Kong's first passenger micro-insurance product: RYDE with YAS.

South Korea’s Shinhan Bank demoed its CBDC platform. Line’s Thailand social bank gets 2 million users in 4 months.

- 💰 Funding Announcements:

- FUND RAISES: Fadada (China, e-signature). AMTD Digital (Hong Kong, banking). WeLab (Hong Kong, lending and banking).

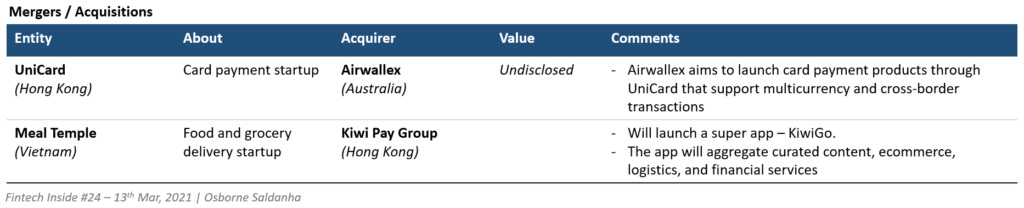

- ACQUISITIONS: Airwallex acquired UniCard. KiwiPay merged with Meal Temple.

🌏 International

It's been a busy week in fintech! If you missed any of it, check out Nik Milanović's This Week in Fintech for the headlines of the past week.

- Plaid launches a new returning user experience.

- Mastercard launches a card to reward shopping at women-owned businesses.

- Nium expands in Africa.

- HSBC offers banking to the homeless.

- Chase is winding down Chase Pay.

- Big fundraises from Starling, Flutterwave, and M1 Finance.

👋🏾 That's all Folks

If you’ve made it this far - thanks! As always, you can always reach me at connect@osborne.vc. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

Found a broken link or incorrect information? Report it.

See you in the next edition.