Digital Debt Collections | Fintech Inside #88 - 17th Mar, 2025

The contrast between India's sophisticated lending infrastructure and its antiquated collection practices represents one of fintech's most glaring innovation gaps.

Hi Insiders, I’m Osborne, an investor in early stage startups.

Welcome to the 88th edition of Fintech Inside. Fintech Inside is the front page of Fintech in emerging markets.

This edition highlights the debt collections market, the opportunities, my reservations in the sector and the future of collections.

For years, India's debt collection industry has been fraught with malpractices, relying on outdated methods and fragmented processes despite being a key part of India’s $2 trillion credit market.

The contrast between India's sophisticated lending infrastructure and its antiquated collection practices represents one of fintech's most glaring innovation gaps.

As retail credit continues its high demand and growth and new borrowers enter the system, the opportunity to modernize collections has never been greater.

With delinquency rates hovering near historic lows and a new wave of tech-enabled startups challenging traditional recovery methods, we're witnessing the early stages of a long-overdue transformation.

Thank you for supporting me and sticking around. Enjoy another great week in fintech!

🤔 One Big Thought

Debt Collections’ Goldilocks Period

Why innovation in India's debt collections is Days Past Due

Before we dive into today's piece, let's understand a few helpful concepts in the credit industry.

Credit/Advance/Loan: From the lenders perspective, a loan given to a borrower.

Debt: From the borrowers perspective, a loan taken by the borrower.

Days Past Due (DPD): If principal and/or interest is due on a certain date, but the same is not repaid on that date, then the loan is Days Past Due from the Due Date. So, if repayment is still pending 7 days after due date, then the DPD is 7 or DPD7. Same for 30 days i.e. DPD30 and so on.

Delinquency: Any amount (principal/interest) that falls in the DPD bucket i.e. DPD1 or DPD180 or more, then the amount is classified as Delinquent. Basically, amounts not paid on or before the due date are classified Delinquent.

GNPA/NNPA: Gross Non-Performing Assets and Net Non-Performing Assets. These are loan amounts that have not been paid back even after DPD90 i.e. 90 days past the due date, basically write offs. GNPA are amounts that are DPD90. The bank also makes certain provisions (not going to get into this) from its cash and profits for anticipated loss from this GNPA. GNPA minus these provisions is NNPA.

Prime, Near Prime and Sub Prime borrowers: This is a classification of borrower risk based on the borrower's credit score. Different credit scoring companies will have different ranges, but credit scores are typically between 300-800 or 900 - 300 being high risk, and 800/900 being flawless, no risk. Any borrower above 750 score is considered Prime (or Super Prime), above 650 is considered near-prime and anyone below 650 is considered sub prime.

Thick File, Thin File, No File: Thick File is a borrower with lots of credit history in terms of years of credit behaviour and number of credit products accessed/utilised. Thin File is limited credit history and No File is no credit history.

Let's get into it.

For donkey's years now, we've been told that India is a credit-starved economy. While this is still largely true, we've come a long way in growing the borrower user base. Thanks in no small part to fintech startups who've developed smarter ways to underwrite risk of first time borrowers.

These first time borrowers, previously ineligible for loan products from incumbent banks, now have some credit repayment behaviour as part of their credit score. Incumbent financial institutions are now fighting fintech startups for this credit worthy borrower.

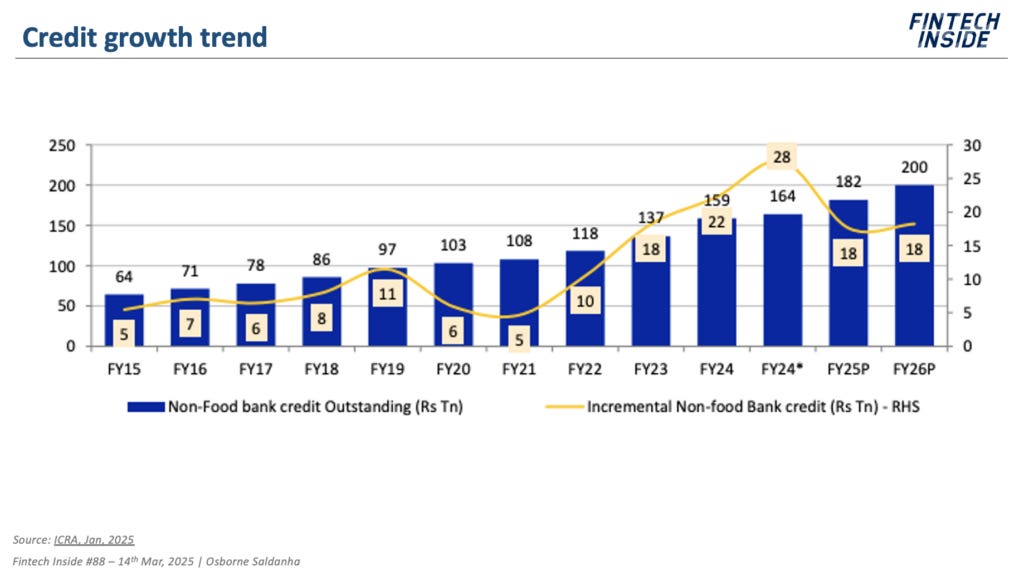

Since the pandemic, India's credit growth has been steady and healthy. Non-food bank credit grew 15-16% YoY, even growing 20%+ in some months. As of Dec, 2024 total outstanding bank credit was 165-175 lakh crore i.e. $1.8-2.0tn. Credit outstanding grew by nearly $1tn in just 5 years!

As you can see below, majority of the credit growth is coming from the retail segment i.e. credit to end users - for consumption, asset creation, or other purposes.

RBI's recent regulations and market intervention, has certainly slowed down that blistering growth rate. This was much needed to cool down the economy. Growth rate seems to have moderated to 11% more recently.

Credit growth moderation was not needed because the credit growth rate was too high. It was high, but manageable. It was also not because the default rate was high. From the chart below we can see that Net Non-Performing Assets (NNPA) is the lowest its been at 0.6% at the overall industry level.

The other chart further shows that the Near Prime and Prime borrowers make up ~90% of the borrowers in India. Only ~10% are sub prime meaning risk is limited and can be contained. All of this seems to suggest India is fairly strong when it comes to fundamentals. If there's no external shocks to India's market, we could well continue on our path to achieve projected GDP growth.

The problem comes up when households borrow more than their income/assets can sustain. As you can see from the chart, an increasing portion of new borrowing is going towards consumption. Again, this by itself is not a bad thing. 60% of India's economy is consumption driven, so it makes sense.

The challenge is that the household liabilities are growing faster than household financial savings. This means that if the credit growth wasn't slowed, or household income/savings growth didn't catch up, households would soon find it tough repay their monthly debt obligations. That would be a real problem.

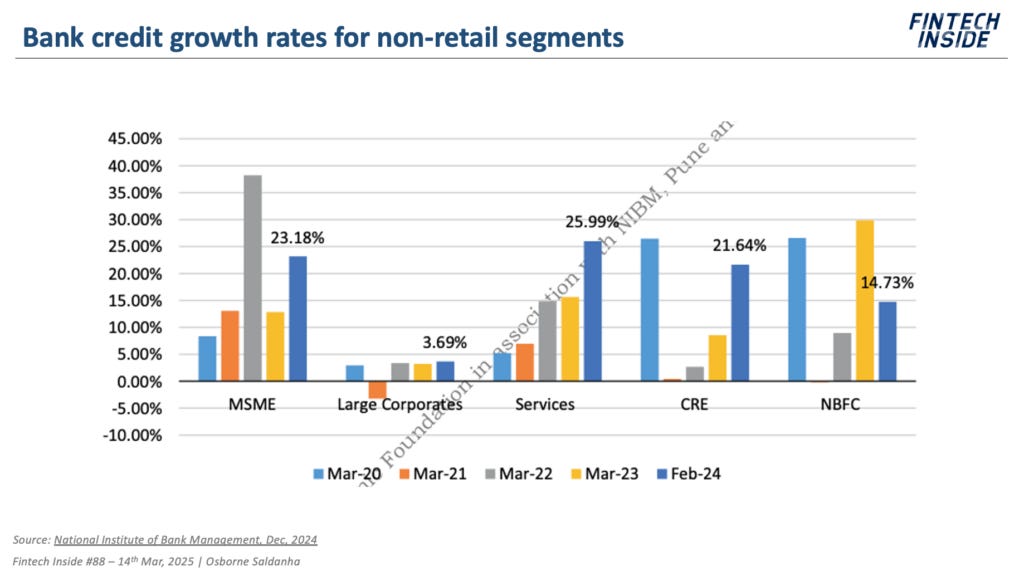

Some sectors are already starting to see stress develop including the small business finance sector, the micro finance sector and until more recently, the credit card sector and the personal unsecured sectors (see below).

Moderate credit value outstanding growth, no apparent structural or fundamental stress in the system, NNPA % levels remaining stable - all this means, we're in a "goldilocks period" for debt collections market opportunity. There's a lot of work to be done.

What is debt collections?

I'm oversimplifying, but as a lender, there are a few broad functions that are important - user acquisition, underwriting, disbursement, portfolio management and collections. As with any company, the decision for each of these functions is to either build in house, partner or outsource.

Depending on loan type, banks will use all three approaches for user acquisition. For example for unsecured, small ticket personal loan, a bank would rather partner or outsource, because the cost is too high for banks to directly acquire. So us VC's have borne these user acquisition costs by investing in fintech startups who partner with these banks. I'm joking! :)

Underwriting, disbursement and portfolio management are too critical for a lender, so that's typically done in house. Again, I'm simplifying, it's more complicated than this, because co-lending and other models exist too.

That last function of Collections is where the bank will typically completely outsource - but with certain limits.

Collections can be broken down as follows - Before Due Date, DPD7, DPD30, DPD90, DPD180 (the DPD milestone matters). When it comes to collections, borrowers are also categorised as "Circumstantial" and "Intentional".

Borrowers paying on or before due date are doing so with minimal (SMS reminders etc.) to no intervention, so this is typically not outsourced. They are revenue generating repayments at little to no extra cost.

Borrowers paying until DPD7 need some intervention (call/message reminders), but still largely pay back in time. There's limited issues/cost to following up with borrowers in this bucket, so lenders tend to not outsource loan amounts in this DPD7 bucket.

Beyond DPD7, things get a little more serious. This is where lenders will start outsourcing collections by using collections agencies to follow up with the borrower.

Collection agents are vendors onboarded by lenders to collect delinquent outstanding loan amounts from borrowers. They are supposed to consistently followup with the borrower until the amount is paid. These agencies have to follow RBI's Fair Practices Code when collecting amounts from borrowers. But sometimes things don't go according to plan and some agencies may use their agency to go beyond just calls for collections. That's where things get challenging with using these offline agencies.

Aside from the fact that one lender may use anywhere from a dozen to hundreds (depending on size of collections, location, etc) of collection agencies, the agencies typically receive borrower data in the form of unprotected excel files. Imagine thousands of rows of borrower data floating around with agencies - what a privacy nightmare. These agencies also tend to operate on the edges of the law - their job is to collect. How they collect is plausible deniability for some lenders.

The longer the loan amount in the DPD bucket, the more hands-on the collection tactics.

This is the opportunity for startups - to modernise debt collections, making it more efficient, cost effective and all the other benefits that come with organising a completely fragmented market.

There are quite a few founders who've recognised this opportunity and started businesses to capitalise on the rising retail lending market. Startups like Freeed, Rezolv, CredResolv, DPDZero, CredGenics, Spocto, PowerEdge, SkitAI, Neowise and more are modernising debt collections.

How do debt collection agencies make money?

Typically, debt collection agencies make a percentage of the delinquent loan amount. The commission percentage varies depending on the DPD bucket. This commission is what everyone is vying for. Commission is higher for the default loan accounts. In the sense, the commission will be 2-5% for the DPD7-30 bucket and could go as high as 40-60% for the DPD180+ bucket.

There's also SaaS income and other fees, but I don't think it will form a major revenue driver for these agencies.

The only metric in the industry that matters and that everyone tracks is "Efficiency". Efficiency is basically how much delinquent amount you were allocated by the lender and how much you were able to recover/collect from the borrower. For example, if a lender allocated INR 100 in default/delinquent amount, and you collect INR 15, your efficiency is 15%.

A lender may give a collection agent a portfolio of delinquent accounts ranging from DPD7 to DPD 180+. Collections efficiency is typically higher in the DPD7 to DPD30 bucket as borrower contactability is higher. With higher DPD buckets (i.e. DPD60-180+, the efficiency rate reduces and commission rate increases. Commissions are higher for DPD90+ because the lender's have already written off the amount on their books and any amount recovered is a good thing.

My information is dated, so I might be wrong, but typically, with offline, incumbent collection agents, I've seen portfolio level Efficiency range between 12-15%. After all portfolio optimisation and collection tactics, that 15% number seems... underwhelming.

The premise of startups building in this space is that with richer data, better targetting and digital payment tools, they'll be able to increase that Efficiency metric. Even a slight increase of 1-2% of efficiency means a lot of revenue. At a $2tn credit market, 2.6% GNPA, that could be a big revenue unlock. Obviously, their plan is to increase that efficiency metric as much as possible.

However, I have my apprehensions on venture-scalability of startups in this sector. Here's why:

Tough to improve efficiency: Despite all the tech interventions and credit builder programs out there, I've not seen efficiency improve beyond what the industry is used to seeing. There's no efficiency in the efficiency, if you get what I mean. The default (DPD90+) buckets just defaults to a hands-on approach to collections and digital just doesn't cut it for those buckets. More importantly, lenders rarely give "easy" borrower accounts to collections agencies, they'd typically keep it in-house. By "easy" I mean, not at risk (circumstantial delinquency) loan accounts, with updated/recent contact details and not already too far in the DPD bucket. Why give away easy revenue for free?

Tough to scale revenues: As mentioned, lenders typically split delinquent loan account allocation for collection among a whole host of collection agents. They typically refrain from giving a major portion of allocation to any single collection agent. The only time I think it makes sense for a lender to do so is if efficiency is higher than any other collection agent. And so, as you break down the "at risk" or delinquent loan book allocated to collection agents, the revenue IMO just doesn't stack up to result in a large revenue business. This makes a collections platform a good business with limited scale, but potentially not a equity fundable business.

I'm putting my apprehensions out here in public, for a few reasons:

Probably this time is different? With the GenAI wave, there are probably cost effective ways to increase efficiency. Further, some of the startups in the list are getting lenders to allocate "easy" delinquent accounts. That should probably help increase profitability and ability

I have my biases formed from past experiences (since 2016) and I'm hoping someone reads this and reaches out to tell me I'm wrong. I'll get to learn something new. Better yet, an exceptional founder comes along and changes the game and maybe it may make sense to invest then,

Ours (investing and starting up) is a risk business. If we don't have people taking risk, we'll never move forward. We'll never have people questioning first principles/status quo and pushing the envelope of what's possible. Our world is progressed, not because of pessimists, but because of optimists.

Despite my biases, I do believe debt collections needs to get better and more efficient. The current way of debt collections should not exist in 2025, unfortunately it does. This is a massive area in fintech that's still largely unorganised. We're at the beginning of what I believe is the start of the J-curve (large outstanding credit and increasing stress in the system) for this cycle of the collections opportunity. When smart founders take on this opportunity, it could unlock massive value in India's growing credit ecosystem.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

🎵 Song on loop

Fintech updates can get boring, so here's an earworm: Latest masterpiece Run it up by Hunumankind. This song may not be for everybody but the rap is tight, the lyrics are powerful, the beats increases your heart rate, but the visuals… my goodness the visuals! Get’s the people going!

👋🏾 That's all Folks

If you’ve made it this far - thanks! As always, you can always reach me at os@osborne.vc. I’d genuinely appreciate any and all feedback. If you liked what you read, please consider sharing or subscribing.

1-min Anonymous Feedback: Your feedback helps me improve this newsletter. Click UPVOTE 👍🏽 or DOWNVOTE 👎🏽

See you in the next edition.

This is as much a "lack of solid underwriting" problem as it is a collections problem :-(.

This was a really interesting read. I believe there’s a much bigger chain involved from the day an account is classified to the end of its life. I would love to know more about the nitigrities as well as how these startups plan to revolutionize this space. Looking forward to reading more from you on this topic.